- Economics

- Law & Policy

- Civil Rights & Race

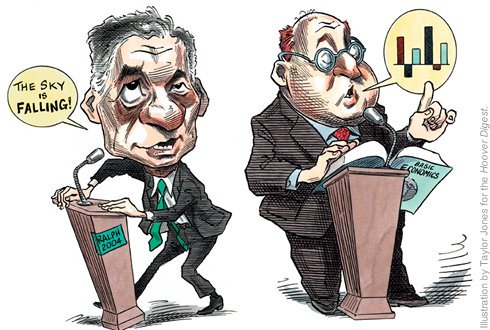

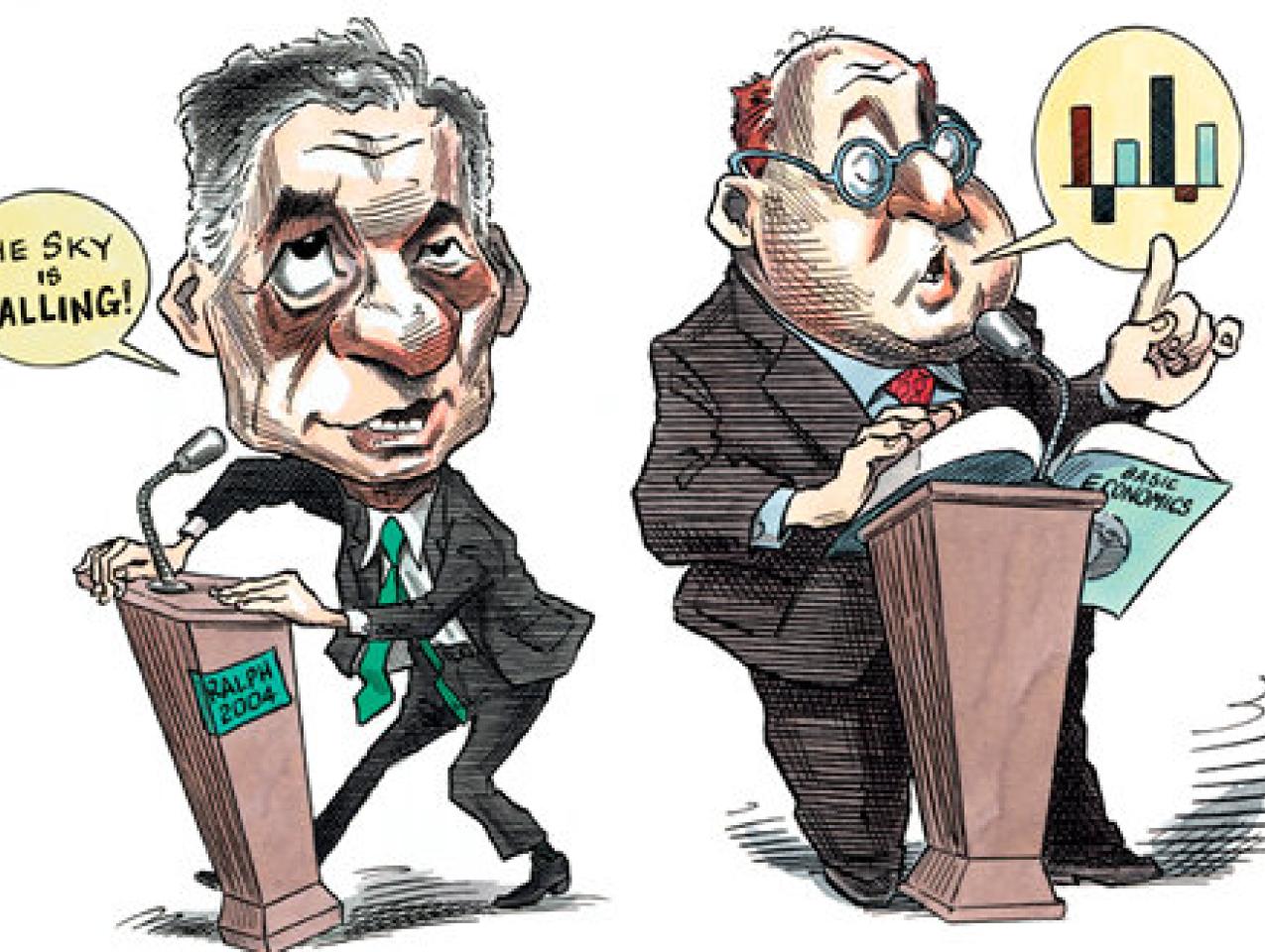

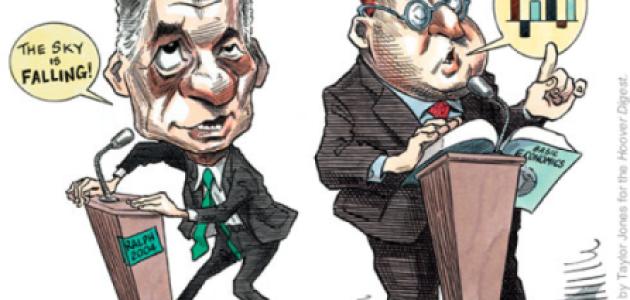

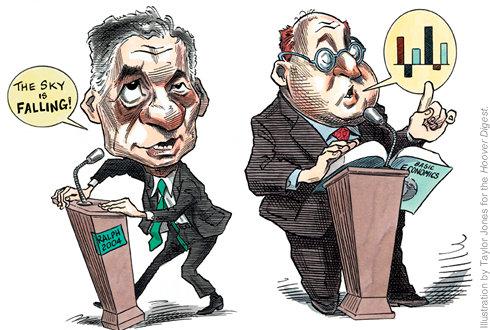

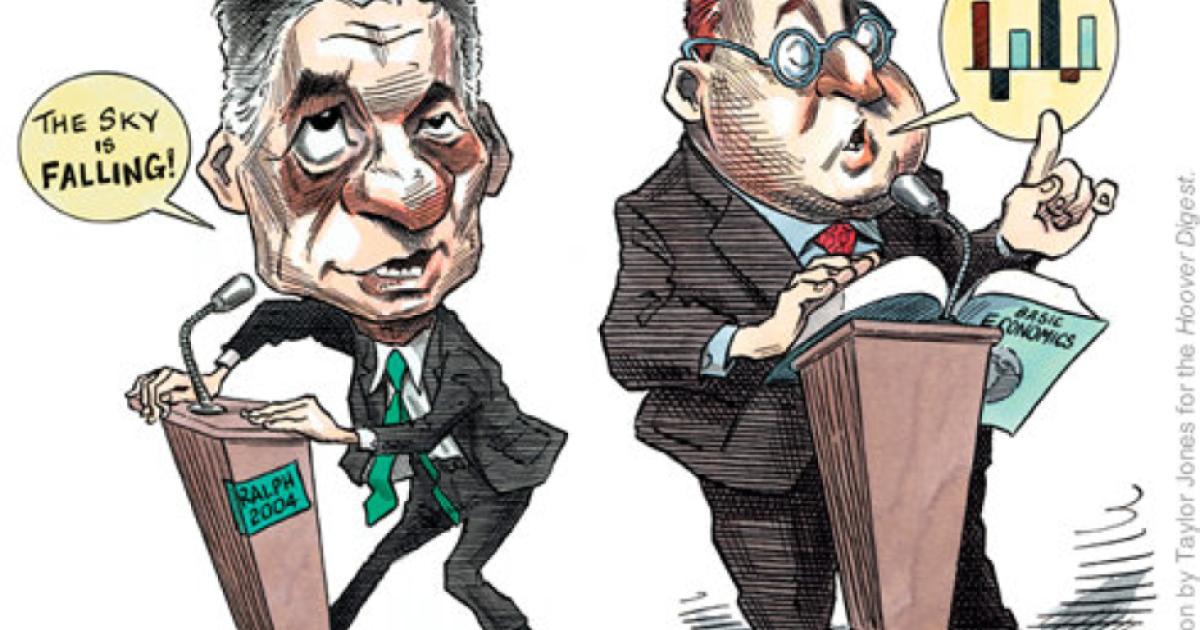

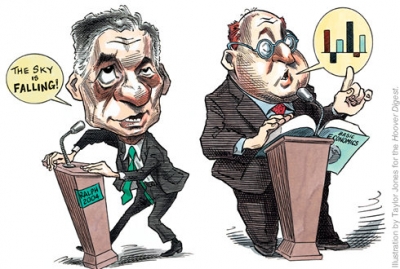

Some years ago, the distinguished international-trade economist Jagdish Bhagwati was visiting Cornell University, giving a lecture to graduate students during the day and debating Ralph Nader on free trade that evening. During his lecture, Professor Bhagwati asked how many of the graduate students would be attending that evening’s debate. Not one hand went up.

