- Politics, Institutions, and Public Opinion

Editor’s note: This is a summary of the paper, “Political Actions by Private Interests: Mortgage Market Regulation in the Wake of Dodd-Frank,” presented at the Hoover Institution Executive Power and the Rule of Law Conferences in March and June 2016. Sanford Gordon and Howard Rosenthal are Professors in the Department of Politics at New York University.

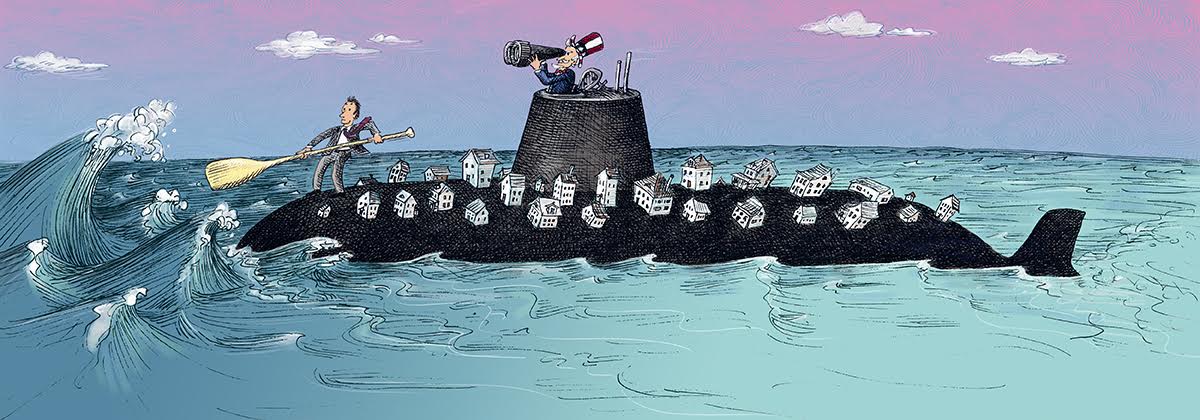

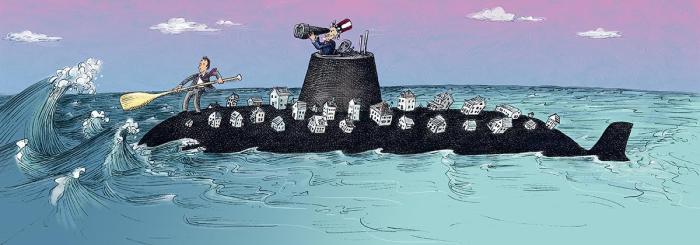

Outstanding residential mortgage debt in the United States tops $11 trillion. The sheer size of this market makes the regulation of systemic risk stemming from these loans a critical object of economic policy. Subprime lending—seen by many as the central contributing factor to the financial crisis of 2007-2009—may be largely a thing of the past, but the regulatory regime that emerged in the wake of the financial crisis has created what might be described as “subprime lite.” Specifically, while the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 contained several provisions intended to reduce the amount of risk in the system, the political conflict over regulatory rulemaking pursuant to those provisions has, to a great extent, led to relatively weak standards.

Our purpose in this article is not to evaluate the appropriateness of those standards. Rather, we provide a perspective on the politics that led to diminished standards. Unsurprisingly, during the course of the rulemaking process, the residential real estate industry—a category that includes realtors, mortgage lenders, builders, title insurers, and mortgage insurers—favored standards weaker than those initially proposed by regulators. The account that follows describes the mechanism by which this preference ultimately translated into regulatory policy. Unlike previous accounts, our narrative deemphasizes the role of lobbying and campaign expenditures. Instead, we focus on the success of the industry in reforging its alliance with progressive groups that favored broadening access to mortgage markets in the run-up to the crisis. Our account highlights the role of organization, in the form of the “Coalition for Sensible Housing Policy” that came to dominate discussions of the rulemaking; the success of the Coalition in mobilizing a bipartisan array of legislators on its behalf; and the ability of the Coalition to outlast regulators who favored a more aggressive approach to tamping down excess risk-taking in the mortgage market.

