- Economics

- Politics, Institutions, and Public Opinion

- Law & Policy

- Civil Rights & Race

The latest fiscal cliff has led the President and Congress on a manic quest to find new sources of revenue for a federal government that is congenitally unable to live within its means. That extra revenue can come in only two ways. We can raise tax rates, clamp down on tax deductions, or do some combination of the two.

In approaching this issue, the Obama administration has had all of the wrong instincts. It has been adamant in its insistence that all changes on the revenue side increase the level of progressivity. The Tax Reform Act of 2012 thus moves the top marginal rates up to 39.6 percent, without accounting for the Medicare override of 3.8 percent that hits all taxpayers in the maximum tax bracket, making their combined rate 43.5 percent, which is above the Clinton norms. Since taxable deductions are not allowed against the Medicare excise tax, the administration has already taken a first step toward its goal of limiting the deductions that are available to high-income taxpayers.

Charitable Deductions in the Crosshairs

Its effort to generate new sources of revenue does not stop with the rise in the Medicare tax. On four separate occasions, President Obama has proposed limiting the deduction for charitable contributions to a maximum 28 percent. Ignoring the Medicare tax, that means a $1,000 contribution will generate at most $280 in tax deductions, or a nearly 30 percent reduction in the $396 in deductions allowed under current law.

Illustration by Barbara Kelley

The President’s proposal is not alone. The Bowles-Simpson commission proposes that taxpayers receive a credit equal to only 12 percent of their charitable deduction, but only to the extent that their charitable giving exceeds 2 percent of their adjusted gross income. The Domenici-Rivlin Debt Reduction Task Force is only slightly more generous in allowing a credit of 15 percent for all donations, without the 2 percent minimum threshold. Both these proposals slash the charitable deduction by over 40 percent.

The received progressive consensus mistakenly pushes hard on limiting charitable deductions and increasing the progressivity of the tax code. For all of its insistence on progressive taxes, it cannot identify the optimal level of progressivity within the system. The flat tax alternative that I have long championed has the great advantage of promoting economic stability by limiting Congress’s freedom to set tax rates for various sorts of transactions. Less widely noted, a flat tax significantly redistributes wealth already, for those with higher incomes pay more for their share of public goods than lower income people, even though those with lower incomes derive roughly the same level of personal security and other public goods that the government provides.

Indeed, as AEI’s Nicholas Eberstadt has noted, there has been a massive rise in transfer payments through entitlement programs. The advocates of redistribution are quick to trumpet its virtue, but slow to identify the optimal level of redistribution that does not undermine the incentives for productive work.

What is doubly ironic in this situation is that the champions of redistribution seek to neuter the single most effective device for redistribution that is available to modern societies—the charitable deduction. Charities do not specialize in wealth transfers from poor to rich. But, as Diana Aviv, the head of the Independent Sector, has pointed out in her testimony to Congress, private efforts to assist those in need are massive. In my view, they are far more efficient in getting aid to target groups than the United States government is.

It is tempting to think that the limitations on deductions will hurt the rich by cutting back on their deductions. But the burden will fall heavily on the recipients of charitable support, for as the price of making a charitable gift rises (anywhere from 30 to 100 percent), the level of charitable giving will decline. Hurt in the shuffle are, of course, the low-income beneficiaries of charity.

It is also important to note that voluntary charitable contributions are not subject to many of the serious worries that undermine regimes of high taxation. What the current tax deduction does, in effect, is to take income out of a rich person’s tax base if he or she is prepared to give it to others. It protects the incentive to create wealth, as people are far more likely to work hard to generate wealth whose distribution they can direct than to create wealth that the government snatches from them for its own purposes. The constant trade-off between the creation of wealth and the transfer of wealth is far less likely to occur with voluntary transactions than coerced ones.

Why Charities Matter

Why then would the government take steps to cut back on charitable giving? The most obvious explanation is both insidious and dangerous. It is to shrink the size of its main competitors in the private sector in order to increase the dependence of ordinary people on the federal government.

Another advantage of the charitable deduction is that it implements the Hayekian imperative of decentralized control over social resources. It was for just this purpose that Congress enacted the charitable deduction in 1917, four years after the adoption of the initial income tax of the Sixteenth Amendment. If we let the government collect money through high taxes, then remote bureaucrats determine who gets what benefits.

It is common for the champions of redistribution to ignore the political forces that operate nonstop in Washington DC that incentivize the transfer of wealth from the opponents of the powerful to their friends. That set of political forces is certainly at play in dealing with public largesse of all forms, as the dominant party can dictate which individuals and groups are allowed to participate in which programs. The expected consequence is greater dissipation of wealth in factional intrigue, and public expenditures in areas where they are not likely to do much good.

