- Law & Policy

- Regulation & Property Rights

- Economics

By far the most common response to providing environmental quality or to conserving natural resources has been command-and-control regulations where the government decides what actions shall be taken by individuals and organizations to meet an environmental objective and enforces them with its police powers. As one would expect, there are numerous problems with this approach; let’s focus on air pollution control and fisheries to illustrate them.

One problem is that regulators do not have the information required to set a cap on the right amount of air pollution or total fishing. They typically rely upon the assessments of agency experts that may or may not coincide with what actual users believe. Indeed, the relationship between users and regulators is often understandably antagonistic with little trust or cooperation. And in other cases, influential parties use regulatory rules to advance their position relative to their competitors. In either case, the “wrong” regulation is likely to be put into place—at least for meeting the objective of improving the environment or protecting a resource in a cost-effective manner.

Illustration by Barbara Kelley

Another related problem is that because regulators do not have the correct information, they typically mandate uniform technologies or performance standards for all parties. Those regulations do not account for the differences across firms in their abatement costs. In the case of electricity utilities, for example, the Environmental Protection Agency (EPA) under the Clean Air Act required that all utilities install flue gas scrubbers to remove sulfur dioxide even if some emitted little sulfur dioxide because they used natural gas or low-sulfur coal in their power plants.

Ideally, regulations should be flexible, allowing those organizations that can reduce pollution at lower cost to do so and be compensated, while allowing those that have higher compliance costs to cut back less, but pay a price. In this manner, a total pollution objective could be met at the lowest cost because most of the reductions would be accomplished by the organizations that can do so most efficiently. Further, these policies would gradually equalize marginal abatement costs across firms. What kind of program would meet these goals?

In both air pollution control and fishery regulation there has been an ingenious “property rights” solution. Because air and migratory ocean fisheries cannot be easily bounded into individual property rights, the alternative has been to designate private “use rights” to the resource, while not to the resource itself. What this means is that fishermen have a right to fish, but do not own the fishery. Similarly, firms have the right to pollute, but do not own the atmosphere. While traveling fish stocks and the air cannot easily be carved up into property rights, their use can.

The way this works is that in the case of air pollution, the total annual amount of allowable emissions is set—usually by a regulator. But instead of commanding that all firms meet this goal, firms are issued tradable shares in the allowable emissions. For each ton of air pollution released, the firm must give up emission shares. The total number of allowable emission shares can be reduced each year until the desired cap or pollution objective is met. Firms can trade them—those with high pollution control costs can buy shares from others that have lower control costs so long as the price is lower than the firm’s abatement cost.

Firms need incentives to invest in pollution control.

This trading opportunity encourages firms to invest in technologies and new ways of controlling emissions so as to free up shares that they can sell. And since the buying firms must purchase the additional “right” to pollute, they have incentives to invest in more efficient ways of controlling pollution. Overall, the objective of a particular desirable pollution amount can be met at the lowest cost in this manner and the regulator has little role, except to set the total cap and issue the shares. The firms and the market do the rest.

In this way, regulation adapts to the market.

Similarly with fisheries, a total annual allowable catch is determined and the fishermen in the fishery are granted individual shares in the total catch, often called ITQs or IVQs (individual tradable quotas or individual vessel quotas). The total cap can be reduced each year so that the shares are to a smaller allowable harvest until the harvest is at a level that is consistent with preserving the fish stock.

The shares should be tradable so that new fishermen can enter the fishery and more efficient fishermen can expand by buying the shares of less efficient fishermen. And importantly, through purchase of shares, vessels and crews can be taken out of the fishery, a major objective because most fisheries that are under threat are subject to over-harvest by too many vessels and crews chasing too few fish—the Tragedy of the Commons.

In all cases, these shares should be secure property rights with the same constitutional protections as for any other type of property. This security makes the market work—for the environment, for the natural resource, and for the users themselves. This is a necessary condition for effective environmental and natural resource policy.

With property rights security, owners can plan ahead with investment in pollution abatement technologies, knowing that their benefits will be captured in saved emission shares that can be banked. Fishermen can invest in new technologies that save the stock or its habitat, knowing that the value of their shares will grow with the vibrancy of the fish stock. And they can trade them when new opportunities develop or use the shares as collateral for loans and other investment funds. Security also makes the market work more effectively by reducing volatility. When share or allowance prices jump or fall for some exogenous reason, any banked shares can be sold (purchased) to smooth price patterns.

Finally, and perhaps most crucially, with secure property rights, regulators are restrained by the costs of the taking of property if new regulations reduce the value of the share. There may be reasons for regulatory change, but compensating owners for property and past investments that have benefited the environment reveals the opportunity cost of any policy change. Regulators then must seek funding through Congress or other means and this in itself is a useful process because legislative negotiations reveal social preferences and the weighing of the costs and benefits of alternative policies—environment, health, education, defense, infrastructure, and so forth.