The Dodd-Frank Act

Before the financial crisis, two aspects of the residential mortgage market were largely unregulated. First, the contract between lender and borrower could take nearly any form, and have little or no relation to the financial capacity of the borrower. In this environment, a host of esoteric mortgage instruments emerged: negative amortization loans, interest only loans, teaser loans with low initial rates, loans with balloon payments, loans with no income verification, and loans that required borrowers to make payments constituting a large fraction of their monthly income. Second, these contracts could be sold and packaged into private mortgage backed securities in which neither the borrowers nor the securitizers had to have “skin in the game”—that is, a retained equity interest in the underlying assets. Borrowers could have loan-to-value ratios in excess of one; and securitizers could retain no financial interest in the underlying mortgages.

The financial crisis precipitated calls for more regulation. There was widespread support for more regulation from those in regulatory agencies, the financial community, the political class, and a mass public that attributed the meltdown to inadequate regulation. Criticism of the deregulated market focused on two issues. First, too many “subprime” borrowers were led into products they could not handle from the outset or would default on given a severe decline in housing prices or at the expiration of teaser rates. Second, the absence of skin in the game meant that too many securities were based on mortgages where the securitizer had little to no incentive to control their underlying quality.

The political response was the Dodd-Frank act of 2010. There was a sharp partisan split on Dodd-Frank. In the House, only 3 Republicans voted for the bill. In the Senate, only three Republicans voted in favor and no Democrats voted against. The partisan split over the bill stands in contrast to the bipartisan consensus that would emerge concerning the loosening of regulatory rules governing mortgage market regulation in subsequent years. Dodd-Frank is byzantine, containing hundreds of new regulatory mandates. Of particular importance in the current story are two provisions: First, the legislation delegated the crafting of the “Qualified Mortgage” (QM) rule to the newly created Consumer Financial Protection Bureau. Lenders making QMs are given safe harbor from liability under the Truth-in-Lending Act. The statute’s definition of a QM includes provisions pertaining to balloon payments, negative amortization, prepayment penalties, negative interest payments, fully amortizing repayment schedules, points and fees, and term of loan; however, the law also delegated to the board regulatory authority the power to revise, add to, or subtract from these criteria. The QM category is intended to encompass, per the statutory language, loans satisfying a minimum underwriting standard.

Second, Dodd-Frank tasked six agencies—the FHFA, Federal Reserve, FDIC, OCC, SEC, and HUD—with responsibility for creating a “Qualified Residential Mortgage” (QRM) rule. Dodd-Frank requires that securitizers retain a five percent interest in asset-backed securities, but exempts QRMs from this requirement. The statute instructs the agencies to take into account underwriting and product features, including document verification, and debt-to-income, and prohibiting and restricting the use of product features such as those in the statutory definition of QM (balloon payments, etc.) Importantly, the law requires that the QRM definition be “no broader than” the QM definition.

Regulatory Implementation

The ultimate expression of “subprime lite” is contained in the form that the QM and QRM rules ultimately took. When regulators incorporated the specific statutory criteria of the QM and QRM definitions into draft rules, they were met with little opposition. Instead, the political battle took place over that which Congress left unmentioned or unspecified.

Ultimately, CFPB crafted a relatively weak standard for QM. CFPB issued its final QM rule in January 2013. In establishing the consumer’s ability to repay, the QM rule permits monthly debt payments as high as 43% of the borrower’s income. Moreover, any mortgage purchased by the FHA, Fannie Mae, or Freddie Mac is “temporarily” qualified. Seven months later, the six agencies charged with fashioning the QRM definition proposed a rule that simply aligned QRM and QM. In other words, the agencies made the standard as lenient as the statute’s “no broader than” injunction permitted.

This rule, which was formally adopted in late 2014, was a far cry from the rule the agencies had initially proposed in the immediate aftermath of Dodd Frank’s passage. In March 2011, the six agencies proposed a very different QRM standard: in addition to the statutory provisions, the proposed rule would have imposed a maximum debt-to-income ratio of 36% (with housing debt constituting 28% or less of income) and a down payment of 20% or higher for new home purchases. Refinances would have even stricter standards, with loan-to-value ratios at most 75 percent for straight refinances, 70 percent for cash outs. The proposal ignited a firestorm of protest from industry, advocacy organizations, and members of Congress, to which regulators ultimately acquiesced.

