- Politics, Institutions, and Public Opinion

- State & Local

- California

Two of California’s historical ballot initiatives – one brought by government outsiders to limit government revenue, the other brought by government insiders to expand government revenue – face an uncertain future if changes to these laws appear on the 2016 ballot.

The legendary Proposition 13, passed overwhelmingly by the voters in 1978, was a tax revolt heard round the world. While limiting property taxes in California – to 1 percent of the acquisition price of property with annual tax increases of up to 2 percent depending on inflation – and setting strict vote requirements before other taxes could be raised, Proposition 13 also served as a springboard for centering the tax issue in national politics. The late Martin Anderson, a Hoover Institution Senior Fellow and top advisor to Ronald Reagan, told me that following the passage of Proposition 13, “The idea of Reagan cutting taxes was now politically viable and rolling. Proposition 13 was a clear political signal that the public was fed up with taxes.”

In the nearly four decades since Proposition 13 passed, it has been declared the “third rail” in California politics – any politician touches it risks defeat at the hands of voters. But now, SCA 5 – introduced by State Senators Holly Mitchell and Loni Hancock and supported by public labor unions and grassroots liberal organizations – is geared to alter the piece of Proposition 13 that covers commercial property. Proposition 13 treats commercial and residential property the same, just as they were treated prior to its passage.

The proposal would phase-in full assessment of most commercial property requiring annual reassessments to full market value. In an attempt to quell small business opposition, SCA 5 allows for a $500,000 exemption on personal property taxes used for business purposes such as machines. While small business might be pleased with the latter provision, substituting the exemption for the uncertainty of an annual, subjective, reassessment is no bargain for them.

Proponents claim it is only fair to close so-called loopholes dealing with business. They often refer to property deals constructed where no one owner takes possession of 50 percent of a commercial property so that the property is not re-assessed as required by Proposition 13 when change of ownership occurs. The provision determining change in ownership was set by the legislature; hence, it can be changed statutorily. But last legislative session, when an effort to do so was proposed by Democratic Assemblymembers, it stalled. There is renewed interest in pursuing this option again, but the outcome likely won’t be different. Certain interests – particularly public employee unions – do not want a fix this problem; they want to reassess all commercial property.

There is little chance that the proposed constitutional amendment will receive the two-thirds legislative vote necessary to make the ballot. Republican legislative leaders have stated that their caucuses oppose the change. There is doubt about how many Democrats would be willing to touch the “third rail” given that the measure’s fate in the legislature seems pre-ordained.

Even so, voters may have an opportunity to approve or reject a change to Proposition 13. The same public unions and grassroots groups that hailed SCA 5 are preparing to file their own initiative if it fails in the legislature. If the proposal makes the ballot it is sure to face a well-funded opposition from both the business and taxpayer advocate communities. In a recent PPIC poll, the idea of changing Proposition 13 to annually reassess commercial property while leaving the residential property tax as is (called the split roll) found favor with only 50 percent of respondents. Even without arguments offered about possible negative consequences – such as thousands of lost jobs – a split roll doesn’t start from an encouraging position for proponents.

