- Finance & Banking

- Economics

- Answering Challenges to Advanced Economies

- Revitalizing American Institutions

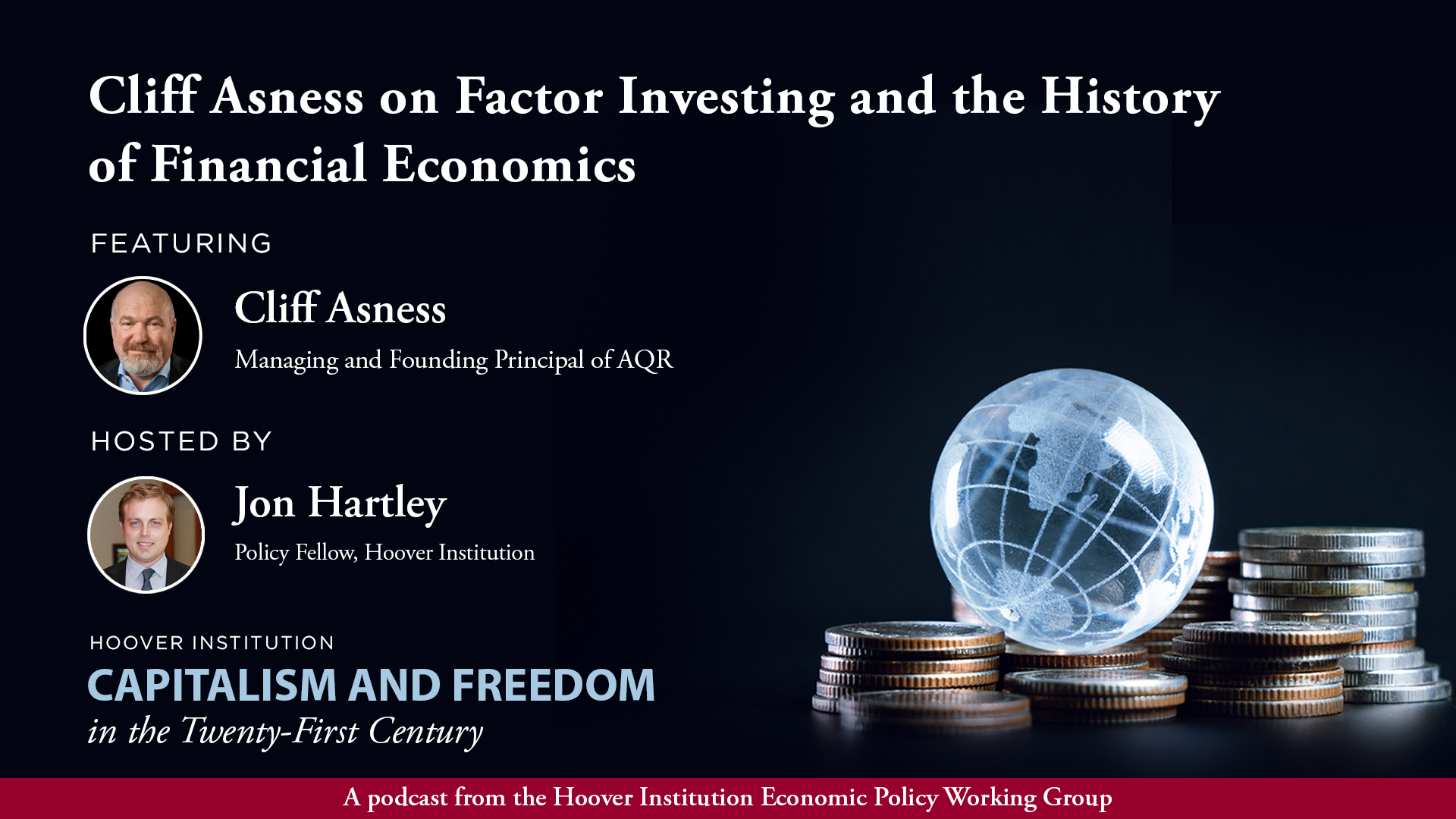

Jon Hartley and Cliff Asness discuss his time as a graduate student under Eugene Fama at the University of Chicago, his career at Goldman Sachs, and founding AQR, factor-based investing (value and momentum), the efficient markets hypothesis, the elastic markets hypothesis, inelastic markets hypothesis, comparisons between private equity and public equity returns, and more.

Recorded on August 27, 2025.

- This is the Capitalism and Freedom in the 21st Century podcast and official podcast of the Hoover Institution Economic Policy Working Group, where we talk about economics, markets, and public policy. I'm Jon Hartley, your host Today. My guest is Cliff Asness, who is the co-founder and managing partner of a QR Capital Management, a quantitative investment manager. Cliff also is a PhD in finance from the University of Chicago Blue School of Business, where he studied under the Nobel Prize winner, Eugene Fama as well. And he's here to talk all about asset pricing and financial and economics. Welcome Cliff.

- Thank you, Jon. Thank you for having me.

- Well, it's a real honor to have you on and really wanna get into, start with getting into your earlier, early career. Where did you grow up and how did you first get interested in economics and finance?

- I was born in Queens, New York. At four, we moved out to suburbia on Long Island and I grew up in, you know, post World War II suburban housing out there. I was not interested in finance for a while. I was kind of a only half engaged high school student. Mediocre grades, good boards. Ended up, my father found this program at the University of Pennsylvania where you got a dual degree. You got a degree in from the engineering school and from the business school. He said, you should do this. You have no clue what you want to do. So study two things that was about the depth of it. I went there, it, it actually was not me. I was not a young, you know, read the Wall Street Journal trade stocks at the age of seven. It wasn't until I took one or two finance classes as part of the Wharton curriculum that I was like, this stuff's pretty cool. So I, I got interested in a very boring way. I took the classes and, and liked them though my dad, again influenced my career a lot because I had always assumed that even though I was studying two fairly mathematical topics, that I would go to law school. 'cause my dad was a lawyer. I had several uncles who were lawyers. And at some point around junior year, I actually registered for the LSATs and my dad said, what are you crazy? None of us can add you, can you do math? You should do something with math. And I switched it to the GMATs and ended up at the University of Chicago's PhD program.

- Wow. Wow. That that's that's fantastic. And, and I know, so, so you went to Wharton as Penn Wharton signed engineering and, and finances while Wharton and I think, I don't know if they called it m and t program.

- They did. It was the early days of the program. It,

- It still exists and is a, a very, a well-known program that that, that, you know, is a super selected program that, that, that students go through. And my understanding is that you also met your, you know, great longtime friend John Byner who would go to Goldman Sachs and you'd kind of meet up with, with later and he'd go on to run the fixed income group at Goldman Sachs Asset Management for, for many years. You went on to U Chicago for your PhD and you saw you fi finished economics under f what was studying with f like, and, and it's just around my guess the 1980s and, and what, you know, what was U Chicago like at that time, what was in the air at that time? And my guess is there were so many Nobel Prize winners at the time and, and many of, so the, you know, the so-called Chicago school were around at that time. And my sense is in, in financial economics side of things too, a good number of folks that that intersected there as well. I'm, I'm curious what was, what was in the year when you were there?

- It was amazing time to be there. I I, I, I think historically there've been a lot of amazing times to be at the University of Chicago studying economics or, or finance. But for me, I always point out that my entire career was, was in some sense a lucky break because I got there in the, in the late 1980s. I think I showed up in fall of 88. And that was basically just when f and French were doing their first paper on the cross section of expected stock returns. It was probably a working paper at that point. I don't remember exactly. I could be off by a year or so in my stories. I'm getting very old. But I was essentially there when what we'll today call factor investing, what we might call systematic value momentum, systematic momentum investing. I was there at the infancy and that's al there's always some luck to, to these things. And even when you look back, it's funny terms like value investing terms like, like factor investing. We didn't use those terms back then. Factor investing came much later. I'm pretty sure the first couple of f and French papers didn't call like their price to book factor value. I think that came later. But when you have some amazing teachers, fam and French were co-chair of my co-chairs of my dissertation. I think you're sitting in John Cochrane's office. He was on the outside committee of my, my, my dissertation. When you have these amazing teachers and they happen to be breaking ground on what will be probably the major field of academic finance for the next 20, 30 years, you've gotta consider yourself pretty, pretty lucky. So it was a pretty amazing place to be

- Now, you know, to be there at that time. I'm sure it's incredibly, you know, farmer French factors are, are sort of new that, you know, those eventually published in the, in, in, I think the JFE in 1993. I'm curious who else was also crossing paths with you at that time? You know, I think, you know, when we talk about momentum investing, you know, mark Carhartt, a fellow Fama student was was was their PhD student, Ray Romanowski. I mean these are all people that you hired later, but I'm curious who else was there Maybe at the time, obviously Fama was working with Dimensional Point advisors and David Booth and, and others. Yeah. But you know, Dan Iveson, man Roman went through booths in, in around that same time as well. I mean, did, did you know any of these other people that sort of also like yourself would go on to if they hadn't already started them at the time? Go on to start these massive, massive, you know, multi-billion dollar asset managers?