It was no secret in the winter of 2011 that regulators were contemplating a stringent QRM rule: several weeks before the notice of proposed rulemaking, Senators Hagan (D-NC), Isaakson (R-GA), and Landrieu (D-LA) wrote the heads of the six agencies to request the down payment provision—ultimately the most controversial feature of the initial rule—be pulled. The regulators did not heed their letter. So what caused the regulators to shift from the initial standard to subprime lite?

We consider several explanations: (1) presidential pressure; (2) changes in lobbying outlays and campaign contribution expenditures over the course of the rule-making process; (3) the development of a coalition of industry interests and advocacy organizations promoting housing for the poor and minorities and, relatedly, bipartisan support within Congress for coalition’s position; and (4) changes in rulemaking agency leadership between the initial and revised rules.

Presidential Influence

The White House does not appear to have been an important direct channel in the diminution of regulated mortgage standards. Press coverage does not indicate an advocacy position by President Obama. During the period between the 2011 proposed standard and the 2013 revised QRM standard, Obama’s influence was expressed chiefly through the appointment of regulators: most notably in the replacement of Sheila Bair at the FDIC and by the nomination of Melvin Watt to head the FHFA.

Industry Lobbying Expenditures and Campaign Contributions.

Government records of campaign contributions and lobbying expenditures do not allow us to pinpoint expenditures specifically allocated to affect the QM and QRM rules. We cannot know, for example, whether a bank’s political action committee contributed to a candidate because of her stance on mortgage regulation as opposed to her stance on derivatives trading. Likewise, a lobbying disclosure report discloses, in addition to a client’s total lobbying expenditures in a quarter, the issues and legislation on which lobbying occurred, and the agencies (including Congress) lobbied; however, it does not disaggregate those expenditures across issues, legislation, or agencies. Likewise, the report does not specify the actual position advocated for by the lobbyist on behalf of the client. Because of these limitations, we can only ask whether the period of regulatory decision-making experienced a discontinuous jump in industry contributions and lobbying expenditures.

To study dynamics of political expenditures, we compiled quarterly data on lobbying and PAC contribution activity of the 149 mortgage lenders who were in the largest 100 in at least one quarter in 2008-2013. Lobbying expenditures by lenders declined in 2008 and 2009, in the darkest days of the financial crisis, and then gradually returned to pre-crisis levels. Importantly, however, we observe no uptick either immediately prior to Dodd-Frank or in the quarters for which the rules defining specific classes of mortgages were most hotly debated. Total PAC contributions tell a similar story, although the point is obscured by the cyclical nature of those contributions (which tend to spike in the second and third quarters of presidential and congressional election years). In short, the data do not suggest either that there were last-minute contributions to affect the content of the legislation or that an incipient regulatory regime induced substantial increases in political expenditures. The same pattern holds when we look at political expenditures by members of the coalition that pushed to relax the QRM standard (described in greater detail below).

One change that did occur is that PAC contributions shifted toward Republican candidates in anticipation of and after the change in control of Congress brought about by the 2010 midterm elections. This back-and-forth with partisan control of Congress is an old story, however, and would appear to bear little relation to QM and QRM given that Congress ultimately showed strong bipartisan support for subprime lite.

Coalition Organization.

A critical political development brought about by the publication of the proposed QRM standard in 2011 was the formation of the Coalition for Sensible Housing Policy (CSHP), and the submission, during the proposed rule’s notice and comment period, of the Coalition’s white paper, “Proposed Qualified Residential Mortgage Definition Harms Creditworthy Borrowers While Frustrating Housing Recovery.” CSHP observed that Congress had rejected including a down payment requirement as part of the QRM definition during debates over relevant Dodd-Frank. The white paper argued that the down payment would harm consumers, stunt the recovery of the housing market, and fail to shrink government presence in the housing market. Ultimately the CSHP would propose aligning the QM and QRM standards.

