By Jonathan Movroydis

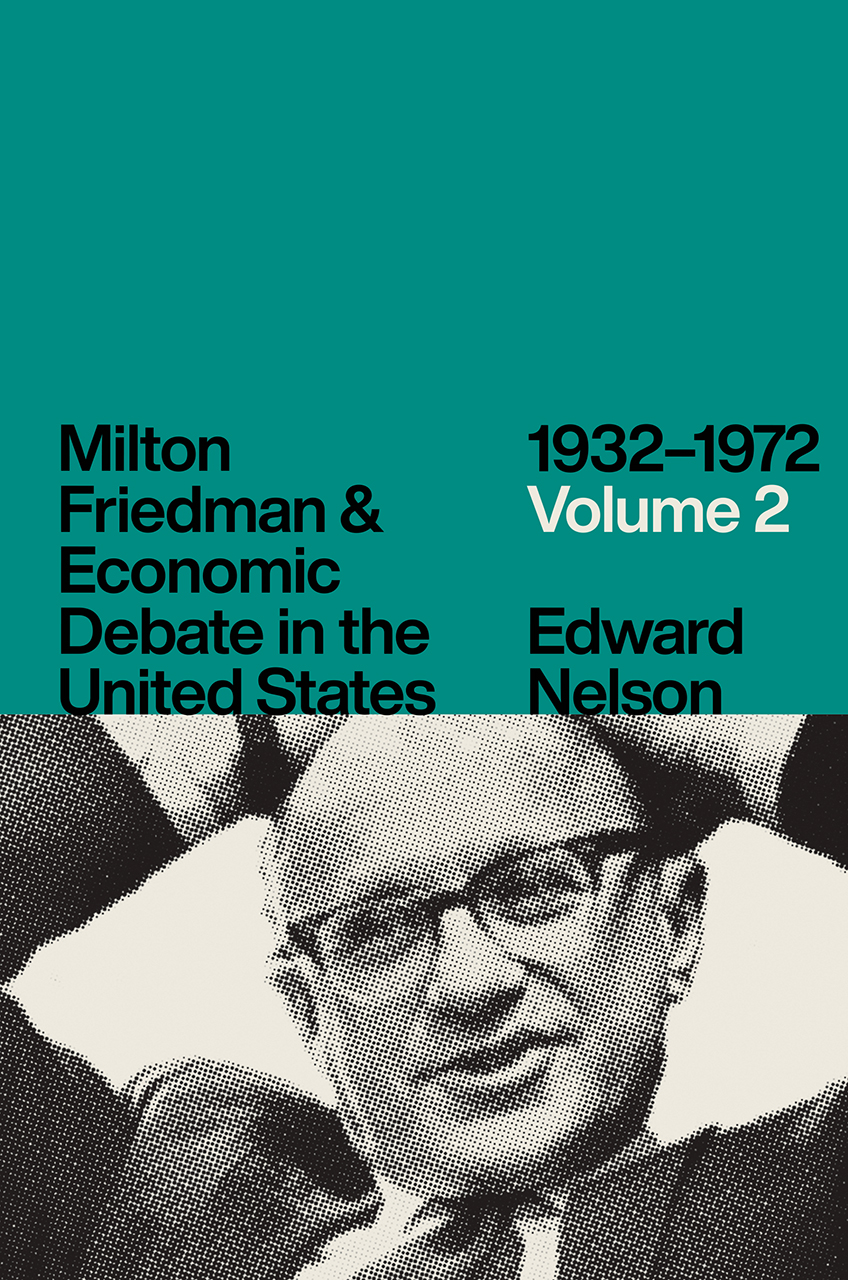

In this interview, recorded on February 10, 2021, Edward Nelson, an economist for the US Federal Reserve Board, discusses his new two-volume work, Milton Friedman and Economic Debate in the United States, 1932–1972. In it, Nelson describes the evolution of the late senior fellow Milton Friedman’s beliefs about the role of monetary policy in the US economy. Friedman advocated for its role in supporting income growth and preventing high rates of inflation, especially in arguments against contemporaries who favored government regulation and controls on prices and wages as a means of stabilizing the economy. In addition, Nelson explains the history of Friedman’s relationship with the late distinguished fellow George P. Shultz, particularly when the latter worked in the Nixon administration in a series of economic posts. The two would work together on establishing flexible exchange rates following the collapse of the Bretton Woods system in 1971.

