- Economics

- Monetary Policy

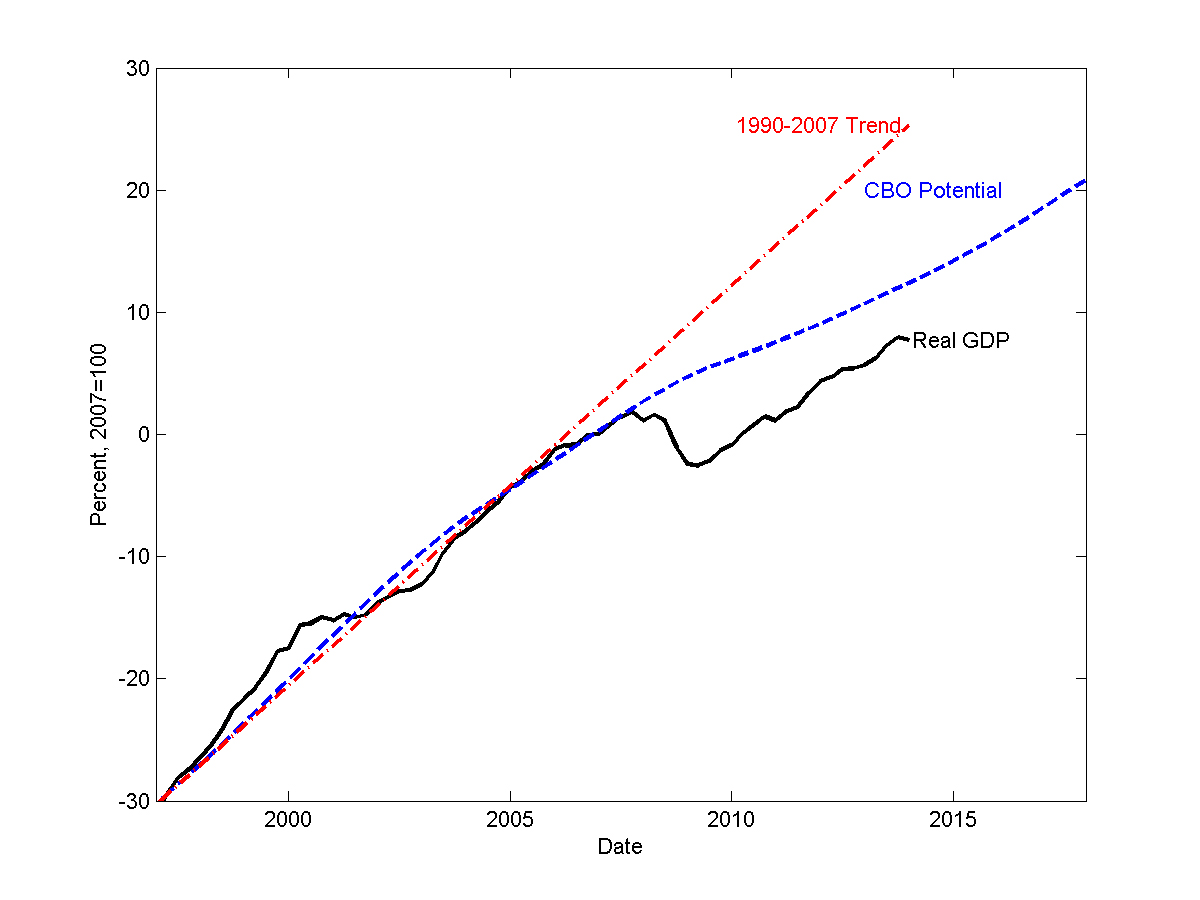

Output per capita fell almost 10 percentage points below trend in the 2008 recession. It has since grown at less than 1.5%, and lost more ground relative to trend. Cumulative losses are many trillions of dollars, and growing. And the latest GDP report disappoints again, declining in the first quarter.

Sclerotic growth trumps every other economic problem. Without strong growth, our children and grandchildren will not see the great rise in health and living standards that we enjoy relative to our parents and grandparents. Without growth, our government's already questionable ability to pay for health care, retirement and its debt evaporate. Without growth, the lot of the unfortunate will not improve. Without growth, U.S. military strength and our influence abroad must fade.

Prominent macroeconomists of all stripes bemoan our slow growth. Stanford's Robert Hall calls the years since 2007 "a macroeconomic disaster for the United States of a magnitude unprecedented since the Great Depression." Describing our current situation, Harvard's Larry Summers (an Obama adviser) or Princeton's Paul Krugman sound a lot like Mr. Hall, Stanford's Ed Lazear and John Taylor (both of whom served in the George W. Bush administration) or Arizona State's Ed Prescott.