- Sure. Mark and Ray, again, my memory's fuzzy. I'm pretty sure I knew Ray and I think I knew Mark in, in the program, or at least I, I knew him through mutual friends. You know, I mean you're a PhD student, you know, a few years into the program, you're not quite in all the same classes together. And I was a few years ahead of them. Mark and I have an intimate connection, not just hiring him, but the momentum factor that I wrote my dissertation on, he included in what became a four factor model when he analyzed mutual funds. So, so we have that connection. And later on in my group at Goldman Sachs, I hired Mark and Ray Ross Stevens was two years behind me in the program. I think it was two years. And I was his official mentor. Somehow I agreed to do that. I didn't even know Ross. I, I, I don't, I don't think I mentored anyone else. But Ross has built an amazing business at, at, at Stone Ridge. So, so he was there. A lot of, you know, big name academics were still there. Merton Miller was still there. I didn't, I I didn't really know Merton until I went to defend my, or propose my dissertation. Scary time to meet Merton when you're presenting your dissertation. And it was amazing. I'm sure a lot of people have the same memory, but the finance seminar was like Tuesday, late afternoon at the University of Chicago. And it, people sat in the whole u and you were at the front and on the far, far right, Fama sat and on the far far left, Merton sat and Merton got into my dissertation. It ended up being very good. It was nerve wracking, but, but he, he, he, he liked it. But I'm going back and forth. It was like a tennis game where my neck was, was in trouble at one point. Merton is asking a pretty hard question and Fama is answering it for me. 'cause he's read my paper 20 times at that point. And I started to interrupt to answer it my way. And I had a moment of clarity, thank God, where I'm like, I'm not gonna interrupt Eugene Fama as he answers the questions for me. So it was a pretty heady time to be at Chicago. Auntie Elman in, who's one of my partners at A QR was my year in in the program. My two co-founders of a QR John Liu and, and Robert Krall were one year behind me in the program. And, and I don't think I met Bob physically there, I think I met him later on through probably John or Ross. But Jon, John and Ross ended up being my first two hires at Goldman Sachs, along with Brian Hurst, who was our analyst. And, and then Bob and John ended up leaving Goldman with me to start a QR. So it's fair to say Chicago was, was responsible for an incredible number of good things in my life.

- That, that's fantastic. And, and I guess like, you know, just to close the thread on, on sort the Chicago years, like when you were presenting, you know, your dissertation on momentum and I, I think this was maybe at the time when yourself and, and your, she and Tim Timon when sort of, you know, momentum was on the left hand side, you know, the equation. And then I think, you know, mark sort of brought on our, to be one of the right factors

- That's well put

- With, with the, you know, four factor model. Like was there an aversion to that? You know, I think of Chicago and Fama as sort of being very risk-based into risk-based factors and you know, momentum never really squares neatly into, you know, this idea that, you know, stocks that have outperformed when we say momentum for the listeners not there, that aren't familiar with momentum means, you know, stocks that have outperformed in the past 12 months are gonna continue to outperform. Those that underperform in the past 12 months are gonna continue to underperform. I mean that, that sort of doesn't really fit into the standard sort of rational Sure. Factors of, you know, value and size that are the, you know, former French factors. Was there a version to, to this or in a truly Chicago Iconoclast way or, or we, we,

- It's a great, it's a great question because as I'm, I'm finding these things and I should say Jish and Tipman deserve pride of place. I was probably only about six months behind them, which I will regret forever. But I, I think they, you know, we should say that I think they're the discoverers. I mean people were trading momentum and, and actual Wall Street forever, but the academic kind of formal discoverers, I think my version of it was a better formation. I'll give myself that. But they, they, they deserve that. I was actually nervous about telling Gene who I'd never, I still today have trouble calling him Gene, he tells me too all the time, and it's Professor Fama, I'm much more comfortable with that. But I was nervous going to tell Professor Fama that I wanna write a dissertation wasn't only on momentum, but that I was including this result in a, in a, in a fairly prominent way. And it, I distinctly remember telling him, I wanna study price momentum for choosing individual stocks and cowardly mumbling. The second part that it works very well. 'cause you're right instinctively, you know, for any so-called factor, a factor is if you sort stocks or other assets. But we always think about stocks first. If you sort stocks on this characteristic, the ones at one end of the sort tend outperform ones at the other end of the sort. For any factor that you believe works, there are always two possible explanations and efficient market story where the ones that are attractive on that factor are in some sense as a portfolio, not individuals riskier than the other ones. And therefore you get a return premium for bearing risk. The other is a market inefficiency explanation where, you know, it's not really a formal kind of measure of risk, it's a bias. People have an error they're making, taking the other side of errors can still be risky in the short term, but it's not a, a so-called price risk. It's not correlated in co varying with some stochastic discount factor that we care about. You can come up with a risk or a behavioral explanation for any of these factors. The plausibility I've always found, and I think the industry would agree with me, the plausibility of a risk-based explanation for momentum. It's pretty hard to swallow. It's pretty hard to swallow. I think I, I think probably also trying to appease a curry favor with Fama. I think I called it the fool strategy when I started just buy what's going up and sell, what's going down it people have tried, I've never seen a very satisfactory, oh, this as a portfolio represents risk. It has a bad left tail, but that left tail seems to be, if anything, a negative beta, not a positive beta. I've never seen, I've never seen a really good story for that. But I'm telling f and I mumbled the second part and he hears me, he prob actually I think he probably made me repeat it once, but, so I say I wanna study price momentum and I, I find it works very well and he pauses for a second and this still had a profound impact on me. It was a very cool moment. He just goes, if it's in the data, write the paper, which is about as close to a religious statement you can get at a, at a Fama. That man's respect for data, no matter what his prior might be is, is extreme. And it's, it's, it's, it's actually, it's actually very a great role model. I think he'll be the first to tell you he never has liked that momentum works. I think he's called it the, the, the principle black mark on their kind of three and ultimately five factor models. But he doesn't deny the, the historical results if it's in the data. Fama wants you to write the paper. So that was a scary moment as you intuited that it might be. But it ended up being quite a warm and, and nice moment for me.