This conversation also includes commentary about Friedman’s research and career by John B. Taylor, George P. Shultz Senior Fellow in Economics. The discussion references Nelson’s participation earlier the same day in a seminar about the volumes, convened by Hoover’s Economic Policy Working Group, which is chaired by Taylor.

Edward Nelson, what inspired you to write the two volumes of Milton Friedman and Economic Debate in the United States, 1939–1972?

Edward Nelson: I have always been interested in Milton Friedman's studies on monetary economics, and I was conscious of the fact that there was a lot of enduring interest in Friedman. Much has been written about Friedman, but his life has not been covered by anyone with a specialized research background in monetary economics. Economics is a very diverse field. One can be an expert in microeconomics and not necessarily be proficient in monetary policy, and vice versa. And one can have knowledge about the analytical aspects of monetary economics while not necessarily knowing much about that same field’s historical or policy details.

I have, I believe it is fair to say, a strong background in monetary economics, including research on the historical behavior of inflation and unemployment and how the course of monetary policy has been related to them. I have also researched extensively the history of the Federal Reserve, especially its post–World War II history. This book is unique also in including extensive recollections given to me by Friedman’s longtime coauthor Anna Schwartz, whom I knew very well and with whom I wrote a couple of papers about Friedman after he passed away.

Taking these pieces of my background and research together, I felt that I was well positioned to make a contribution that provided a detailed treatment of Friedman’s career and research, one written in a way that was informed by my own interest in and background in monetary economics.

John B. Taylor: What Ed has accomplished is monumental. The coverage is superb, and there is a third volume coming out soon. It's just amazing how much Ed has been able to bring to life about Friedman’s work.

In terms of this forty-year period, 1932 to 1972, will you provide an overview about Milton Friedman's views on monetary policy and how they square with those of some of the people he was debating?

Edward Nelson: There is quite a big discrepancy between Friedman's views in the years leading up to 1948 and the views that he developed afterward.

In the early 1940s, Friedman was very skeptical about monetary policy. He was strongly disposed toward using fiscal policy—that is, settings of federal taxes and government expenditures—as the key element in a strategy of manipulating aggregate demand. During this period, while working as an economist at the Department of the Treasury, he actually coauthored a book about taxing to prevent inflation.

Later in that decade, probably because of the research he was conducting with Anna Schwartz but also partly because Friedman was impressed by how the policy stance of the Federal Reserve was promoting high rates of inflation, he became more positively disposed toward monetary policy.

Over this period, Friedman had established himself as a very well-regarded microeconomist, and he won the Clark medal in 1951 for his work in microeconomics. But he was increasingly becoming attracted to macroeconomics. Once he had adopted his new views on monetary matters in the early 1950s, he started laying down markers that created a lot of macroeconomic debates in the 1960s.

In the late 1950s, he met with Federal Reserve officials and criticized their policy, because he thought that they were not looking at monetary aggregates adequately and were misjudging the extent to which the Federal Reserve could affect the money supply.

In the 1960s, Friedman had debates with the likes of James Tobin, an economist at Yale University. Tobin was very bullish about the extent to which the Kennedy and Johnson administrations could set ambitious targets regarding US economic activity while controlling inflation through measures such as “guideposts,” which basically amounted to the federal government making recommendations to firms and labor organizations about upper limits on their increases in wages and prices.

Friedman also had arguments with other leading Keynesian economists, including Paul Samuelson and Robert Solow, who also believed in direct government intervention or guidance in the wage- and price-setting process, instead of Friedman’s preferred approach, in which wages and prices would be market determined and would respond to monetary conditions that the authorities had charted out.

In these volumes, you devote some time to when Friedman was a young economist working in the US government during the 1930s. What were his perspectives about economic policy during the depression and, subsequently, the Second World War?

Edward Nelson: I think Friedman has been underestimated or caricatured in the sense that people think he was virulently against the New Deal. I think it's more accurate to say that he thought that monetary policy was mismanaged during the Great Depression. However, he did accept the basic premise that once the Great Depression was in motion, the government had to step in and take active measures to revive the economy.

He didn’t demonize Franklin Delano Roosevelt or John Maynard Keynes. Friedman thought that FDR’s 1932 inaugural address, in which he said “there is nothing to fear but fear itself,” had set the right tone for the nation. Friedman also supported the creation of the FDIC (Federal Deposit Insurance Corporation). He wasn't sympathetic to some of the interventionist approaches the Roosevelt administration took in regulating specific industries. He didn’t agree that these particular types of supply-side policies contributed to economic recovery. He believed that concentrating on major government actions to stimulate demand and restore confidence in the economy, especially its monetary system, would have been a more appropriate policy response.