Amazed, he asked why. The answer was that the economics students considered it to be a waste of time. The kind of silly stuff that Ralph Nader was saying had been refuted by economists ages ago. The net result was that the audience for the debate consisted of people largely illiterate in economics, and they cheered for Nader.

Professor Bhagwati was exceptional among leading economists in understanding the need to confront gross misconceptions of economics in the general public, including the so-called educated public. Nobel laureates Milton Friedman and Gary Becker are other such exceptions in addressing a wider general audience, rather than confining what they say to technical analysis addressed to fellow economists and their students. By and large, the economics profession fails to educate the public on the basics, while devoting much time and effort to narrower and even esoteric research.

The net result is that fallacies flourish in discussions of economic policy issues, while the refutations of those fallacies lie dormant in old books and academic journals gathering dust on library shelves. As former House majority leader Dick Armey—an economist by trade—put it: “Demagoguery beats data in making public policy.”

Sometimes the fallacies are based on something as simple as a failure to define terms accurately. Everyone has heard the claim that a high-wage country like the United States loses jobs to low-wage countries when there is free trade. When the North American Free Trade Agreement went into effect a decade ago, there were dire predictions of “a giant sucking sound” as American jobs were drawn away, to Mexico especially.

In reality, the number of jobs in the United States increased by millions after NAFTA went into effect and the unemployment rate fell to low levels not seen in years. Behind the radically wrong predictions was a simple confusion between wage rates and labor costs. Wage rates per unit of time are not the same as labor costs per unit of output. When workers are paid twice as much per hour and produce three times as much per hour, the labor costs per unit of output are lower. That is why high-wage countries have been exporting to low-wage countries for centuries. An international study found the average productivity of workers in the modern sector of the Indian economy to be 15 percent of that of American workers.

In other words, if you paid the average Indian worker one-fifth of what you paid the average American worker, it would cost you more to get the job done in India.

In particular industries, such as computer software, Indian workers are more comparable, which is why there is so much outsourcing of computer work to India. But virtually every country has a comparative advantage in something, whether it is a high-wage country or a low-wage country.

Those who complain loudly about how many jobs have been “exported” to other countries because of international free trade totally ignore all the jobs that have been imported to the American economy because of that same free trade. Siemens alone employs tens of thousands of American workers, and Toyota has already produced its ten millionth car in the United States. Management guru Peter Drucker has said that this country imports far more jobs than it exports, and no one has contradicted him. Indeed, those who are loudest in denouncing the exporting of jobs totally ignore the importing of jobs.

Free international trade produces both the benefits of increased productivity and the adjustment problems that all other forms of increased productivity produce—namely, job losses in the less competitive firms and industries. The typewriter industry was devastated by the rise of the computer, as the horse and buggy industry was devastated by the rise of the automobile. Histories of the industrial revolution lament the plight of the hand-loom weavers when power looms were introduced.

International trade has no monopoly on economic illiteracy. One of the apparently invincible fallacies of our times is the belief that President Ronald Reagan’s tax cuts caused the federal budget deficits of the 1980s. In reality, the federal government collected more tax revenue in every year of the Reagan administration than had ever been collected in any year of any previous administration. But there is no amount of money that Congress cannot outspend. Here again, the confusion is due to a simple failure to define terms.

What Reagan’s “tax cuts for the rich” actually cut were the tax rates per dollar of income. Out of rising incomes, the country as a whole—including the rich—paid more total taxes than ever before.

At the state and local levels, this confusion of tax rates and tax revenues has led some local politicians to see higher tax rates as the answer to budget problems, even though higher tax rates can drive businesses out of the city or state, with adverse effects on the total amount of tax revenues collected.

Price controls are another area where very elementary economics is all that is needed to show what the consequences are: shortages, quality deterioration, and black markets. It has happened repeatedly in countries around the world, over a period of centuries. Yet politicians keep selling the idea of price controls and voters keeping buying it.

Many economic issues are complex, but sometimes a single fact will tell you all you need to know. When you know that central planners in the Soviet Union had to set 24 million prices—and keep adjusting them, relative to one another, as conditions changed—you realize that central planning did not just happen to fail. It had no chance of succeeding from the outset. It is a wholly different ball game when hundreds of millions of people individually keep track of the relatively few prices they need to know for their own decision making in a market economy.

Simple stuff like this is not very exciting for economists, and there is no payoff in one’s professional career for clarifying such things for the general public. The only reason to do it is that it very much needs to be done—especially during an election year.