Decentralized control of spending changes that political dynamic entirely. The charitable deduction gives each person who makes a contribution to the public welfare a matching gift from the government, no questions asked. The kind of activities that should be eligible for these matching grants should be limited to charitable purposes that have proven their worth over time. Today, organizations whose operations are dedicated to charitable activities, broadly defined, count. That includes traditional charities dedicated to the alleviation of poverty, and also organizations devoted to religious, scientific, literary, and educational purposes.

Within these broad parameters, the charitable deduction ensures that no political elite gets to dictate the ways in which charitable dollars are spent. Indeed, one strength of the system is that it allows individuals and groups with wholly different agendas to get the same public benefit without having to convince their rivals to approve their expenditures. As such, the deduction does not alter the amount and direction of charitable activities that would take place in a non-tax world.

As such, the device has three important advantages. First, this non-discretionary subsidy increases the total amount of charitable activity, without increasing the role of the government in the collection or distribution of funds. Second, it still requires charitable institutions to persuade some potential donors that their mission is worthy of private support, which can only be done if organizations have some form of private monitoring by charitable boards and other external watchdogs. Third, the rise of charitable organizations attracts the civil participation of a large number of people who receive no direct cash payment for their charitable efforts. Charities, in sum, reduce the control of government over the lives of ordinary individuals. People in need now have other places to look for assistance.

Getting the Right Tax Structure

The champions of limiting the charitable deduction assume that balancing budgets is the primary objective of any sensible system of tax reform. But, in fact, they are incorrect. The first task is to figure out what the ideal tax structure is—what proportion of the tax burden ought to be paid by which citizens. Once that is in place, the next task is to determine the rates that need to be charged in order to bring revenues into line with expenditures.

In this regard, the correct solution is to have a flat tax and a full charitable deduction. In her December 2012 op-ed in the Wall Street Journal, Kim Dennis, the head of the Searle Freedom Trust, urged her fellow non-profit organizations to not support higher taxes on the wealthy in order to protect the present charitable deduction against direct attack. The conventional nonprofit thinking, of course, was that the willingness to give to charities would marginally increase with the size of the charitable deduction.

What was missing from their approach, as Dennis points out, was the simple point that any general tax increase is likely to reduce the income of the wealthiest, who often give the most to charitable activities.

As Ezra Klein has noted, in 2009, families who earned more than $200,000 participated in charitable activities that generated about $60 billion in charitable contributions—and people who generated $10 million or more in income averaged about $1.75 million in charitable contributions. These are not numbers to sneeze at.

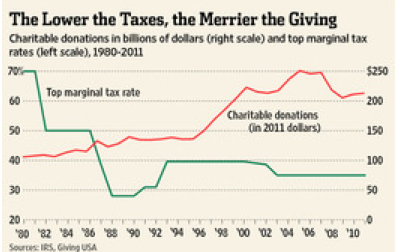

The good news is that, as John List of the University of Chicago has noted, charitable giving “has nearly doubled in real terms since 1990,” as the number of charitable organizations registered with the IRS has increased by nearly 60 percent. Indeed, as Dennis notes, the amount of charitable giving remains about the same regardless of changes in marginal tax rates, as this graph that accompanied Dennis’ op-ed shows. The point should not be astonishing. After all, the great philanthropy of the nineteenth century occurred when income tax rates were zero.

Photo credit: WSJ

Nonetheless I disagree with Dennis to this extent. It is uncertain whether the wealth effect will prove stronger than the deduction effect, given that at no previous time in our history has the charitable deduction been truncated in the form proposed today. In my view, it is just too dangerous to take the chance that the contributions will fall once the deduction is whittled away. There is in fact a better way to reduce the tax-benefits from the charitable deduction, which is quite simple: flatten the tax rate structure to promote higher growth than the current policies, which favor high marginal rates and multiple forms of taxation.

Indeed, the ideal tax is a flat consumption tax that exempts from taxation investment gains and savings from earned income until it is spent. The charitable deduction can easily fit into that system by one simple adjustment. When people direct funds that are in their tax-free savings account to eligible charities, those distributions should be non-taxable. These revenues don’t attract a tax when saved, and they don’t generate a deduction when paid out. That yields the same bottom line under the current income tax system, which taxes the revenues when earned only to offer a deduction when paid out.

The bottom line is that the charitable deduction should stay. It is the rest of the system that stands in desperate need of reform.