- That's, that's fantastic and amazing to hear about, about Fama. I'm curious, so you know, you're a PhD student in, you know, your later years. Were you ever thinking about becoming a professor or you just knew that you wanted to sort of apply all this to, to

- No, no. I, when I entered the PhD program, I assumed I was gonna be a professor. I, I got slowly seduced to what you might call the dark side. You mentioned my friend John Byner. I should explain why you mentioned him 'cause you also worked at Goldman Sachs Asset Management where, where John ran fixed income for many years. He was much more junior in 1991 when John and a few other people I knew working there offered me a summer job. I was still a PhD student and it was come for the summer, see what you think. I went there, I had a fun summer and they said, come for a year you can work on your dissertation part-time. See, see if you like it. And I did that. And at the end of the year, maybe it was, maybe it stretched to more like a year and a half. I still hadn't really decided when, again, dumb luck. Any story that you think ends well and I hope it's not the end of my story, but I hope, I hope it has gone well. Any story that has gone well has a lot of luck along the way and I'm, I always try to be humble about that. Pimco, the West Coast, you know, most known for fixed income, huge respected money manager. Read the first piece I wrote in the Journal of Portfolio Management. It had the exciting title option, adjusted spreads and a steep yield curve. The movie version has yet to be made. But they, they liked the paper, ended up calling me and said, would you be interested in coming out and starting a quant group for us? And I did talk to them. They offered, they actually did offer me a job. And I, I was incredibly naively honest. I I I walked up to my superiors at Goldman and I said, I think I lucked into this, but I think this is what I wanna do. I can, I can pursue the academic stuff that I really have grown to love and I can see if it works in the real world. Which I found very attractive. And I will have to admit, I did notice that if it works in the real world, you, you probably make a little more money than a professor makes. And someone who says they chose Goldman Sachs over being an academic and doesn't kind of admit that was at least part of the equation for them is probably not telling the full truth. And my, my, the partners I reported to said, Hey, we're looking to start a group like this and to this day I'm not a hundred percent sure that was true or if they were just really opportunistic and quick on their feet. I think it was probably true. I, I think there, I got lucky again, this'll really date the story because this did not end well. But I think Goldman wanted to start a group doing this, having really no idea what this group would because of the then success of the hedge fund, long-term capital about 6, 7, 8 years later, 1998. That did not end so, so, so pleasantly. But they helped, they helped me out a lot in my life. 'cause Goldman I think was like, these guys are making a ton of money. They're academics applying their stuff to Wall Street, you know, cliff, why don't you try to do that here? And we didn't do very similar things to long-term capital. But I I I told Fama in French, I I think I'm gonna stay and do this. This is perfect. Fama was not happy with my choice. He wanted me to go on the academic job market and it still saddens me. 'cause I love f and I didn't wanna make him, you know, I didn't wanna cause unhappiness. I do take it as a bit of a compliment that he was, that he was upset if he, if he thought I wouldn't be a good academic, he, he wouldn't have been upset. But I still remember his comment to me. I told him, I think I'm gonna stay at Goldman Sachs and build this group. And he just goes, why do you wanna stay and be a salesman? And it was very Fama que comment, you know, if I, and I was, I I would never say this to Gene if he hears this podcast, I'm saying it now. I I was thinking you guys work with DFA, right? You, you, you do this and I'm just gonna do it from over, over there. So there are points on a spectrum. But yeah, I saw the opportunity to pursue the academic stuff, trade it in the real world and, and, and, and do really well if it, if it worked

- Well, I'm just curious, I mean like how Goldman was set up at the time. I mean, my sort of sense of things, understanding a bit of the history is that, you know, Goldman was a big innovator at that time in the sense that, you know, there, there were people there like Fisher Black, like Bob Litman that were in the fixed income research group. This was sort of even before Goldman Sachs asset management came to be, I think in the early 1990s. And and I, that's kind of where yourself and, and, and John Byner and, and Charmine Ma Armani and all these other folks kind of come in. But I mean the fact that you, you know, one of the sort of co-founders of the Black Shoals, you know, Merton model was, was at Goldman. You know, the the, we talk a lot about black Letterman optimization, you know, still being used in in portfolio management. I mean Goldman Sachs, you know, at that time was, you know, a hugely innovative environment. It totally makes sense that, you know, young CLS would wanna work there and to, to this day you're still writing academic papers. So, so it it never stopped you from, from doing research as well?

- No, no. And that was a major attraction of it. The ability to fuse both worlds. Who was who and who was where is a bit complicated. Bob Litman was on the sell side, not on the asset manager side at the time. He actually came over when I left to run my group actually in a broader role than I had to run my group among other things. But he moved to asset management. I think it's a direct response to, to myself and a few other of our member, our group leaving Fisher Black being there was some of the, again, dumb luck in my life. I got to spend a lot of time with Fisher. He was really a sounding board. He wasn't building models with us. I remember one time I was showing him one of our early models and he kept calling it a DM model and I, I kept thinking he meant Deutschemark because they used to be a Deutschemark and he actually meant is it to Data Mind? And I didn't, you know, he was using it as a shorthand. But Fisher was, was was great. One of the Fisher stories I love is he wrote a paper that was quite critical of some of Fama and French's early work. And his first line of the paper was Fama and French misinterpret their own data. I could be slightly off on that, but I'm getting very close. He only thanked a tiny group of people, including me. And from the bad luck of alphabetical order, I'm the first one thanked. I am not done with my dissertation yet for Fama and French. So I, I should have given them more credit. But I call up Ken as soon as I saw it and I say, you know, I gave Fisher some comments, but I don't agree that he that with, with that, that you're misinterpreting your own data. And Ken was like, we know Fisher, don't worry, don't worry. 'cause Fisher was absolutely brilliant, suffered from less groupthink than anyone I've ever met. Emperor always had no clothes for him. He is always willing to say it, but I will say nine outta 10 things. He said, were a little, this, this is very disrespectful, but were a little wacky sometimes. The 10th one was brilliant and nobody ever thought of it and it was well worth the price of admission. But that, that, that did scare me. But now Litman was on the sell side, came over after I left. But we did use a version of Black Litman in building our, our, our process. So yeah, there was a guy, Bob Jones, who doesn't get enough credit in the quant world. Bob was running a quant equity product, again, I don't think we even called it factor investing, but doing a lot of the early stuff and some innovative new stuff of his own. And he was a very early practitioner of quantitative investing and he was there. So yeah, it certainly was not even close to just me. I was, I landed in a fertile environment

- That, that's fascinating. So, so my understanding is like you came in, you into the summer, you're working on fixed income stuff for the most part. And, and then this,

- The summer was fixed income when I came back for the year. It was fixed income while writing my dissertation on what we would now call quant equity, including momentum at night and on the weekends. That was

- A come by day quant equity by night.

- Yeah. Later it was probably the hardest, craziest time of my life except many years later. My wife and I had two sets of twins 18 months apart when I was building a QR. So that was a fairly similar crazy period just with a different nocturnal activity instead of, instead of writing, you know, laboring away at a keyboard at night, I was feeding and changing children. If, if my wife watches this, she's gonna go, you didn't change too many children, so let's, I might not send this one to her

- That, that's too funny. That's, so I guess it's fair to say what was quant equities always sort of your, your passionate and that was kind of what, what sort of led them to say, Hey, you know, cliff, we need you to start a quant equities group or a quant group in general. Also maybe do quant macro assets as well. And, and then that, that was where the impetus for starting these two groups, you know, I think one was called qd, one was called QAs and now I think it's still called quantitative investment strategies years later. But that was sort of the, the impetus for, for that

- You're giving us, you're giving us all way too much credit. It was not that well thought out. It was thought out at the level. I said before that other people seem to be making money with academic stuff. Let's see if Cliff can build a group to do that. The, in fact the way I remember it for the first, I don't know how many weeks we were kind of walking around a little nervous that we had nothing to do. We started a quant group and it was, and and, and to some extent nobody had a real plan for what we, I think they thought I had one and I thought they had one. And what happened, Bob Jones was doing the quant equity. We ended up doing a parallel effort, but we weren't gonna touch that early, early on he was doing a good job at it. There was a group run outta London non quants active, you know, concentrated stock pickers running a portfolio that had done well but had hit a very rough patch. And I think we did the performance attribution on them and it turned out that they were actually pretty good, at least ex post i, the statistical valid validity of this, I have no idea if we were, if, if, if we had a T statistic above 0.5, but in the performance attribution they had been good stock pickers country by country and always in the wrong countries. So the first thing Goldman asked us to do was this macro question, can you decide where in the world to invest using these quantitative methods? I think I said of course we can do that. Give us, give us some time. And then our four person group got in a tiny room and we said, how are we gonna do that? I said, of course before I had a clue embarrassingly, 'cause I think it's kind of obvious what we did, it took a little bit, but within a day or two we just said countries are just portfolios of individual stocks. This is childishly simple. If we aggregate up the numbers that people like pharma, French, my dissertation had been building factors on, if we aggregate them up for countries, if Germany is, is is double the price to earnings price to sales price to Book of France and has worse one year price momentum, you normally don't get that 'cause they're negatively correlated factors. But if that will do you expect Germany to do worse? And the answer of course was yes, this is a bit of a cooking show. I got the cake already baked in the back, I'm taking you through the steps, but I know how it turns out. And we built the tool that that that the active group did use. We, we ended up building it for stocks, bonds, and currencies using different factors. But they all were some version of value momentum or what we might today call a carry factor. What does it pay you if you, if nothing happens. But we also realized pretty quickly that we can give advice to the, to the active groups at Goldman, but we could also directly run money using these. So by, by near the end of 1994, Goldman Sachs seeded something called the Global Alpha Fund that used both macro and our version of what Bob Jones was doing. That we ran it separately of a quantitative equity model to run a series of long short strategies, long short country futures, long short bond futures, long short currencies, and then long short individual stocks within many of these countries. All with a goal to be market neutral, very aggressively targeting very high vol. And that grew into a lot of the things that that we did.