What were his positions on monetary policy during the postwar period, when the country experienced high rates of economic growth?

Certainly Friedman accepted that the postwar period had been a very good time for real income growth. Many people attributed this success to the Keynesian revolution and increased government intervention in the economy. Friedman argued against these interpretations. He believed the high rates of growth were due in part to the fact that monetary policy was much more stable after the war. Such stability enabled economic activity in the private sector to flourish. When growth slowed, starting in the 1970s, Friedman believed this was because of increased government intervention and regulation that had adversely affected the supply side of the economy.

Will you mention some ways in which Milton Friedman’s ideas became influential and affected the way policy makers enacted their measures?

In the case of Richard Nixon, one of the conduits was George P. Shultz, who had known Friedman when they were both at the University of Chicago. Friedman had known Nixon since the 1968 campaign. Though Friedman didn’t see Nixon very often, Shultz would invite Friedman in for meetings with the president when Shultz joined Nixon’s cabinet and held a succession of economic posts (secretary of labor, director of the Office of Management and Budget, and secretary of the Treasury).

At the time, the Bretton Woods international monetary system was breaking down. Friedman was around to say, “This is not the end of the world, to break away from the Bretton Woods arrangements. We can have a stable system without them.” Friedman was an important voice articulating that position. Nixon was impressed by Friedman because of the economist’s ability to distill complex economic issues in a manner that was understandable.

One of the curiosities of another economic giant of this period, Paul Samuelson, is that while he was one of the best-known economists of the time, in part because of his widely assigned undergraduate textbooks, he had a lot of trouble breaking things down into their simplest forms. So his textbooks are full of academic qualifications and quite abstract explanations. Conversely, Friedman was very good at making things concrete and understandable—a talent that I think made him very good company for politicians who were also free-market oriented. Friedman did have a policy disagreement with Nixon over wage and price controls in 1971. It wasn’t anything personal, however, since the two of them continued to have a friendly relationship, and Nixon subsequently phoned Friedman when Friedman reached milestones in his life, including winning the Nobel prize in 1976.

John Taylor: I think former Federal Reserve chairman Arthur Burns should be mentioned as well. Burns was Friedman’s former teacher and also free-market oriented. He diverged from his conservative economic principles by advocating for wage and price controls during the Nixon administration. Friedman wasn’t hesitant about criticizing Burns, whom he considered a friend. Friedman also worked behind the scenes with Shultz to institute a flexible exchange range rate following the collapse of Bretton Woods in 1971. These debates are also highlighted in Ed’s book.

Edward Nelson: Yes. I think all those points are very important. Shultz really lived up to Friedman's expectations for him in government, and Burns did not. Shultz was very consistently against wage and price controls. In terms of Bretton Woods, Friedman was very much involved in talking with Shultz about advocating a system of flexible exchange rates, whose adoption provided a way of addressing the international balance of payments.

What do you hope people gain from reading this book?

Edward Nelson: I hope that people will get a better picture of how the consensus about monetary policy evolved. Just before COVID-19 emerged, I watched a conversation with Emi Nakamura and Jón Steinsson, coauthors of a paper about the history of the National Bureau of Economic Research. Steinsson, who is one of the leading young monetary theorists of today, said that it’s hard to describe Friedman's work in terms of it being a criticism of Keynesianism because it so closely resembles the modern, New Keynesian view of monetary policy.

What this indicates is that Friedman had a lot of influence on the modern consensus of monetary policy. Today much of the professional consensus about economic policy reflects his view, which was a minority position in the early postwar decades, that monetary policy should be central to managing aggregate demand, and Friedman has also helped shape modern discussions of the relationship between inflation and unemployment.

I also hope that the book demonstrates how influential Friedman was on the development of economic thinking and also on policy, through his research, debates with other economists, public policy activity, and role in advising national leaders.

I first met Friedman in 1992 when, as something of an uppity undergraduate, I arranged to pay a visit him at the Hoover Institution while I was on vacation in the United States from Australia. So it’s nice to return and be able to have participated in a seminar on Friedman at Hoover, where he spent the final three decades of his life and career.

John B. Taylor: One thing that's really nice about the two volumes is that they portray Friedman’s beliefs about the economy at the time. I think that's very important, because many of the questions we asked Ed in today’s session were, “What would Milton say and do now?” I think maybe Milton would say, “We don't know. We just don't know.” However, we can see what shaped Friedman’s thinking in the context of the environment in which he lived. I think that’s very valuable in helping us better understand developments in US monetary policy.