- Economics

- US Labor Market

- Budget & Spending

- Monetary Policy

- Law & Policy

- Regulation & Property Rights

- History

- Economic

- Politics, Institutions, and Public Opinion

Is the American Recovery and Reinvestment Act of 2009 working? Ever since the act was passed almost a year ago, mere weeks after President Barack Obama took office, the question has been hotly debated. Administration economists cited Keynesian models that predicted that the $787 billion stimulus package would increase gross domestic product by enough to create 3.6 million jobs. Our research showed that more modern macroeconomic models predicted an impact on gross domestic product only one-sixth as large. Estimates by economist and Hoover senior fellow Robert J. Barro predicted an impact not significantly different from zero.

Data collected during the months after the act’s passage allowed us to put aside models to see what actually happened.

Consider first the part of the package that consists of government transfers and rebates. These include one-time payments of $250 to eligible individuals receiving Social Security, Supplemental Security Income, veterans’ benefits, or railroad retirement benefits and temporary reductions in income tax withholding for a refundable tax credit of up to $400 for individuals and $800 for families with incomes below certain thresholds. Those payments, which began last March, were intended to increase consumption and thus help jump-start the economy. Now that a good fraction of those actions have taken place, we can assess their impact.

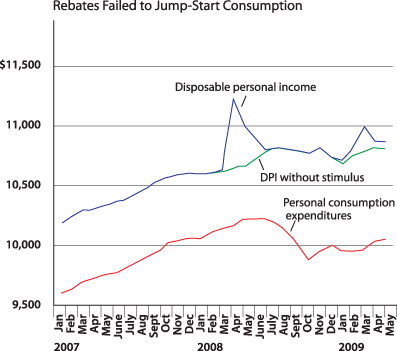

ONLY A TEMPORARY BOOST TO INCOME

The chart on the opposite page shows income and consumption through July 2009. Consider first the part of the figure that pertains to spring 2009; observe that disposable personal income (DPI)—the total amount of income people have left to spend after they pay taxes and receive transfers from the government—jumped. That increase is due to the transfer and rebate payments in the 2009 stimulus package. As the chart also shows, however, there was no noticeable impact on personal consumption expenditures. Because the boost to income was temporary, at best only a small fraction was consumed.

This is exactly what one would expect from permanent income or life cycle theories of consumption, which argue that temporary changes in income have little effect on consumption. Those theories, developed by Milton Friedman and Franco Modigliani fifty years ago, have been empirically tested many times. They are much more accurate than simple Keynesian theories of consumption; thus the lack of an impact should not be surprising.

Indeed, anyone who had looked at the Bush administration’s Economic Stimulus Act of 2008 would have found plenty of evidence that temporary payments of this kind would not jump-start consumption. That package made one-time payments and rebates to people in the spring of 2008, but, as the chart shows, failed to stimulate consumption as had been hoped. Some argued that other factors, such as high oil and gasoline prices, caused consumption to fall and that it would have been even lower without the stimulus, but no significant impact has been found even after controlling for oil prices.

Now we turn to the government spending part of the stimulus package. The Obama administration points to the sharp reduction in the decline in real GDP from the first to the second quarter of 2009 as evidence that the package is working. Economic growth was minus 6.4 percent in the first quarter and minus 1 percent in the second quarter; thus the implied improvement of 5.4 percentage points is indeed big. But how much of that improved growth rate can be attributed to higher government spending due to the stimulus?

If we rely on model predictions, again we see disagreement and debate. According to our research with modern macroeconomic models, the increase in government spending would add less than 1 percentage point, a relatively small portion. The model predictions cited by the administration’s economists suggest a much larger portion: 2 to 3 percentage points. Barro’s model predicts zero.

Let’s look at the data on the contributions of government spending and other components of GDP to the 5.4-point improvement. By far the largest contributor to the improvement was investment—which went from minus 9 percent to minus 3.2 percent, an improvement of 5.8 percentage points and more than enough to explain the improved GDP growth. Investments by private firms in plant, equipment, and inventories, rather than residential investment, were the major contributors to the investment improvement. In contrast, consumption was a negative contributor to the change in GDP growth because consumption growth declined after the passage of the stimulus package.

RESILIENCE IN THE PRIVATE SECTOR

One is hard put to see which specific items in the stimulus act could have arrested the decline in business investment by such a magnitude. When one looks at monthly investment indicators—such as new orders for nondefense capital goods—one sees a flattening out beginning early in the first quarter of 2009, well before the package went into operation. The free fall of investment orders caused by the financial panic of fall 2008 had stabilized substantially by January 2009, and investment has remained relatively stable since then. This created the residue of a large negative growth rate from the fourth quarter of 2008 to the first quarter of 2009 and then moderation from the first quarter to the second of 2009. There is no plausible role for the fiscal stimulus here.

Direct evidence of an impact by government spending can be found in 1.8 percentage points of the 5.4-point improvement from the first to the second quarter of 2009. More than half of this contribution, however, was due to defense spending that was not part of the stimulus package. Of the entire $787 billion stimulus package, only $4.5 billion went to federal purchases and $17.7 billion to state and local purchases in the second quarter. The growth improvement in the second quarter must have been largely due to factors other than the stimulus package.

New data will reveal more in the months to come, but the evidence so far is that the government transfers and rebates did not stimulate consumption at all, and that the resilience of the private sector after the fall 2008 panic—not the fiscal stimulus program—deserved the lion’s share of the credit for the impressive growth improvement from the first to the second quarter of 2009. As the economic recovery takes hold, it is important to continue assessing the role played by the stimulus package and other factors. Such assessments can guide future policy makers in designing effective policy responses to economic downturns.