- That's, it's, it's an amazing history. And also just all the, I think all the people that I I my sense you helped hire and bring in, you know, people who are PhDs, you know, many of whom you know, I think folks and, and many of whom at University of Chicago, you know, at business school, I think Mark Carhart, Ray Romanowski, I think, you know, maybe George, you know, there's also

- Georgio was after me. Okay, mark and Ray hired Georgio when they took over when I left.

- Okay. Well then, then there's also, you know, Don Mulvihill, he was early, he was a University of Chicago guy as well, you know, built their big tax, tax loss harvesting strategy, which one of their largest strategies to this day. And and and many others, you know, who, who came to, you know, lead the group, you know, afterward, you know, think do Gary RAF and others. Yeah, yeah. I'm just so, you know, fast forward, I guess five years later, you know, the, the infancy of a QR, you started it in 1998. What John knew Robert Krall and, and, and Dave Kabil, some of these were classmates of yours and, and were working at, at Goldman Sachs as well. And what was the impetus for starting EQR and going out on, on your own and, and starting something totally de novo,

- 80% naked greed? I think, I think we did the math and said as well as you can do at Goldman Sachs, if you build your own asset manager, you do somewhat, you do somewhat better. Again, it's very similar to me telling you earlier that that that going to Goldman as opposed to academia had something to do with, with how well you do. It's just, just being honest. I think 20% was an early recognition on, on my part that I I don't always work and play well with others. That you can't say whatever you want at Goldman Sachs. You can't say whatever you want at a qr. Only I can a a a company has to have some, you know, if, if, if, if someone at a QR suddenly has an opinion that a product of ours isn't great, absolutely should tell us that we should debate it. But if they went out and submitted a paper on it without telling us, that would be upsetting. And I knew I wanted to be the guy who could could say and write what, what he wanted. Again, I'm not claiming some altruistic, this is, I'm giving you 20%, the 80% greed was still, was still there. But I think I I pretty early on, even though I loved Goldman, Goldman was very kind to me. I did well at Goldman. Realized that I, that I, that I was a guy who, who ultimately had to be on his own. And then David Caber still co-founding partner, still my my co-founder still active today. He deserves a lot of credit. At some points when we've had tough times, I I, I wanted to blame him, but on that credit, 'cause he spent the better part of a year convincing me that we, that that if we left and it became a we, it it could work, people would actually invest with us because I I was not the the as secure about the stuff as I am now. This notion that a bunch of people turning 30 could leave and attract capital. I had to be convinced of and David did convince me

- Well that that's that's fantastic and, and, and so great to hear. It's amazing. I mean a QR is amazing in how transparent it is in terms of its investment process in terms of the factors that you're using. And it's, it's amazing how many sort of public goods that you're sort of generating in, in doing research in, in, I think in many ways succeeding, you know, Goldman Sachs asset management just in terms of the, the amount of research and output that you're doing on, you know, on factors and various things. And, and a QR has been a real leader in this respect, in, in in factor investing and, and you know, some of the biggest factors I think that you're, you you've been focused on and as, as other investors have value, momentum, quality. I'm curious, you know, now in sort of the factor-based investing world, you know, there's been a lot of discussion about, you know, what factors have, you know, the greatest sort of relevance and, and sort of staying power, you know, A A QR is also, you know, taking the lead on on some new factors like invol, low volatility, bending against beta as a factor. I'm curious, where do you stand on your favorite factors?

- You know, it's, it's funny, we, this does not affect the weights we put on things. We've actually moved to a more systematic approach to weights. It looks at ins, sample out a sample data. So favorites, I would be terrified that someone would think I'm sitting around, you know, and, and just overriding all the data and saying, I kind of like this one. But I've always thought two of the originals, which still matter, they don't matter as much as they used to 'cause the models have grown. But the value and momentum stuff, I've often joked that it's a almost a, a rach test, almost a personality test. Someone's either wired to be a contrarian or to be a jump on the bandwagon person. And I, i, I can't test this, but I've always thought one of the harder parts of active stock picking is that these two things do really work and it's hard to keep both in your head at once 'cause you're wired for one or the other. You know, all else equal. I'm wired to be a contrarian in almost every part of my life. Sometimes excessively so, so favorite in maybe an emotional sense I'm at, at core a value guy. I don't think, certainly not today. I think in the past I've probably let that, let, that let me overweight it maybe even a little too much. We've certainly moved away from that over time. But if I had to have a favorite, I also love the fact that value, you know, can work for a host of different reasons. I think it was Ray Ball, I hope I have his first name right, who wrote a paper in the early days of factor investing who pointed out that value's kind of a catchall for expected returns. It can be behavioral, it could be risk premium, but for the same cash flows, if expected returns are higher, the multiples all equal lower. So it it, you know, the theoretical justification, no matter what the empiric now value of all the factors we trade value is probably the most episodic. Meaning it's not IID it goes through some long periods of being in favor and long periods of being out of favor. I think that's probably part of why it doesn't get arbitraged away. You know, after a lot of years marketing these things, I'm pretty good at turning a negative into a positive. But you know, the harder something is to do, the more plausible it is that not enough people do it to make it go away. So there's always good and bad news when you say something is hard to stick with. The bad news is it's hard to stick with the good news is that maybe why it doesn't go to zero. But, you know, I love, but I love momentum. I've never been as much a momentum guy even though it's somewhat one, one of the things I'm known for in academia is being, you know, after Jian Tipman very early in creating that, that is again, more emotional. That's a matter of personal preference. I used to do, I I finally stopped about a decade ago, but for the first like 20 years of doing this, I'd make the same annoying joke when people would bring me a trade that we were doing and I'd look and I'd go, are you telling me we're buying more of the Japanese yen because it is more expensive than it was last month? 'cause that's what momentum does. And often that would be more important than a valuation in the short run. And someone would look at me, they got the joke at some point, very deadpan and go, yes, that is what I'm telling you. And I'd be like, okay, I was just checking. 'cause you know, in the, in some fiber of my being, it just that, that would always just bug me. But being a value momentum, being a value investor without momentum would scare me because value does have, its, its its long dark periods as they said about Winston Churchill in the thirties in the wilderness. Betting against beta is is one of my favorite factors because the empirics are so strong and because the story is so beautiful, it's simply, it's a basic cap m story with restricted leverage where leverage is e people are either unwilling or it's too expensive to do and it leads directly to low beta stocks, which really help you in a world where you leverage the Ency portfolio. But if you're unwilling to do that, they're kind of orphans and it's a very, very sweet story that shows up in the data very nicely profitability. One of the quality factors I love because it's empirically so strong. I think it's one of the weaker theoretical stories. I don't have a great, frankly we'll do things for different combinations. We like to have both, but a super strong empirical story and, and and, and a less strong theoretical or common sense even story or vice versa can still get you in the, in in the process. You'll get more of a weight if you got both. I, I'm actually dating myself, we've changed to a more systematic approach. So that's, that's a little less true than it used to be, but I'm just gonna, I'm just gonna go with it. But you're asking one of my favorites. I love the empirical results in and out of sample of profitability. I've never liked the stories why you should get paid for buying more profitable companies. I've never seen anyone and I, I don't keep up with the academic literature quite as much as I used to, but I've still not seen anyone come up with a great theoretical story for why you should get paid for that. Though it's so strong empirically in so many different places it's passed the out sample test. So yeah, I have different loves and, and and, and, and ones I'm a little more queasy about. But again, we don't let my loves and queasiness matter. I don't think we ever let 'em dominate and we don't let 'em matter as much as they used to.