Where macroeconomists differ, sharply, is on the causes of the post-recession slump and which policies might cure it. Broadly speaking, is the slump a lack of "demand," which monetary or fiscal stimulus can address, or one of structural sand-in-the gears that stimulus won't fix?

The "demand" side initially cited New Keynesian macroeconomic models. In this view, the economy requires a sharply negative real (after inflation) rate of interest. But inflation is only 2%, and the Federal Reserve cannot lower interest rates below zero. Thus the current negative 2% real rate is too high, inducing people to save too much and spend too little.

New Keynesian models have also produced attractively magical policy predictions. Government spending, even if financed by taxes, and even if completely wasted, raises GDP. Larry Summers and Berkeley's Brad DeLong write of a multiplier so large that spending generates enough taxes to pay for itself. Paul Krugman writes that even the "broken windows fallacy ceases to be a fallacy," because replacing windows "can stimulate spending and raise employment."

If you look hard at New-Keynesian models, however, this diagnosis and these policy predictions are fragile. There are many ways to generate the models' predictions for GDP, employment and inflation from their underlying assumptions about how people behave. Some predict outsize multipliers and revive the broken-window fallacy. Others generate normal policy predictions—small multipliers and costly broken windows. None produces our steady low-inflation slump as a "demand" failure.

These problems are recognized, and now academics such as Brown University's Gauti Eggertsson and Neil Mehrotra are busy tweaking the models to address them. Good. But models that someone might get to work in the future are not ready to drive trillions of dollars of public expenditure.

The reaction in policy circles to these problems is instead a full-on retreat, not just from the admirable rigor of New Keynesian modeling, but from the attempt to make economics scientific at all.

Messrs. DeLong and Summers and Johns Hopkins's Laurence Ball capture this feeling well, writing in a recent paper that "the appropriate new thinking is largely old thinking: traditional Keynesian ideas of the 1930s to 1960s." That is, from before the 1960s when Keynesian thinking was quantified, fed into computers and checked against data; and before the 1970s, when that check failed, and other economists built new and more coherent models. Paul Krugman likewise rails against "generations of economists" who are "viewing the world through a haze of equations."

Well, maybe they're right. Social sciences can go off the rails for 50 years. I think Keynesian economics did just that. But if economics is as ephemeral as philosophy or literature, then it cannot don the mantle of scientific expertise to demand trillions of public expenditure.

The climate policy establishment also wants to spend trillions of dollars, and cites scientific literature, imperfect and contentious as that literature may be. Imagine how much less persuasive they would be if they instead denied published climate science since 1975 and bemoaned climate models' "haze of equations"; if they told us to go back to the complex writings of a weather guru from the 1930s Dustbowl, as they interpret his writings. That's the current argument for fiscal stimulus.

In the alternative view, a lack of "demand" is no longer the problem. Financial observers now worry about "reach for yield" and "asset bubbles." House prices are up. Inflation is steady. The Federal Reserve evidently agrees, since it is talking about taper and exit, not more stimulus. Even super-Keynesians note that five years of slump have let physical and human capital decay, which "demand" will not quickly reverse. But we are stuck in low gear. Though unemployment rates are returning to normal, many people are not even looking for work.

Where, instead, are the problems? John Taylor, Stanford's Nick Bloom and Chicago Booth's Steve Davis see the uncertainty induced by seat-of-the-pants policy at fault. Who wants to hire, lend or invest when the next stroke of the presidential pen or Justice Department witch hunt can undo all the hard work? Ed Prescott emphasizes large distorting taxes and intrusive regulations. The University of Chicago's Casey Mulligan deconstructs the unintended disincentives of social programs. And so forth. These problems did not cause the recession. But they are worse now, and they can impede recovery and retard growth.

These views are a lot less sexy than a unicausal "demand," fixable by simple, magic-bullet policies. They require us to do the hard work of fixing the things we all agree need fixing: our tax code, our cronyist regulatory state, our welter of anticompetitive and anti-innovative protections, education, immigration, social program disincentives, and so on. They require "structural reform," not "stimulus," in policy lingo.

But congratulate all sides for emphasizing that slow growth is the burning problem—though Washington seems to have forgotten about it—and that slow growth represents a self-inflicted wound, not an inevitability to be suffered.

Mr. Cochrane is professor of finance at the University of Chicago, a senior fellow of the Hoover Institution, and an adjunct scholar of the Cato Institute.