U.S. pollution control costs have increased by over 300 percent since 1972.

Absent property rights security, regulators are much freer to adjust policies with little concern as to the costs involved because they are borne by shareholders. Further, the policy is subject to greater litigation challenge because the rights are not firm and with broader agency discretion, there is greater opportunity for other constituencies to seek to modify property. With secure property rights, constitutional guarantees constrain such litigious activities and promote greater stability in the environment.

So what has the U.S. done in this regard? Let’s take a look.

Sulfur Dioxide Allowance Trading.

In the 1960s there was growing awareness of the damage caused to lakes and forests from acid rain downwind from power plants that released sulfur dioxide into the atmosphere. In the same decade, economists Thomas Crocker and J.H. Dales proposed a property rights solution to sulfur dioxide emission problems with tradable emission shares. Instead of implementing this approach, the 1970 and 1977 Clean Air Act Amendments (CAAA) set national maximum concentrations of sulfur dioxide, and the states were charged with meeting those standards.

Most sulfur dioxide was released by electricity-generating utilities in the Midwest and North East that used high-sulfur coal as a fuel and often had older facilities. Under the regulations to reduce sulfur dioxide emissions, utilities were to add flue gas scrubbers (often at a cost of $10 million or more) even if low-sulfur coal was being burned and/or other new low-polluting equipment was being used. Advanced technology standards for reducing pollution were to be applied to any new generating plants put on board.

Owners of existing, less-efficient facilities had little incentive to build new ones or upgrade old ones that would require the new technologies, thus slowing the pace at which sulfur dioxide emissions were reduced.We won’t get into the politics of why the earlier Clean Air Act worked in this way, but it will come as no shock that it was due to constituent group politics and political and bureaucratic incentives.

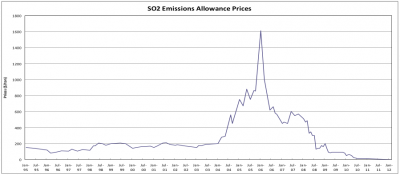

Not surprisingly, acid rain continued to be a problem. By 1990, U.S. pollution control costs had reached $125 billion annually, nearly a 300 percent increase in real terms from 1972. Finally, over twenty years after they were first suggested, property rights in the form of tradable emission permits were made part of Title IV of the 1990 Clean Air Act Amendments. An even tighter target was set and emission shares were given out to utilities in the upper Midwest and Eastern states.

The result was spectacular. They were a major success. Emissions were reduced by approximately 50 percent—more than under the original Clean Air Act and at much lower cost than the uniform standards previously used. The program’s long-term goal to reduce the amount of nationwide utility emissions of sulfur dioxide to 8.95 million tons was achieved by 2007 through the nationwide trading of emission shares. It has been estimated that abatement costs would have been over three times as high as they actually were to achieve this level of pollution reduction, $2.6 billion annually as compared to the actual program cost of $747 million.

The law required a two-phase gradual reduction of pollution through the use of emission shares. Phase I (1995–99) focused on the dirtiest plants and Phase II (2000 and after) included most other utilities. Under the legislation, firms were granted annual emission shares and then required to relinquish one for every ton of sulfur dioxide released. Shares could be banked by firms across both phases, and there was an active trading market in shares.

Property rights can reverse the global trend toward the collapse of fisheries.

Even with all of this success, there was programmatic danger. The emissions shares were vulnerable to agency discretion and adversarial litigation because in the legislation and in EPA policies they were explicitly declared not to be property rights.

By the late 1990s there was also growing concern about particulate emissions from electricity and their health effects. In 2002, the Bush Administration tried to amend the Clean Air Act to tighten controls on particulates, but the legislation did not pass. The EPA then attempted to implement its own program broadly within existing legislation. In 2005, the agency introduced the Clean Air Interstate Rule (CAIR) that further reduced the cap on sulfur dioxide and nitrogen oxide emissions, and focused more stringent requirements on certain facilities with high particulate releases in twenty-eight states.

To meet the lower cap quickly, the EPA required 2 emission shares to be relinquished for every ton of sulfur dioxide and 2.86 emission allowances for every ton by 2015, requirements that were not authorized in the original legislation. Allowance trading was still feasible, although the specialized regional restrictions in CAIR raised questions about the nationwide exchange program. In 2008, the DC Circuit Court of Appeals ruled that the EPA had gone beyond its delegated authority under the 1990 Clean Air Act Amendments in a variety of ways, and CAIR was rejected. Uncertainty regarding the status of the emission share trading program and the rights critical to it rose.

Another court ruling in 2010 further restricted EPA plans, and in July 2011, the agency implemented a new cross-state pollution rule (CSAPR). The new policy does not allow for cross-state emissions share trading, only exchanges within states, and the EPA has returned to command-and-control technology requirements.