- Well, I I'm just curious a little bit about market time or, or sorry, factor timing, let's just say,

- Okay

- And you've, I think always, and correct me if I'm, I'm wrong, I've always sort of seen you as a critic of of factor timing a bit. And I'm just curious how investors should maybe think about periods where like traditional factors like value underperformed for over a decade or longer. Like obviously value in the US you know, has become, you know, bending against tech specific story, which, you know, if you've been doing that for the past 15 years, it's been a very difficult thing. Obviously, you know, you can do sector neutral sorts where you're doing, you know, you still have the same weight that you know the tech sector will have in the, in say the s and p 500, but then you'll, you know, within each sector, you know, you will pick stocks that have the most value. So you'd still have the same overall tech exposure for example, but you just would pick tech stocks as the most value. What do you think about that? I mean there's lots of STAAR people out there that are trying to time the market sort of in, in have various sort of market timing strategies. You know, when you have a big crash in the s and p and your expected returns go up. I'm just curious what you think about factor timing, market timing in general.

- You asked a ton of stuff in that question and I'm not gonna remember all of it. But first on the industry adjustment thing, the sector adjustment thing, I think we were the first to do that. Myself and Ross Stevens wrote a paper in 1995, never published, but you can still find on the SSRM and I think we get pride a place on showing that most factors, and I think value is particularly strong, do better if you do it within industries and don't take an industry bet that the apples to oranges, you know, to go to the extreme comparing tech to a textile on price to earnings. Are you ever gonna not be short tech and cannot be right to, to have a permanent bet? Momentum was the only one that had very similar power for, for both. And I think that's very intuitive 'cause there's no measurement problem. Momentum is momentum. It's, it's, it's return value has a big measurement problem. Does this, does this ratio mean the same thing for this industry as this other industry? So I do, I do have to brag for a second value. The, the simple farm and French definition price to book in the us I don't remember. It's on a certainly more than a decade, probably like a 15 year drawdown versions of value that are global, which fa and French do also. It's not a knock on them and they use more measures than just price to book and don't take that industry bet. The longest we've seen, which have been quite painful, have been kind of two and a half year drawdowns. Actually you're in drawdown for longer than that so you have to make it back. But two and a half year negative periods made back at about that same amount of time where multifactor processes are often not nearly as bad. Remember we, except if a client specifically wants one factor for some purpose they have, we're always trading a whole bunch of factors at once. So, you know, the value drawdown, the this, the simple version has been out of favor for a while though. I wrote a piece defending it just a couple years ago called The Long Run is lying to you. I mean to most people, 10 to 15 years is an eternity. If you ran a practical investment product doing only this 15 years later, only you and your mom are still invested and your mom has asked for the redemption papers, she wants to know kind of what the rules are for when she can get out. But in real life at modest sharp ratios, remember, you know, if we're trying to achieve a sharp ratio, call it one, and we have many, many factors in many, many countries, each individual one can't be close to one or otherwise we'd be a sharp ratio of five. So they're not giant in any single country. One factor is not a giant edge. So when you do the math, a standard deviation event, you know, if you're, if you're a 0.5, which is gigantic for a single factor, right? If you were 0.5 across tons of things, if you were 0.5, it takes less than a two standard deviation event to be down for a decade. So these things to a statistician are often much less shocking than they are to a, a real world person who has to go in in year nine and a half and say still down. The other thing is one thing I, I do think we pioneer, I'm bragging a lot on this call, you're bringing it outer me, but during the tech bubble in 99 we released the first to publicly do this. You never want to claim you're really the first 'cause we do things privately. We don't write about, we don't publish everything John, we only publish the things we think are mostly out there. So I gotta give other people the benefit of the doubt also. But we wrote a piece trying to measure the, the long term, not short term attractiveness of the value strategy and introduced this idea called the value spread that many others use now. And if you, if you go back and look at the academic papers, all the early work were sorts, ordinal sorts that built a portfolio of the better and went went short or underweight portfolio of, of of the worse. We asked the question particularly 'cause value is getting creamed for a year and a half. Okay, how extreme is it? And to our knowledge, at least publicly again, we were the first to say, alright, pick your favorite valuation ratio. We, we looked at multiple ones. If you, if you like price to sales, what's the price to sales of the cheap portfolio compared to the expensive one? Is it more different than it normally is or tighter than it normally is? And the idea is when there's bigger differences, when the expensive ones are at a much higher multiple than the, than the cheap ones than normal, they're always look more expensive, right? You created the measure, you sorted the stocks. If, if you sort on something the the ones that are higher will be higher but how much higher varies through time. And we did find that if you have a long horizon, you know three years is good, five years is even better, that there is some power to it. When that spread is larger things go on the, the value strategy will do better. When, when spreads are tight, the sharp ratio is lower. We also found, and here's an example of publishing, I'm still a little bitter about this one. An official a QR publication strategy is the perfect a QR publication strategy is you discover something you think no one else knows that has some alpha, you trade it for a decade and you write a paper on it a minute and a half before someone else is gonna write a paper on it 'cause it's gonna be out there anyway. Might as well get the credit. Obviously that's art, not science. And we've been trading the fact that factors themselves have momentum. They tend to trend for many years. And someone else wrote the paper and we were very, I was very angry that we, that we missed that one. We, we let someone sneak in before us. But that matters too. In the short run, fighting momentum is always a problem that this result repeats again and again and again. So never bet your life on factor timing. It's still particularly on an individual factor, pretty low risk adjusted return. But the perfect time to like any factor is when it looks quite cheap versus history. But when the last six to 12 months are starting to look pretty reasonable, you never like any value plus momentum strategy, you never nail the peak of the trough because you need to see it start to work. But because trend following is real, that's a higher sharp strategy. And when I've messed up in this field, it's when I found the valuation so attractive that I've said, ah, we gotta do a little even before the trend turns, turns out the trend is, has tended to still have efficacy. So I do think you shouldn't do much factor timing. I think most of your factor timing should actually be trend based, not valuation based. And valuation only gets interesting when you're at something I jokingly call the hundred 20th percentile. You're a guy who will understand sometimes I make that joke and people don't understand there is no such thing as the hundred 20th percentile, I mean like wider than you've ever seen before, but mostly don't do it. And to be totally fair, the times I've been most cynical about factor timing is when one of my frenemies, Rob Arnot, is very, very into it. Somehow when he writes something I, I instinctively take the other side too much 'cause Rob's a brilliant guy. So I have been a little schizophrenic on, on on factor timing. Historically we've, we've not been flighty in the portfolios. We've always done a little with some valuation and, and particularly trend following factor trends are just, we think they're real.

- Yeah. Well I'm curious just to maybe lightning round through a few of these topics that, that you've spoken a bit about fire

- Away.

- You know, one is, you know, in academia at least there's a bit of a a replication crisis and, and in fact research has I think suffered a bit in, in academic finding and it's not being published as much anymore. And I think a big question is, you know, what are the real factors and you know, to what, what's really PA what's sustainable and maybe one a factor discovered it's arbitraged away and people pile into it. I'm just curious, you know, what you think about factor research and, and how do we sort of dis over time build an understanding of what are the essential factors in the structure of prices?