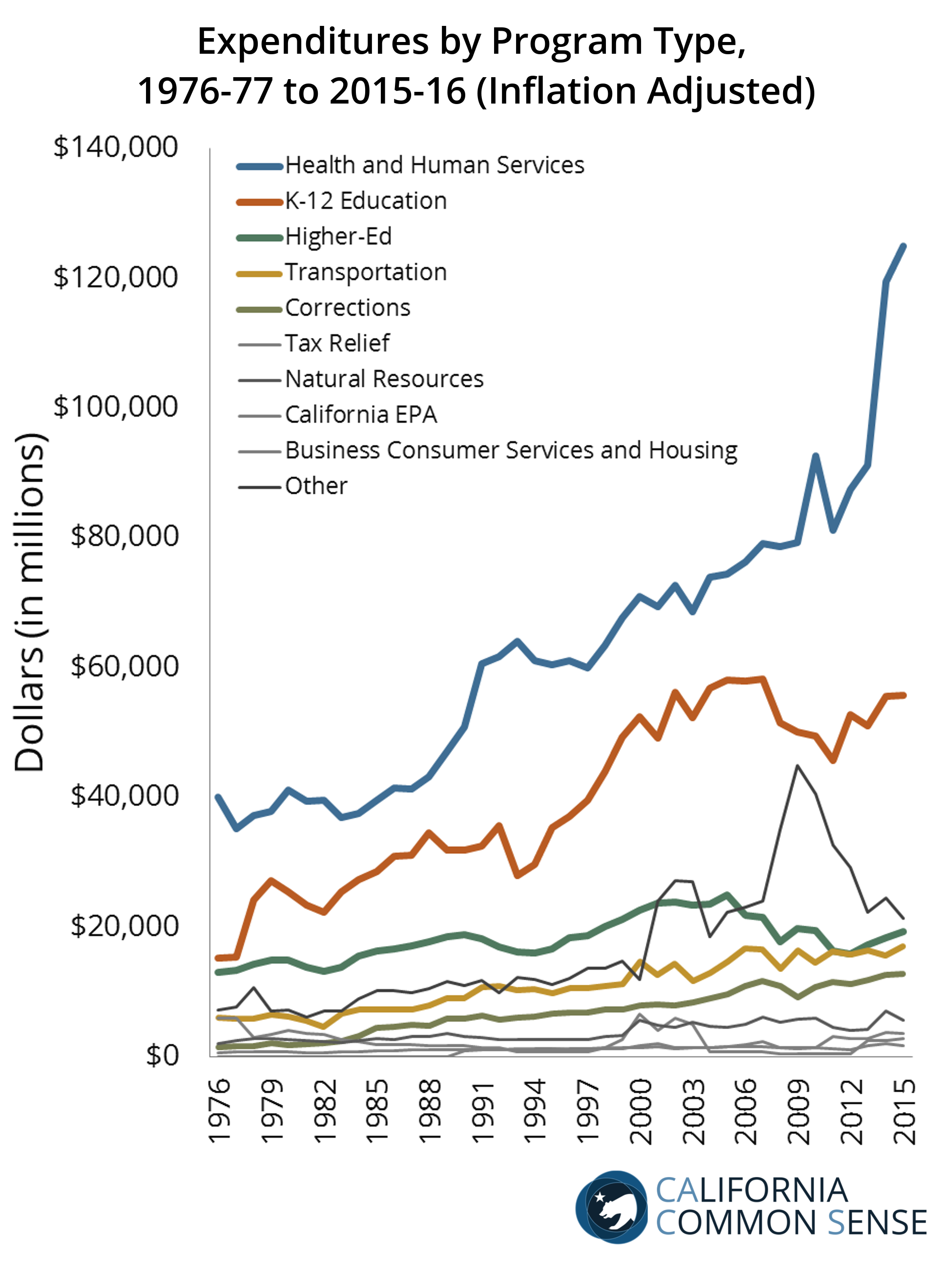

In 2012, Governor Jerry Brown led a coalition of public unions and government program advocates with some business support to pass Proposition 30, a $6 billion a year tax increase. Proposition 30 raised personal income taxes for seven years on taxpayers with taxable incomes of $250,000 or more. It also increased sales taxes by a quarter-cent for four years. Key to the “Yes on 30” argument was that the tax increase was needed to help the state recover from the Great Recession, a focus on funding education, and the text of the initiative stating that the funding would be temporary.

However, current discussions led by teachers unions are to extend or make permanent the Proposition 30 taxes. They argue California school funding would be jeopardized if Proposition 30 were allowed to expire with advocates talking about falling off a “fiscal cliff” if Proposition 30 ends. Analysis by both Standard and Poor’s and the Legislative Analyst’s Office determined that the state’s economic growth would avert this “fiscal cliff” scenario. Governor Brown, publically, is keeping to his pledge not to delay the temporary tax’s expiration.

However, there are two scenarios in which the taxes could continue. One would be another initiative measure to lengthen or make permanent the temporary status of Proposition 30. The second is to change some of the details of Proposition 30 – say eliminate the sales tax increase and cut a percentage off the income tax increase – and introduce it as a new tax, not as severe, but something needed to fill the hole created by the end of Proposition 30, which could open a loophole in Governor Brown’s pledge to gain his support. Proponents, though, may run into problems with voters on extending Proposition 30. The same PPIC poll found that 47 percent of respondents would oppose extending the tax with another 16 percent saying they’d oppose efforts to make it permanent.

One of the unusual aspects driving the Proposition 13 split roll and Proposition 30 extension discussions is the difference of opinions and strategies amongst public unions. Teachers unions have been the biggest beneficiaries of Proposition 30. But other unions, such as the SEIU, feel left out. A property tax increase would benefit its members, especially on the local government level. Some of the effort behind the Proposition 13 split roll may be a maneuver by these public unions to force the teachers unions to work together on one tax issue that would benefit all public labor groups. If two tax increases end up on the ballot there is less likelihood either would pass.

With little hope of either of these tax provisions passing out of the legislature, thanks to the Democrats losing their two-thirds majority in 2014, any action will take place on the ballot. But first, proponents must get the measures onto the ballot, which will be the first test of the issues’ public sentiment.

Proposition 13

Taxpayer advocate Howard Jarvis’ 1978 Proposition 13 campaign was the reaction to a decade of rapidly rising property tax reassessments. Passed with 65 percent of the vote, it sought to stem property tax growth and impose strict tax restrictions on elected officials by capping property tax rates at 1percent of assessed value, limiting assessed value increases at 2 percent per year (or to market value at change of ownership), and imposed a two-thirds vote requirement for elected officials to increase tax rates or create new taxes.