What was perhaps more important than what was said in the white paper was who was saying it. The National Association of Realtors took credit for organizing the coalition through the public relations firm of Rasky-Baerlin. The coalition grew to encompass 57 trade associations and advocacy organizations. Unsurprisingly, trade associations representing financial, insurance, and real estate interests were on board, including the American Bankers Association, the Community Lenders Association, and the Mortgage Bankers Association. The Mortgage Insurance Companies of America (MICA) also joined: borrowers with mortgages with a loan-to-value ratio above 80% must buy mortgage insurance for Fannie and Freddie to purchase them, creating a significant interest for the insurers in a high volume of loans with small down payments.

Along with industry trade associations, however, CSHP also contained a number of community advocacy, left-wing, and civil rights organizations as signatories. These included the NAACP, the National Urban League, Habitat for Humanity, Consumer Federation of America, and the National Fair Housing Alliance. By 2013, when CSHP was commenting on the revised rule, the Center for American Progress (CAP) joined in as well. These additional signatories signal the rebirth of the pre-crisis coalition that had supported weak standards that arguably brought about the subprime crisis in the first place. In its earlier incarnation, that coalition was supported by the lobbying and organizational efforts of the GSEs: between the two of them, Fannie Mae and Freddie Mac racked up more than $100 million in lobbying expenses from 2003-2007; and starting in the 1990s, Fannie opened partnership offices in local communities to foster the alliance with low income housing advocacy groups and facilitate grassroots lobbying. Conservatorship has eliminated lobbying by the GSEs, but the CSHP has effectively replaced their organizational role.

The position advocated by the CSHP found widespread support in the hundreds of comments submitted to the regulators in the Notice and Comment period between the 2011 proposed credit risk retention rule and the revised rule in 2013. Although some of the comments concerned other aspects of credit risk retention, such as automobile loans and premium cash reserves, the vast majority were focused on the down payment and LTV standards for residential mortgages. Of these (excluding less than a handful from private individuals), all took the same position as the CHSP, with two exceptions. JP Morgan Chase and Wells Fargo, two large banks that were also the largest mortgage lenders at the time, supported relatively strict standards. Otherwise, industry players that commented, including the large lender Quicken Loans, all supported subprime lite. Many of the trade associations in CSHP submitted their own comments, as did 10 of the 11 Home Loan Boards in a joint comment. Similarly, minority organizations commented, and were echoed by non-coalition member La Raza.

Perhaps the most influential comments were those submitted by members of Congress. 304 representatives and 48 senators were on record supporting eliminating or weakening the down payment and LTV provisions of the preliminary QRM rule. These signatories were evenly spread across the two major parties and across the liberal-conservative ideological continuum. And not a single member of Congress expressed support for these features of the initial rule.

Rotation of Regulators.

Regulators undoubtedly found it difficult, if not impossible, to resist the pressure from the industry, its organizational allies, and Congress. Regulatory acquiescence was facilitated by the ultimate departure of officials who favored a more aggressive regulatory approach. Most notably FDIC chair Sheila Bair (appointed by George W. Bush) was replaced by Martin Gruenberg. Out of government, Bair expressed disappointment at the revised rule.

***

We have characterized the revised rule as subprime lite. Whether the rule makes sense as public policy is debatable. On the one hand, loans can be made without the borrower’s having sufficient equity to provide an incentive against default. Borrowers may also find themselves with insufficient income to cover the monthly payment. On the other hand, the retained statutory provisions concerning negative amortization loans, interest only loans, balloon payment loans, etc. may prevent the worst excesses of the subprime period.

That being said even lower lending standards may be quite possible in the future. It is likely that different motives were expressed in the bipartisan support in Congress for the position of the CSHP. Republicans like lax standards because they move in the direction of deregulation. Democrats like lax standards because they make credit more available to their base.

The Republican motive found expression in late 2015 when the House passed “The Portfolio Lending and Mortgage Access Act,” which would have expanded QM to include any loan on a lender’s balance sheet, irrespective of product features. The bill passed on an almost perfect party-line vote. (The Senate took no action, and President Obama would likely have vetoed the bill had it been presented to him.) Any future Democratic congressional majority might be favorable to adjusting QM or QRM in a manner that would make credit more widely available. Moreover, even in the absence of new legislation, the CFPB can revise the “statutory” provisions under Section 1412 of Dodd-Frank. After several more years without a popped real estate bubble and a favorable political constellation, it is not inconceivable that a coalition will form for further relaxation of what is “qualified.”