- Sure. A again, you ask questions that I I could not do a lightning round. I can go on for a long time. You know, the literature well it's actually how big the replication crisis is in factor investing is a contentious topic. Las St. Peterson, Brian Kelly and i, I, they work with me so I i I think they had co-authored so I don't wanna imply it was just them. They take the, the, the view in their paper that the replication crisis is not that bad for one thing. I think some people hold it a hold replication to too high of a standard literally for close to 30 years. As a rough rule of thumb, we've said if we get half a back test going forward, we'll be thrilled. 'cause we know there's some p hacking and everything. I mean obviously there's some things you might wanna discount more, some you might wanna discount less. Not saying it's a be all end all half is a pretty cheap and easy kind of wimpy guess, you know, how many times in life do you just split the difference? But for, for at least we've been consistent in our wimpy guess that changes what you think of as success or failure by a lot against that standard. We find the results are fairly reasonable. I think value plus momentum has been about half of a back test since we've started looking at it. So we don't think it's quite that bad. But obviously data mining p hacking overfitting is a perennial issue when it comes to which factors are easier to arbitrage away. I think the hardest ones are ones, again, like the value factor that's based I think on basic risk or behavioral reasons and I've drifted more to the behavioral side over my career. I I think it's just proximity to Fama being away from Fama, I drift. And if I, if I walked into his office, I'd probably snap back into, into the risk side being a, a total coward to loves the man. But factors say, say value is based on behavioral errors people make. That means they're pretty deep behavioral errors over extrapolating good and bad times overpaying for them. It also value as it's seen as it's shown us goes through long periods of pain. Even if it pays off long term like we discussed earlier, that can make something very hard to arbitrage away. That could be bad news to someone living through it. But good news to whether it's gonna be around for as close to forever as you can say in this business factors most susceptible to being the way are legal information advantages. When I say information advantages, I'm quite careful to please a QR compliance and throw in the word legal. But if you've built a data set and you know, nowadays people call this alternative data and we are actually fairly into it. We, we, we certainly do this if someone builds a new data set and is only gonna sell it to one or two managers. And that itself is a very interesting negotiation. 'cause you have to decide if you think it's real. They charge a lot more than traditional data 'cause they're only giving it to one or two managers. But you don't expect to trade this for 20 years. It's an an informational advantage. It's, you know, you're, you're looking down to a satellite, you're doing a credit card summary of of, of what's going on in the real world and you have an edge for a while. But those kind, any factor that's about speed of in info, getting information and acting faster than other people, you know, and unless you're the fastest in the world, which some people do try to be, that is probably not even close to a permanent edge and everything is on a spectrum.

- Absolutely. Okay, next question. How has machine learning changed, if at all, if at all how, you know, your systematic approach to investing at a QR works?

- Well, it's, it's creeping in is understating it, but it is, it is starting to show up everywhere. And I, I'm nervous saying this 'cause I've said this publicly and the financial press has picked it up and overdone it. I've said that I probably slowed us down by a couple years in machine learning because I was a little cynical. We've always told this story like I was telling you that we care about both data and story. And when you move into machine learning, you, you gotta lean more heavily on data. It's kind of the point, right? You're, you're not telling the story, you're surrendering yourself, if anything, a little more to the data to, so I, I've had a couple of headlines like as this does flip-flop on machine learning, that kind of stuff drives me crazy. Of course, like anyone in business is driven crazy sometimes by the, by the press. We invested a lot in machine learning when it was all on the arm, when we didn't know if it would work. We hired Brian Kelly outta Yale. One of the major machine learning, and I, I'm biased, but I think the top machine learning guy in finance. We, we explored and built machine learning in, in our existing funds. People like Andrea Fini, Laura Serbin here. So we were not so cynical that we didn't pursue it. I just had smaller hopes than maybe some others did because I was so used to this world of, of, of being more worried about overfitting than anything else. And one thing machine learning does is it deals with very complex problems with more parameters. This is quite controversial right now in academia. And I will not try to do Brian Kelly's job because I'll do it horrendously badly. But his paper, the virtue of complexity, arguing that ML changes the equation on on, on how many parameters you can have and the dangers of overfitting versus under fitting. I think Brian's right, but if I try to, I'll, I'll lose the debate if I try to do it, but it is changing how we do things. There are factors where we usually can still get some intuition out of, out of what's going on. I think there are pure ML players that just throw away all intuition and I don't think we've quite gone there, but has ML moved us more towards the data? I got a question once. I never thought of it this way from a client about an ML factor and saying, can you gimme a, a precise, intuitive explanation of what it's doing. I can go, I can give you a very imprecise one, but if I could tell, be very precise about it. What is it doing? Where's the machine learning? What is it doing? If I can just give you a, a, a off the cuff, easy one line answer to it. You know, one of the primary areas where, where ML has helped so far is processing natural language. Being able to tell if something is good or bad. News and quants have done this for a million years. The old fashioned way to do it is to build up keywords and phrases and assign numerical scores. Way oversimplifying. Do you see the word increasing plus one count up all, you know, similar words. And of course you, you immediately see the problem if the actual sentence was massive, embezzlement is increasing, plus one was probably not your best guess. Now quants can survive looking silly 47% of the time if we get it right 53% of the time. So I'm not knocking this old approach, I'm just saying it's very noisy. It turns out that applying a natural language processing to to language data language is a very nonlinear thing. Whether a certain word is good or bad might depend on this sentence. I got the simple one I just gave, but it might depend on three sentences ago. Nothing is perfect. Language is very complicated, but it turns out NLP applied to to, to textural data, to forecast returns. We found to be very powerful and we've had some great success with it. I can tell you in general what it's doing. It's doing a fundamental form of momentum or good things happening. But can I tell you precisely why it likes this stock? I cannot. And when you do ml, you often have to give that up or again, what the heck is the ML doing?

- So next question's. Private markets versus public markets. You're,

- Oh, we're shift, we're shifting gears.

- I know you're, you're a big public markets guy and also a bit outspoken on, on making comparisons between public markets and private markets. Obviously private markets just in terms of assets have totally exploded in in in recent years. You know, do I understand this right? That, you know, when you talk about so-called volatility laundering and, and making the, but you how you can't really compare public market returns to private market returns. Is that the issue? Is that with Marx, how private markets do marks? Is that, that you know, how they value themselves. It's not just a frequency issue and that, you know, public markets, you have every tick that the Australian public markets, but it's, it's a, a quality of marks that, you know, these firms say private equity firms are, are valuing themselves and there's a bit of a bias in terms of how they value themselves and, and that kind of distorts Sure. Volatility and return metrics a bit for, for private funds, say private equity funds, comparing them to say public funds, publicly traded funds.

- I'll give you a short version of my complete private equity story. First the term volatility laundering, which was mine. I, I feel kind of bad about 'cause it's pretty snotty and you know, I'm not really implying anything illegal is going on here. I wanna be clear about that. But laundering is when something doesn't show up that's there. And the way my sense of how most privates are marked is, let's go to two extremes. You can mark any asset at one of two extremes or anywhere in between you could market at where you could sell it at today. And even that has some issues. What if I tried to sell a ton of it today? Maybe you get a lower price but you know what you're trying to do. And for public markets that's quite easy to do. You look up the price and you market there. The other end of the spectrum is you can market at what you think it's worth and that's not illegitimate. You know, that's an interesting thing. My sense of the way where privates do is much closer to where they think it's worth. I think if markets move, they factor that in a little. I don't think they're, they run to a a, a zero beta but they're mostly marking to their model to what they think the thing is is worth. And I don't object to that. If I get to do what I object to is different standards. And then the worst thing is when these are mixed and people will show an efficient frontier using market prices for public assets and what the private people think it's worth prices for the private assets. And you'll see this, you'll see some, some investors put out their, their assumptions and they'll draw 'em on the efficient frontier and they'll have like public equities at 16% vol with an expected 10% return. Private assets at a 5% vol with an expected 14% return. You could debate the 14 versus the 10, but the, the the 16 against five, I think that's what I said. You cannot debate that that's just not apples to orange. That is apples to oranges. And it's, it pisses me off, off because I gotta live in the standard of, of what the market will pay me. I am just as capable of telling you what I think our portfolio is worth. And when we started a QR we started, I mentioned before, right before the.com bubble of the late nineties really took off and we were down a lot before we did very well. Well if I marked to what I think my portfolio is worth, I would've said all these tech stocks that were short, I don't think they're worth this. So I'm gonna mark it to what I think I'm worth. And if I tried to tell my clients actually we're up a little bit, I think they would sue me because they would say no you're not. Look at the prices. And what I don't get is the private people can do exactly the same thing. They are the world's best people at valuing a company. They could tell you where I could sell it today just as easily as they could tell you where their model is. And for some reason they get to do it one way and I get to do it another. And that part of the story I'm certain of that their risk is much higher than you think. If we go through a 10 year bear market, that risk will show up and that's pretty much all you really worry about is the giant bear market. So I do think they're understating their risks. It can even matter for prospective returns going forward. 'cause imagine, and I find this very easy to imagine 'cause I think this is actually what's going on, but imagine a lot of investors have grown to value this volatility laundering. It's easier to stick with if you don't have to deal with the real current market to market prices, right? The public markets are way down in 2022. Privates are only down a little easier to stick with. Well in the early days when David Swenson at Yale was, was pioneering using privates for institutions, it was pretty easy In his book, pioneering portfolio management talks about this all over the place. It was particularly easy to say you get paid a premium for owning the illiquid private asset. 'cause who wants something not marked to market? That's hard to well imagine today. And again I think this is actually at least to some degree what's going on. Imagine today that that is a desired feature, not a bug. That not having to mark to market and not having to report the full volatility is a good thing. Well you pay up for a good thing. You accept a, you, you demand a higher expected return if you have to take on a bad characteristic, you accept a lower expected return if you have to take on, if you're forced to take on or if you take on a characteristic you want. So I think it can actually affect the expected returns going forward. I would not expect, I won't tell you what I think it's gonna be, it's all over the place, but I whatever premium and this is fought over 'cause private data is private data. We don't have the best apples to to, to, to, to apple's comparisons. But whatever the past has been, my strongest guess is privates will not enjoy the same advantage over public going forward. 'cause what used to be a bug is now a feature.

