New empirical research establishes a strong relationship between very low interest rates set by the Fed, as in the period 2002-2005, and a risk-taking search for yield. This policy-induced lessening of risk aversion has been emphasized by Raghu Rajan and others as a key factor bringing on the financial crisis. The new empirical support for this view is reported in the working paper “Risk, Uncertainty and Monetary Policy” by Geert Bekaert, Marie Hoerova, and Marco Lo Duca.

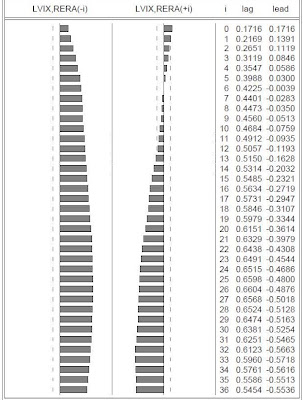

The basic evidence is the pattern of correlations over time which can found by looking carefully through the following bar graphs and table drawn from the paper.

The bar graphs show the correlation between market volatility, measured by VIX, and the interest rate set by the Fed, measured by RERA—the federal fund rate minus the inflation rate. The two columns of five-digit numbers in the table labeled lead and lag are the values of the correlations shown in the bars. (VIX, of course, is the implied volatility of the S&P 500. The identifier LVIX is used because they actually look at the log of VIX).