- Budget & Spending

- Economics

- Law & Policy

- Regulation & Property Rights

- US Labor Market

- Monetary Policy

- Economic

- Politics, Institutions, and Public Opinion

- Health Care

- History

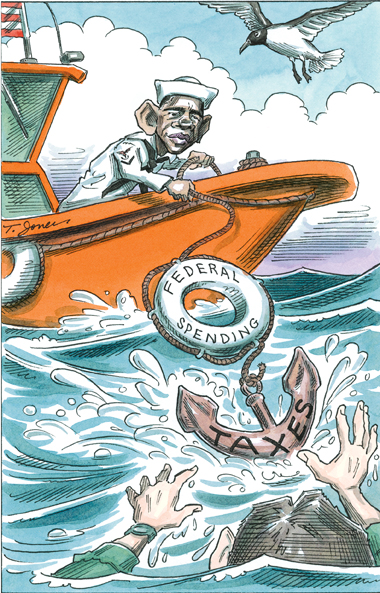

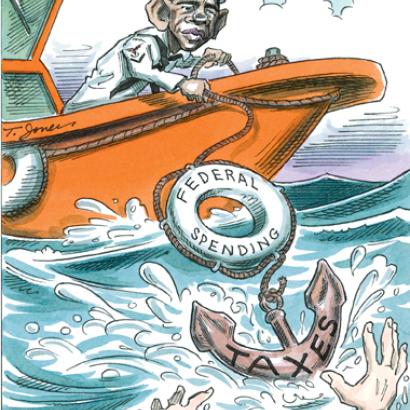

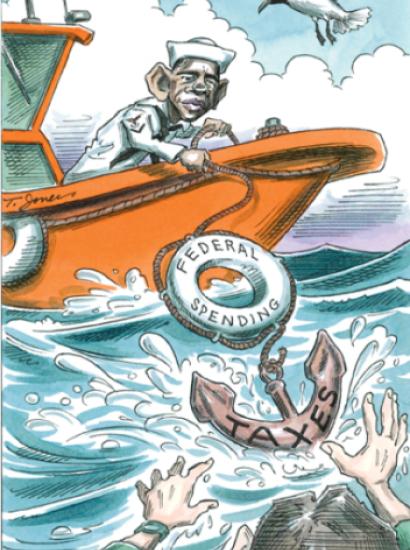

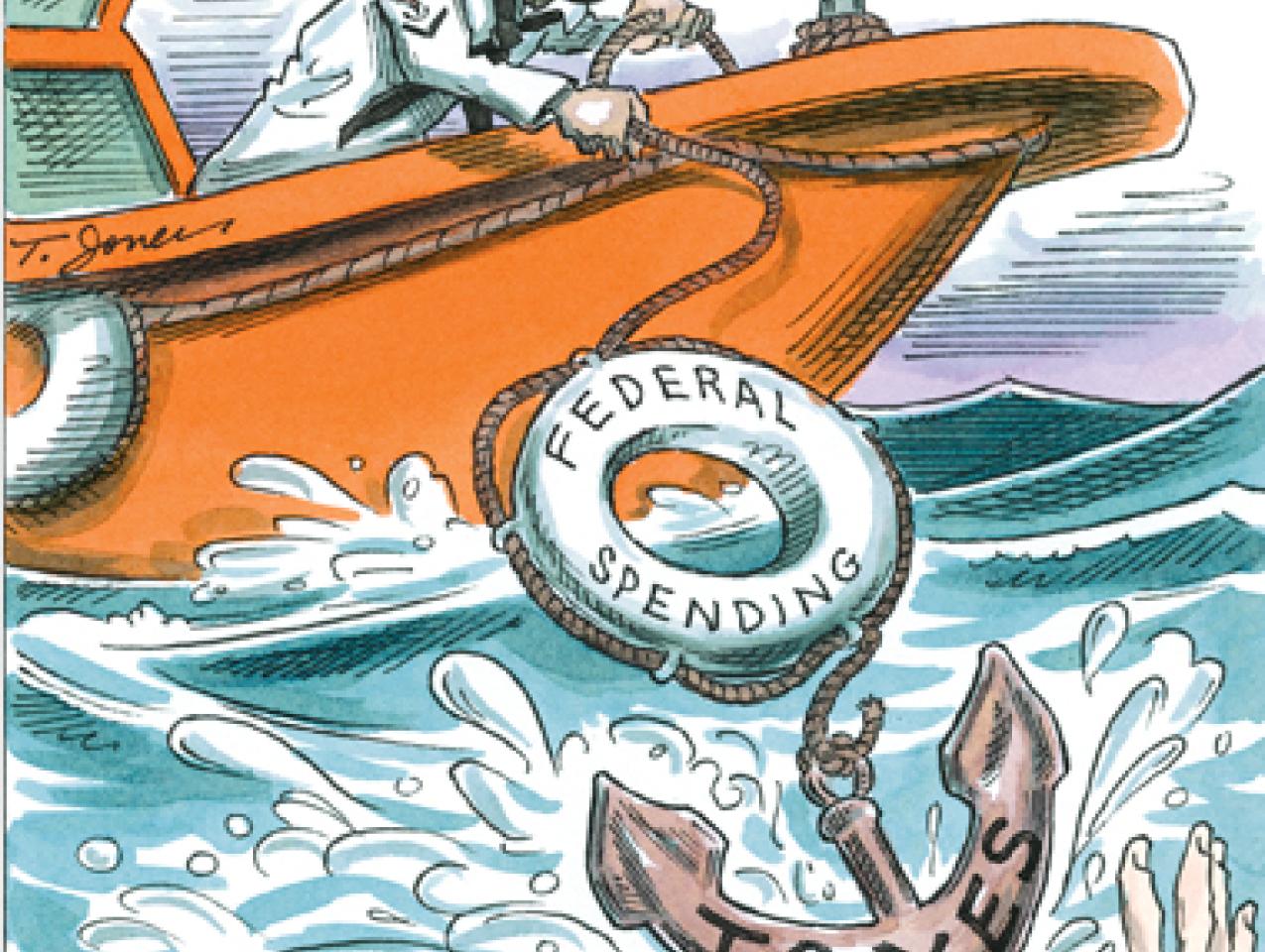

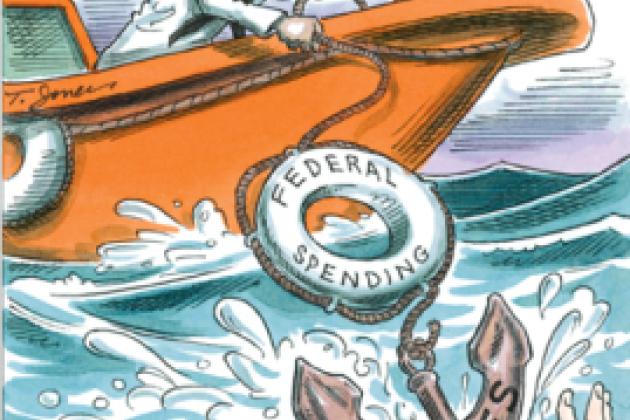

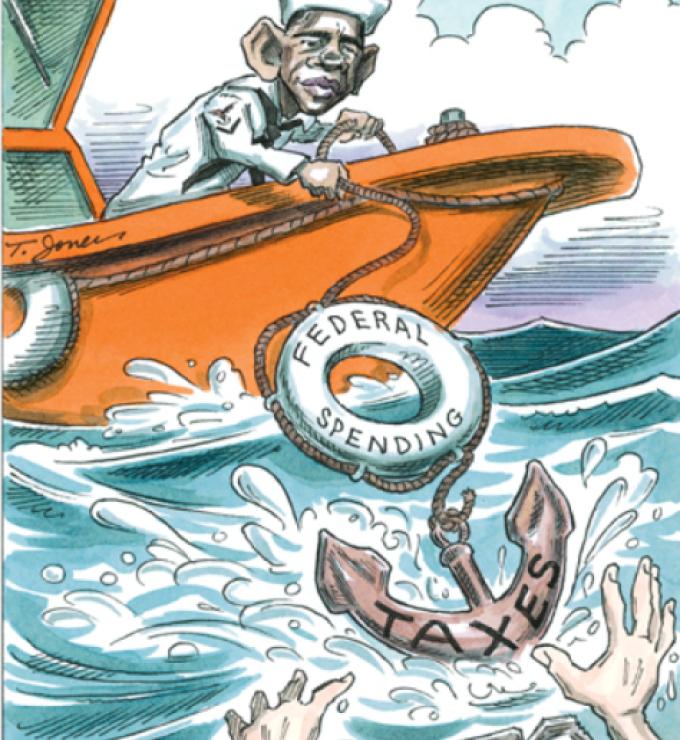

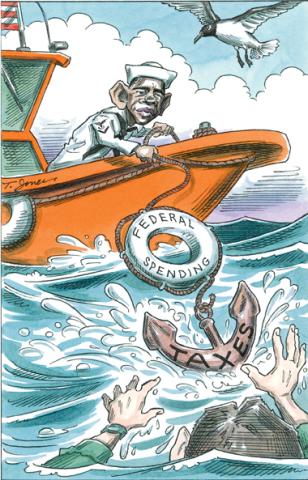

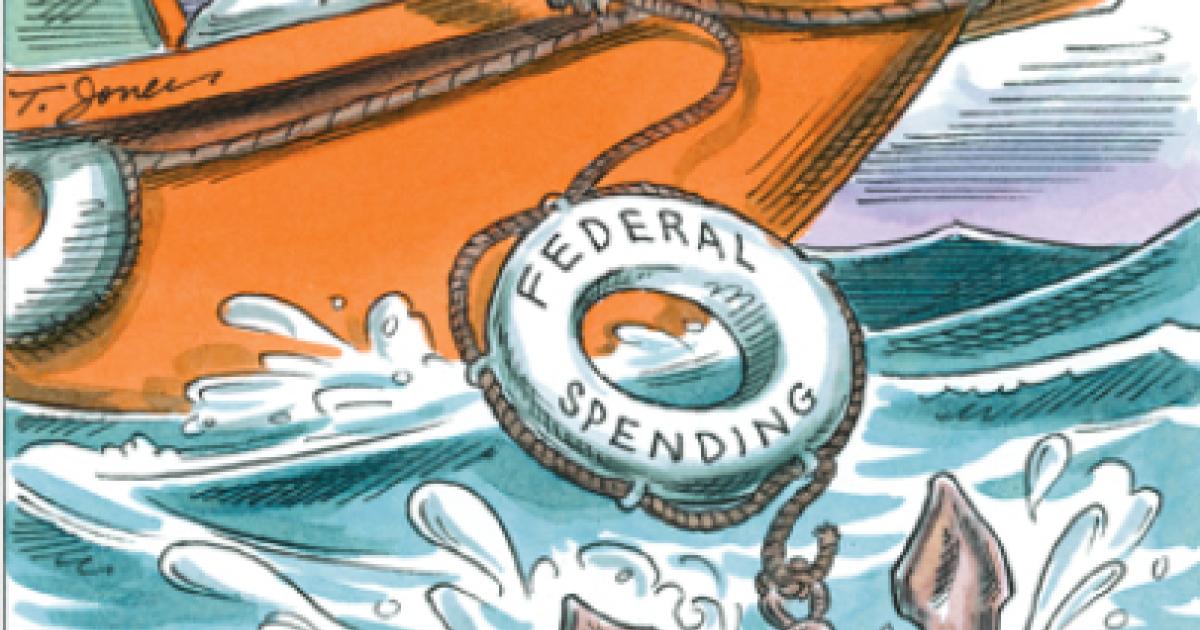

The economy has finally started to grow, but the disturbingly high unemployment rate is increasing pressure from the left to double down on the fiscal stimulus originally sold, if not well designed, to “create jobs.” After the stimulus bill was signed, the ranks of the unemployed grew by more than 3 million (4 million, if involuntary part-time and discouraged workers are included). The national unemployment rate, which the Obama administration projected the stimulus would contain to 8 percent, was 10 percent as of December. Meanwhile, the president and congressional leadership stampede legislation that would destroy even more private sector jobs.

There is little likelihood that another round of similar fiscal stimulus would yield much more than the paltry return on the first one. The original transfer payments and tax rebates barely nudged consumer spending, and the federal spending has been painfully slow. The delayed infrastructure spending—the shovels are still in the shed—will have a bigger impact, though less than claimed. Some of the funds to state and local government did reduce layoffs. But as an explanation for the improvement in the economy and slower deterioration of the labor market since the depths of the recession, the stimulus bill surely ranks dead last behind the natural dynamics of the business cycle, the Fed’s zero-interest-rate policy and (partially successful) quantitative easing, and the automatic stabilizers in the tax code that have reduced taxes proportionally more than income.

But to evaluate the stimulus properly we should consider not just what we got for the $787 billion (job gains minus losses, and the value of the goods produced versus the negative impact of future tax hikes to service the debt) but also the effects of alternative policies that might have been enacted—there is no stimulus free lunch.