- Hmm. That's,

- And I live in Greenwich, Connecticut and I gotta be careful if I go near a golf course that people won't aim at me.

- That's too funny. Yeah. The the there's a lot, a lot of private equity folks out there now increasing. Yes. Increasing number of them.

- Yes. The old cliche applies to me. Some of my best friends are private equity managers.

- It's that, that's too funny. I I hope they're, they're so kind to you. I wanna sort of, my last question or two here for you is really about your investment philosophy. And I remember when Fama and Schiller both won the Nobel Prize in 2013 along with bars Hansen. It was I think a pretty seminal moment. And I mean in part because they were giving a prize to both Fama who is sort of the standard bearer, the risk-based decision markets view as well as Robert Schiller who is really the standard bearer, the, I would say very behavioral finance view. And I've always felt that you are, you're somewhere sort of in between. You recently wrote a paper titled The Less Efficient Market Hypothesis. I'm curious what you meant by that and

- Sure.

- What your kind of broader view is. Well

- Let me start out by saying Fama should have won a sobel, solo Nobel Prize 10, 15 years earlier than that. I'm still a little bitter.

- Not that Well they could still give him a second prize. I mean you could lobby for that.

- I don't know how often, I don't know if that's ever been done, but I I know in the sciences people have won in other categories. Yeah, but, but it's gonna be hard for it to get a second one in economics. I think. So I think pharma revolutionized the field. We, the efficient market hypothesis, no matter whether you believe it's close to holding or not, is, is kind of the firmament we start with to test everything. So, you know, I think he's the MVP of modern finance. With that said, make it up numbers. I was never a pure behavioralist. Remember I wrote my dissertation a a big part on momentum, which is very hard to reconcile with, with, with risk-based explanations. But I was probably 75 25 f French risk-based and I'm probably 75 25 behavioralist at this point. You know, the real world smacking you in the head, living through multiple things where I would use the word bubble. I'd use the word bubble about early 2000. I'd use the word bubble about late COVID late 2020. I don't use that word very much. I still use it a lot less than a fair amount of active managers twice in a career is not, I think too abusive, but jean don't like that word. So the less efficient market hypothesis was really A-A-A-A-A-A 20 page op-ed, the Journal of Portfolio Management had its 50th, I think 50th anniversary and they invited some of us who've been publishing there a long time to write papers and invited papers are awesome 'cause they're not refereed. So you have a, you, you have a lot more latitude. Frank Zi the wonderful publisher there. I think he, he would do some quality control if I submitted something insane, but it's not quite the same. He encouraged us to muse a little bit more. It was supposed to be like an old man reflecting on what they've learned. And I do think over my career I have moved on this and I think markets have actually changed somewhat that, that that value spread thing we described earlier, the, the spread between cheap and expensive by March of 2000, the.com bubble hit levels that were not close to anything in 50 years of history when the next two to three years happened and we made way more than all that money back. And life was good. If you had said to me, are you gonna see something as crazy in your career again, I don't think, I hope I never would've promised anything, not just for legal reasons, but for intellectual reasons. Never say never. But I, I think I would've said very, very unlikely for one, it was the biggest in 50 years. I, you know, as much as I'd like to live forever, I don't think I necessarily have a 50 year career. Two, your question presupposes I and others like me will still be around in your career. And we saw this and then by the end of COVID it was getting close before COVID. So I can't blame COVID for the whole thing. By the end of COVID by late 2020, it was substantially wider of value spread as we measure it than we saw in the.com bubble. So if that doesn't make you go, has something changed versus history over the last 20, 30 years? And I have a few hypotheses. I know you are very, the inelastic market hypothesis, how that affects indexing and whatnot. The, the growth of indexing could matter. I I am not someone who thinks the growth of indexing is the worst thing that's ever happened in the world. There are a fair amount of people who are, I think a little hysterical about it, but we all know that the, the, the classic kind of finance, you know, brain teaser, what if everybody tried to cap weight index is gibberish, right? There's literally nobody thinking about prices. It's hard to believe we jumped to gibberish going from 99.999% indexing to a hundred. So the fact that we have a lot more people cap weight indexing and a lot and a lot fewer people looking at companies, could that matter for this? Could that let prices drift further? I don't have a formal model but yeah, I accept that. My favorite hypothesis and I I stress the word hypothesis 'cause nobody knows is I'm gonna really sound like a, an old man yelling at clouds now. But it, the, the the social media environment 24 7 gamified trading. I think most people of any political persuasion, I won't say everyone 'cause we have a lot of people with some odd views these days, but I think most people would probably agree that this environment has made our politics worse. It's pushed us into bubbles. It's confirmation bias has gone way up. It, it has made herd mob behavior easier to get going. Markets are voting mechanisms. They're not arbitrage mechanisms, they're voting mechanisms. The old schleifer ny limits of arbitrage said no, it could be an arbitrage, but if you can't hold it, it doesn't last. If, if if somebody has is making an error. Fama French wrote a paper on this too. If somebody is making an error, you take the other side of that error but not enough tobit to zero. 'cause the early part of taking the other side makes you a decent expected return and low risk. But as you keep adding that to your portfolio, you're closing the gap and the expected return goes down and the risk goes up. 'cause you have to own more of it. So if, if, if the world makes net errors as fa and French say, and I'm paraphrasing, less errors miraculously balance each other, prices will be set in a vote in a dollar weighted vote. So I find it very hard to believe that this environment has made our politics much worse. But a voting mechanism called the market has been immune to it. I could be cheap and point to the meme stocks. I think they are a extreme mutated example of what I'm talking about. But I think it has, it has made the idea of, of mispricings, even if they're not all the time occasional large mispricings from mob behavior, much more plausible to me. Sorry, go

- On. There's, there's this question about quantities, right? So, so i I think it's it's very much integrated in into this where, you know, right now there's in academic finance a big debate happening and, and you mentioned this about, you know, the role quantities and and what do we mean by that? You know, it's, if if you hypothetically had, you know, a a billion dollars on the sidelines in cash that just went into the stock market, what would the effect of that, you know, influx of cash say $1 billion, would it be, you know, a permanent increase of $5 billion or multiplier five? And that's kind of what the very behavioral folks like Xavier Gbe and Ralph Koan argue in their new paper Inelastic Markets hypothesis. It's called the Inelastic Markets hypothesis. Some people would argue it's a bit less, you know, there was a paper in the 1980s by Andre Schleifer that you know, you know, does the demand curve for stocks slow down? I sort of, I have a tongue in cheek paper called the elastic markets hypothesis that argues it is somewhere in between, probably similar to yourself. But there is this question about, you know, what is the shape of the demand curve for assets and you know, in efficient markets world, I think I would say it's sort of perfectly elastic. Very, very horizontal. And in that sort of Fama world or modern finance world, information was key. Arbitrage were key. Yeah. But it seems like

- Prices expected discounted cash flows, which doesn't move with a trade.