Some 12 million emission shares that had been purchased and banked were not recognized, and their values collapsed, bringing losses of an estimated $3 billion with no takings implications. The future of any interstate trading program to reduce pollution is now questionable. Clearly, no firms would consider use permits to be credible property rights because history has shown they are not. The figure below shows the pattern of emission allocation prices that I calculated from 1995–2012.

Fishery ITQs

As with air pollution control, regulators in fisheries have used command-and-control regulations, but with little benefit. Fishermen have maneuvered around the restrictions and stocks have plummeted. In 1973, fishery economist Francis Christy outlined how property rights to fish created through individual transferable quotas could solve the problem. In 1986 and 1989, New Zealand and Iceland, two countries that depend on fisheries for a large portion of their economies, adopted ITQs. The United States did not follow suit until 1991.

As with air pollution control, the results have been beyond anyone’s wildest dreams in many cases. A recent study by my colleagues at the University of California at Santa Barbara and published in Science in 2008 found that after examining some 11,135 fisheries worldwide from 1950 to 2003, the implementation of catch shares as property rights halts, and even reverses, the global trend toward the widespread collapse of fisheries. This institutional change has the potential for greatly altering the future of global fish stocks.

Just as with tradable emission shares, these rights-based institutions have been more effective because they better align the harvest practices of fishers with practices that protect or enhance the fishery. The value of their quotas, which often can be major sources of wealth, depends on the long-term health of the stock. Hence, there are incentives for self and group monitoring of compliance. Moreover, because ITQs are transferable property rights, they provide the basis for trade among fishermen to reduce fishing pressure by buying quota and retiring vessels.

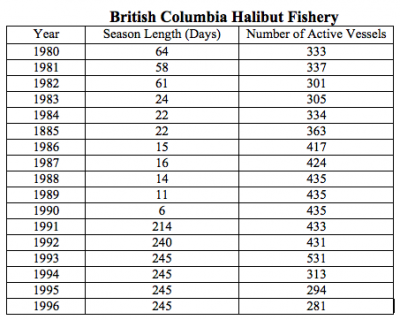

The data in the table below from a 2000 paper in the Journal of Law and Economics reveal the effects of tradable fishery shares or ITQs. Prior to the adoption of the ITQ program under regulation, there were fishing derbies, congestion, and gradual shortening of the fishing season. In 1990, the season length was only six days, which meant that all the halibut had to be caught at that time, frozen, and then shipped to market as less-valuable frozen halibut. After the ITQ program was implemented in 1990, the season expanded to 245 days, the number of vessels declined, and importantly, valuable fresh halibut could be available for most of the year.

But just as with emissions permits, there is regulatory risk and a threat to these ITQs. The strength of ITQ property rights varies. In New Zealand, quota ownership is viewed as a perpetual right to fish, and the rights can serve as collateral in financial markets. In contrast, ITQs in the United States have been controversial and are a weaker ownership right. In 1996, a four-year moratorium was placed on new ITQs under the Magnuson-Stevens Act, and the law included specific language stating that quota shares were a permit only, revocable any time and not private property—sound familiar?

Further, there were restrictions placed on transferability. In some U.S. fisheries, quotas are granted to the community or have restrictions on how many can be held by any fisherman in an effort to maintain a small-vessel, local fishery. Unfortunately, limiting exchange only weakens property rights and their ability to reduce harvest pressure and protect the fishery upon which these small communities depend.

Where property rights are weaker, sales values should be lower than in cases where rights are stronger, and short-term lease prices should be higher. With ownership uncertainty fishermen prefer to lease shares from one another than to purchase them. Comparing the ratio of quota lease prices to sales prices across fishers in the United States, New Zealand, and Canada, my colleagues Corbett Grainger and Christopher Costello found that the ratio values for the United States are significantly higher than in the other countries. This result supports the perception that the United States has more uncertain property rights to fishery use than its peer countries.

Conclusion

Can government credibly commit to property rights in environmental and natural resource use regulation? The answer is no. Politicians and bureaucratic officials appear not to be able to assign secure use rights. We must let the markets operate and bear the opportunity costs of any programmatic changes. If we don’t, there will be serious implications for the environment, natural resource stewardship, and for the American economy, given the total costs of environmental regulation.

Treating a trading system based on government created limitations (cap and trade) as if it were property is a corruption of the concept of property. It would be more appropriate to call these kinds of government controls either regulation or quasi-prohibition. A real solution to pollution based on property rights would work to apply the principles of real and intellectual property jurisprudence to the privatization of water and airways. A great first look at how this can be done is presented in the article found at the link below.

"The Practicality of Private Waterways" by J. Brian Phillips and Alan Germani