JOB CREATION SLUGGISH, HIGHER TAXES ON THE WAY

My Stanford colleague Pete Klenow and University of Rochester economist Mark Bils estimated that cutting the payroll tax by 6 percentage points (of the 12.4 percent Social Security component) would, under standard assumptions, increase employment by 3 million to 4 million workers, an amount equal to all the job losses since the stimulus was passed. The employer tax cut would have reduced business firms’ costs by roughly the same amount as from the entire decline in employment. A cut in both the employer and employee components of the payroll tax stimulates employment under a wide range of alternative views of why recessions occur and how the economy responds to policy. It would have cost less than half as much as the stimulus, gotten far more income into paychecks quickly, and, most important, greatly reduced incentives for firms to lay off workers. In fact, it would have created increased incentives to hire and work.

Even using the administration’s claim of 1 million jobs “created or saved,” the stimulus program passed last February is millions of jobs short of what a cheaper payroll tax suspension would have delivered. Three times as many jobs—many of them more permanent, making the highest use of the value of the labor, and not dead-end, low-value stimulus jobs—could have been created for half the cost per job. That is a tragic wasted opportunity.

But worse yet, the president and Congress are preparing vast new taxes on employment in the health care reform program and other legislation. Raising the top federal tax rate to 45 percent (from the current 35 percent with a 5.4 percent surcharge plus the expiration of the Bush tax cuts) will hit successful small businesses especially hard. Its hidden tax hike on capital gains and dividends also will raise the cost of equity capital, further weakening businesses (including banks) desperate for private capital to avoid further retrenchment. Many firms will also either face an 8 percent additional payroll tax or be forced to pay a higher share of health insurance premiums. Such tax increases will hit employment and wages hard.

It would be far better to junk part of the remaining stimulus in favor of a one-year partial cut in the payroll tax. At the same time, we should accelerate spending that will need to be done eventually, such as replenishing military equipment used up in Iraq and Afghanistan and adding a desperately needed two Army brigades. That would create spending in America and jobs for the unemployed. Some stimulus funds, on the contrary, would be leaked to imports and spur hiring that only diverted workers from other jobs.

There are five large, interrelated headwinds to jobs and growth:

- Continued deleveraging, unresolved toxic assets, and weak banks are constraining credit, especially for small business, which is the source of most hiring.

- Household balance sheets, depressed from declines in home values and portfolios, are likely to constrain consumption growth.

- Government industrial-policy micromanagement with subsidies, investment, and mandates from pay to products is forcing noncommercial decisions on wide swaths of the economy, from financial services and autos to energy and health care. Such policies have never worked before—ask the Japanese, Koreans, or Europeans.

- The explosion of spending, deficits, and debt foreshadows even higher prospective taxes on work, saving, investment, and employment, which not only will damage our economic future but is harming jobs and growth now.

- The massive liquidity injections by the Fed raise the specter of future inflation.

ROOTING OUT JOB-KILLERS AND EMERGENCY MEASURES

What is by far the best response to these headwinds? Curtail the huge current and contemplated future government control of the economy with a clear, predictable exit strategy, before the programs become permanently entrenched, develop powerful dependent constituencies, and greatly increase the risk of rising interest rates, inflation, and taxation. Doing so would more rapidly improve the outlook for permanent private sector employment, investment, and growth than any conceivable second stimulus. It would also allocate capital and labor to their highest value in providing goods and services that people actually want and need, not what government bureaucrats want them to have.

The jobs agenda must begin with a Hippocratic oath: first, do no harm to employment. That means jettisoning, or at least delaying, job-killing energy and health care legislation with their mandates, taxes, and costs that especially hammer small businesses; stopping the impending large tax hikes; and controlling spending, deficits, and debt as the economy returns to health.

We also need to wind down, as soon as possible, the emergency measures that healthy businesses, households, and investors fear will become permanent competitive impediments. Start with TARP, which the Treasury uses as a permanent revolving fund even for non-financial bailouts.

Financial regulation should focus on disclosure, transparency, effective clearing, capital adequacy, and new bankruptcy procedures. We also need a Plan B, modeled on the Resolution Trust Corporation cleanup of the savings and loans, in the event that the losses on toxic assets are too large for time, profitability, and economic recovery to manage. And the Fed must forestall future inflation by withdrawing its immense liquidity injections in favor of private extension of credit as soon and predictably as feasible (its initial steps are commendable).

Finally, if possible, we should complement these pro-employment policies with long-run fiscal reform: control the growth of entitlement costs (for example, with price rather than wage indexing of Social Security) and enact real tax reform, with the widest possible tax bases and lowest possible rates. (Especially damaging is America’s high corporate tax rate, the second-highest among advanced economies.)

These are the ingredients of a far more consistent, commonsense recipe for more and better jobs—and far sooner—than the current contradictory, ineffective, at times economically illiterate policy mess emanating from Washington.