- Exactly. And it seems like this kind of, you know, say very behavioral vision of very inelastic markets is is almost going sort of pre-modern finance where everything was about supply and demand. And I'm just curious what you think about, you know, how qu how quantities work. I mean a QR I'm sure spends a lot of time thinking about market impact of trading transaction costs. You know, there there's this famous, you know, three half model or you know, quad model of market impact out there. I mean how do you think about sure quantities market impact, is it a short term thing and things revert or is it a permanent thing in the same respect that gibe and coin and argue there's this five x multiplier that's kind of a permanent thing. Sure. How do you think about that?

- Okay, it's your fault. Again, this is a nine part question. A first full disclosure. I think the world of Ralph Cogen, we gave him an award for the inelastic market hypothesis paper. 'cause we used to give out an annual award and he is actually the A QR professor of finance at the University of Chicago. So with that said, I am, as you predicted closer to you on this. I i I don't, I my guess, and it really is a guess, you're closer to the academic debate than I am. My guess is it comes out that markets are certainly not perfectly elastic gene, gene Fama when it comes to the efficient market hypothesis. Something like second week of class. He tells you markets are certainly not perfectly efficient and the class guess 'cause they're Gene Fama's class and the University of Chicago and he looks at him like, he doesn't say this 'cause a very nice man, but he is like, what are you idiots? Perfection is a stupid hypothesis. The real world isn't perfect. So I'm gonna guess some of it holds up. I'm gonna get some of the critiques that are coming out, bring those results a little back towards the middle. But one thing I stress is I make very little of my living based on market direction. I'm, I make it much more based on stock and other asset selection. We do macro also, but thinking about just stocks much more of my life is about a thousand to 1500 stocks long against a thousand to 1500 stocks short. And the, the, the idea that that is highly inelastic is far less plausible in the market. We can debate the market, but the market has few close substitutes and you can't have, if you, if if you have few substitutes, it's at least plausible to be somewhat inelastic. But if you have a lot of close substitutes, I think it gets very implausible. And individual stocks have tons of close substitutes. So I have not seen you, you might be more, you probably are more familiar with the literature, any paper claiming that that individual stocks in a say a market neutral trade are highly inelastic. It. Have you?

- Well, I I I don't, I think the claim that Quebec,

- It's a hadda paper that has something along this line.

- There, there are some that have tried to push the inelastic markets hypothesis thing beyond just sort of macro assets, which is I think the original sort of Ralph coin argument that, that it may exist also in, in at the stock level. But I'm, I'm skeptical of claims about either.

- Yeah, but, and when it comes to market impact, first of all it's very real. You know, if you assume zero market impact, you way overestimate what you'll make from any model or active process. But comes to reversion at the individual stock level, one stock against another. I think most of market impact is not permanent Because again, being close substitutes, I don't think it, it, it, it moves prices to the same extent. And it would be kind of weird if the prospects of one stock against another were permanently altered because somebody put a trade on one day. You can imagine the market has to absorb that a lot of people, which is not us, make their living from so-called statistical arbitrage even going into the high frequency trading world. And a lot of that is about what tends to trend and what tends to reverse at the short term. And again, this is not my world. I wrote a paper that was very close to state of the art stat arb in 1995, and I've been told this by stat arb people and it's my fifth story, you know, every fisherman has the one that got away the big one. And I looked at it and said, doesn't cover TCOs. And moved on. And, and it did ultimately, if you kept that, it covered TCOs, I should have kept with that one big error. But I think most of the market impact we look at is relatively short term. And, and the jury I think is still out on market wide market impact. Even there, I find it hard to believe you get a forever change in price. But is it last, can it last longer? Is it hard to take the other, harder to take the other side there, the plausibility of the, of, of the kogen etal story, she only has one co-author, so I shouldn't say etal, but I can never pronounce the name right. So

- Get back is alright friend's last name,

- Yes. We, we don't mean this meanly or a wonderful researcher, the plausibility of that story, but when he says how many people will take a market bet, we tend to run most things to a zero beta. So if somebody wants to go long extra stocks, we tend to mostly, I won't say completely, mostly not be the people who take the other side of that. So then, you know, a lot of funds are wired to do that now. So the notion that that some of that maybe again, full permanency, I just instinctively find hard to believe. But the idea that is far closer to, to permanent, that lasts much longer. I, I I find that plausible, the, the market wide argument, which I think is where most of this is occurring, is mostly spectator sport. For me, it, I don't think it affects very much what we do, but I will be watching to see which one of you guys ends up winning.

- Well, yeah, well I feel like there's, there's some similarities with the, the, the less efficient markets hypothesis in the elastic markets hypothesis and things are almost efficient but not perfectly efficient. And there, you know, there's some things that are behavioral out there, but, but, but not a ton. So, so maybe we'll we will, we'll take that tag team for the win. Cliff, I really wanna thank you for coming on. This has been an amazing conversation.

- Oh, I really enjoyed it, John. These were fantastic questions and thank you for having me.

- This is the Capitalism and Freedom, the 21st Century podcast, an official podcast of the Hoover Institution Economic Policy Working group where we talk about economics, markets, and public policy. I'm John Huntley, your host. Thanks so much for joining us.

ABOUT THE SPEAKERS:

Cliff Asness is a Founder, Managing Principal, and Chief Investment Officer at AQR Capital Management. He is an active researcher and has authored articles on a variety of financial topics for many publications, including The Journal of Portfolio Management, Financial Analysts Journal, The Journal of Finance, and The Journal of Financial Economics. He has received five Bernstein Fabozzi/Jacobs Levy Awards from The Journal of Portfolio Management in 2002, 2004, 2005, 2014, and 2015. Financial Analysts Journal has twice awarded him the Graham and Dodd Award for the year’s best paper, as well as a Graham and Dodd Excellence Award, the award for the best perspectives piece, and the Graham and Dodd Readers’ Choice Award. He has won the second prize of the Fama/DFA Prize for Capital Markets and Asset Pricing in the 2020 Journal of Financial Economics. In 2006, the CFA Institute presented Cliff with the James R. Vertin Award, which is periodically given to individuals who have produced a body of research notable for its relevance and enduring value to investment professionals.

Prior to co-founding AQR Capital Management, he was a Managing Director and Director of Quantitative Research for the Asset Management Division of Goldman, Sachs & Co. He is on the advisory board of the Journal of Investment Management and on the ambassador board of The Journal of Portfolio Management, where he is a frequent author. He is also a board member of the American Enterprise Institute and Commentary Magazine.

Cliff received a B.S. in economics from the Wharton School and a B.S. in engineering from the Moore School of Electrical Engineering at the University of Pennsylvania, graduating summa cum laude in both. He received an M.B.A. with high honors and a Ph.D. in finance from the University of Chicago, where he was Eugene Fama’s student and teaching assistant for two years (so he still feels guilty when trying to beat the market).

Jon Hartley is currently a Policy Fellow at the Hoover Institution, an economics PhD Candidate at Stanford University, a Research Fellow at the UT-Austin Civitas Institute, a Senior Fellow at the Foundation for Research on Equal Opportunity (FREOPP), a Senior Fellow at the Macdonald-Laurier Institute, and an Affiliated Scholar at the Mercatus Center. Jon also is the host of the Capitalism and Freedom in the 21st Century Podcast, an official podcast of the Hoover Institution, a member of the Canadian Group of Economists, and the chair of the Economic Club of Miami.

Jon has previously worked at Goldman Sachs Asset Management as a Fixed Income Portfolio Construction and Risk Management Associate and as a Quantitative Investment Strategies Client Portfolio Management Senior Analyst and in various policy/governmental roles at the World Bank, IMF, Committee on Capital Markets Regulation, U.S. Congress Joint Economic Committee, the Federal Reserve Bank of New York, the Federal Reserve Bank of Chicago, and the Bank of Canada.

Jon has also been a regular economics contributor for National Review Online, Forbes and The Huffington Post and has contributed to The Wall Street Journal, The New York Times, USA Today, Globe and Mail, National Post, and Toronto Star among other outlets. Jon has also appeared on CNBC, Fox Business, Fox News, Bloomberg, and NBC and was named to the 2017 Forbes 30 Under 30 Law & Policy list, the 2017 Wharton 40 Under 40 list and was previously a World Economic Forum Global Shaper.

ABOUT THE SERIES: