- State & Local

- California Decides

- Empowering State and Local Governance

This primer examines the administrative, empirical, and economic case against wealth taxation at the state and national levels. Wealth taxes are a relic of earlier fiscal systems where tangible, immobile assets were the only practical tax base. As financial markets expanded and capital became more mobile, advanced economies shifted toward income and consumption taxes — and most countries that experimented with modern wealth taxes ultimately repealed them.

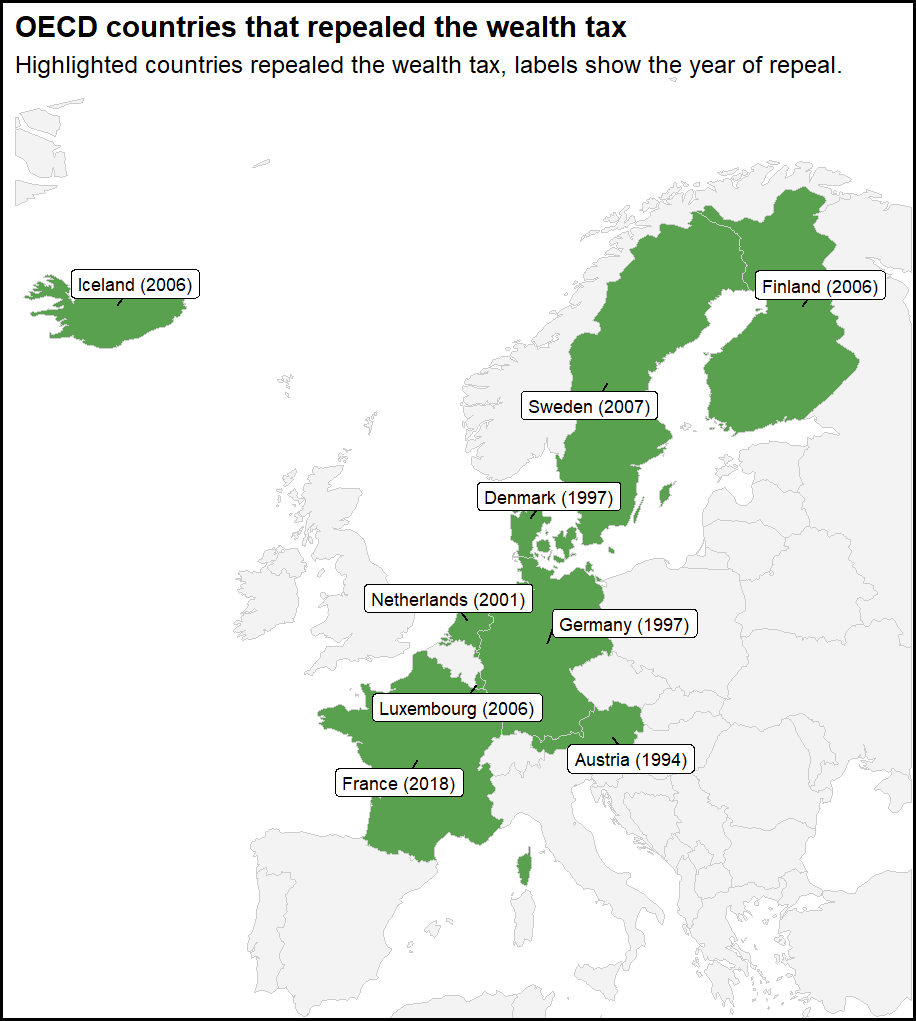

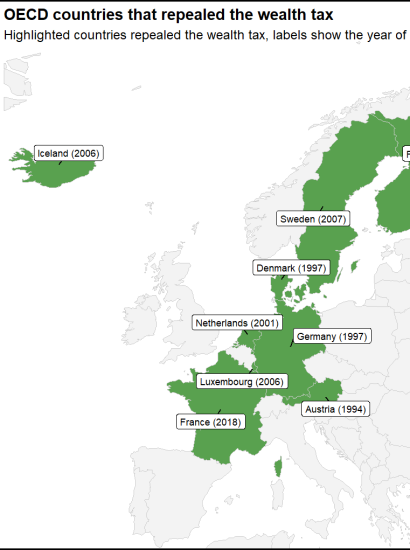

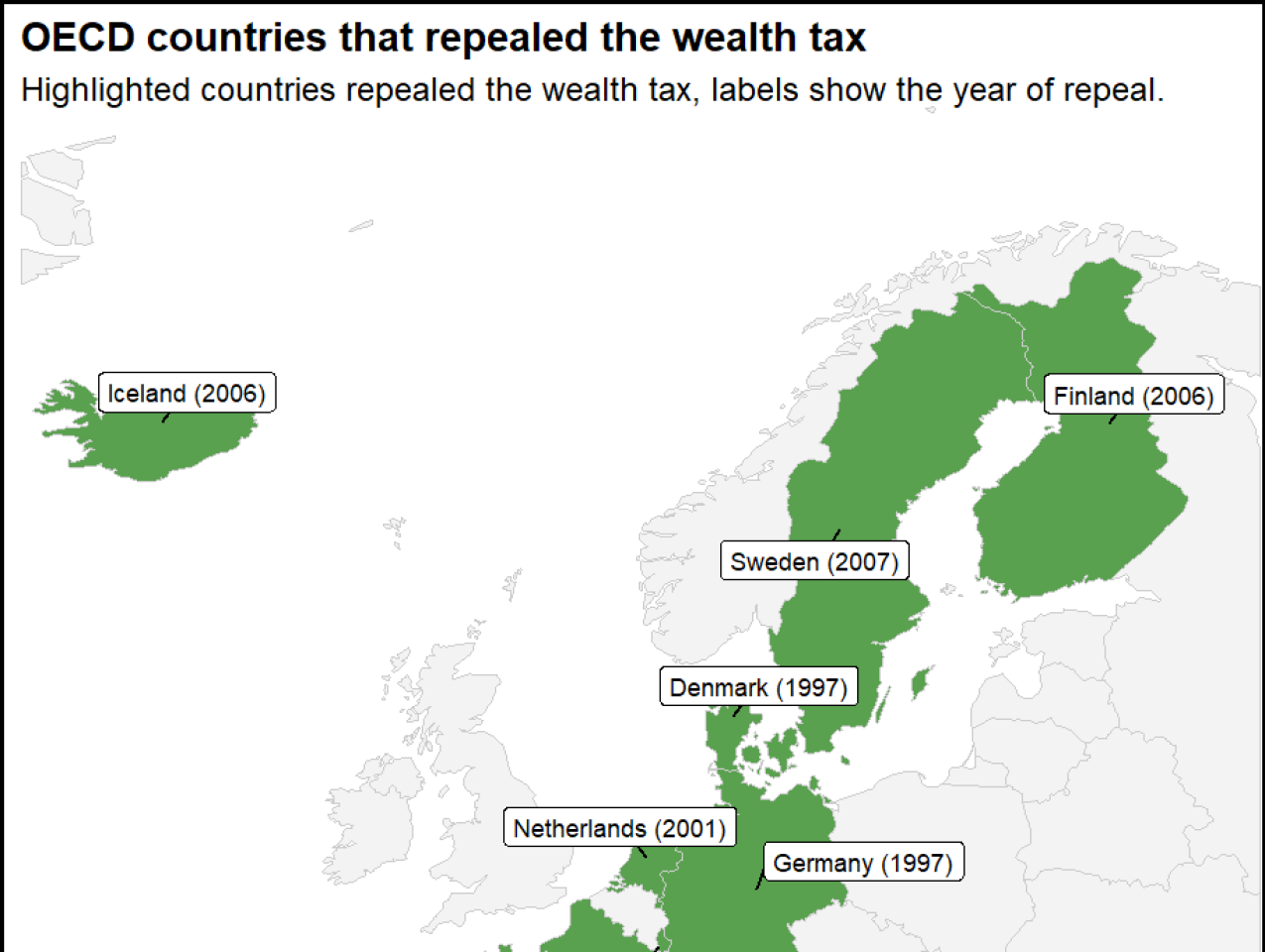

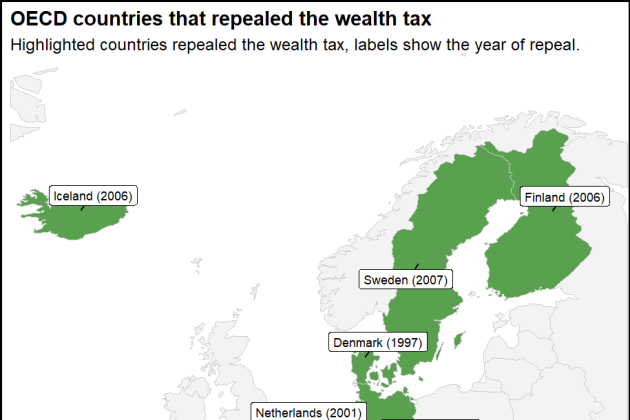

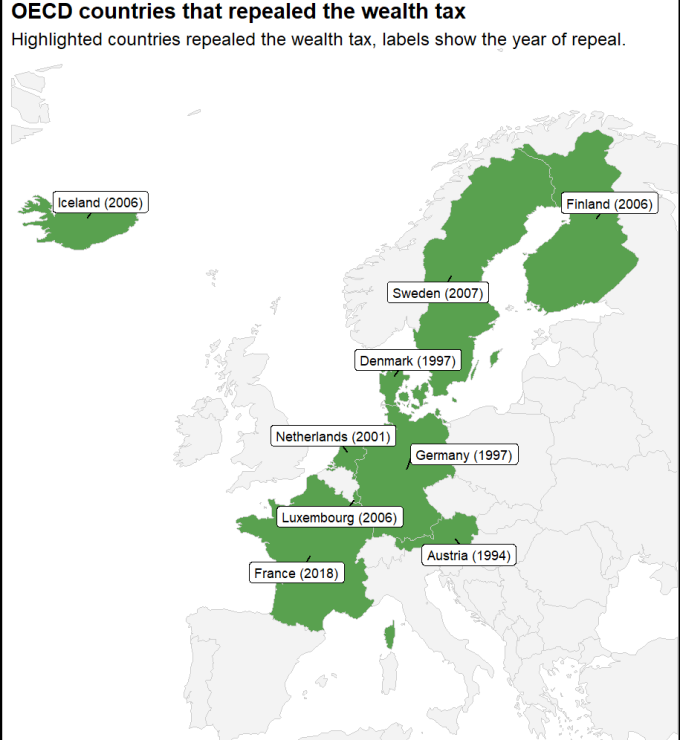

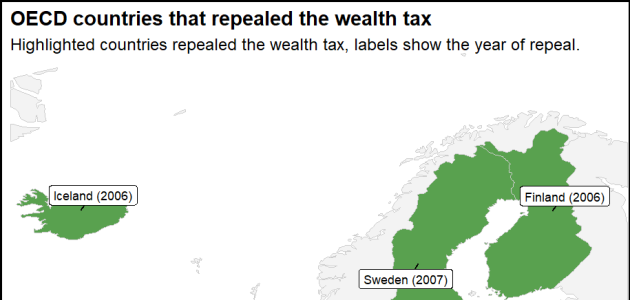

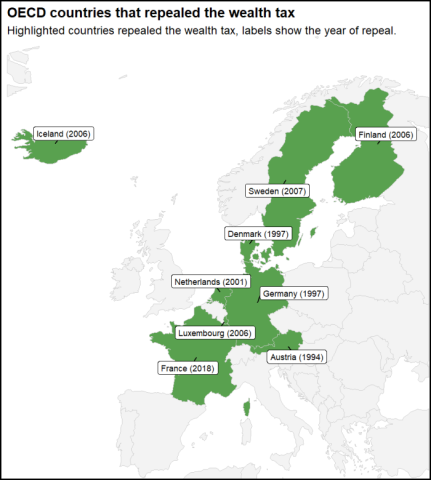

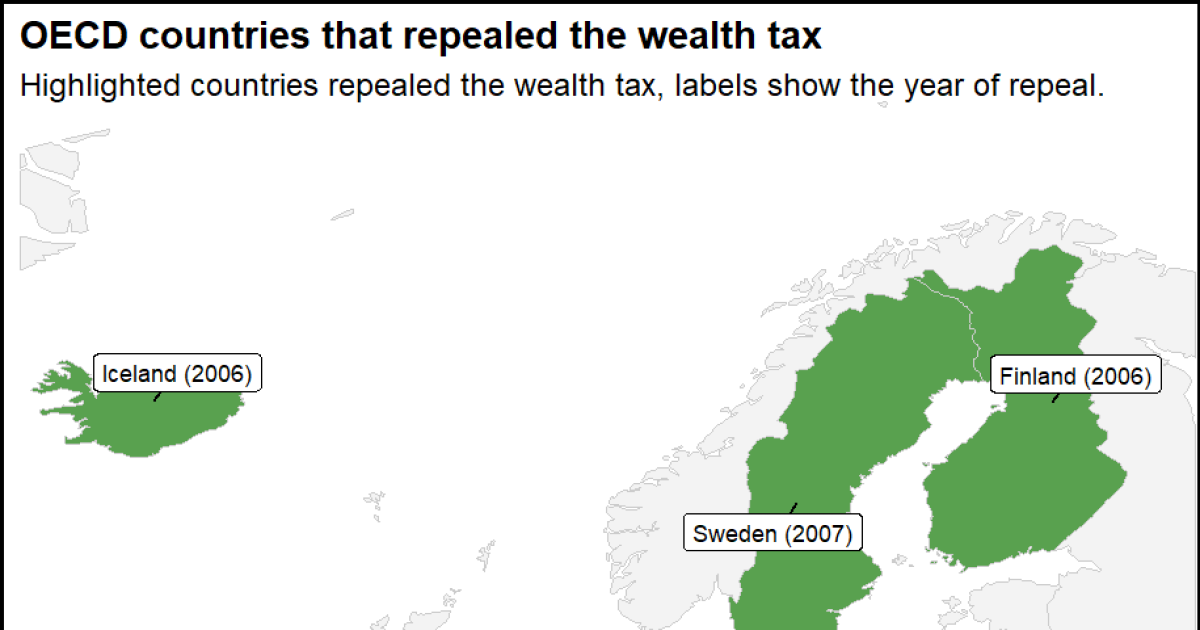

The primers showcases the historical retreat of wealth taxes — of the twelve OECD countries that levied wealth taxes in 1990, nine had repealed them by 2025. This was caused by the administrative complexity of the tax and the capital flight it motivated, leading to disappointing revenue.

In particular:

- Wealth tax revenue estimates lack credibility. Wealth tax revenue projections rest on untested assumptions about asset valuation and taxpayer behavior. Without reliable methods for valuing underlying assets or estimating behavioral responses, projected revenues lack credibility.

- Wealth taxes are distortionary. Wealth taxes distort capital allocation and reduce incentives to save, invest, and build businesses. Because wealth tax bases are highly elastic, taxpayer responses through avoidance, evasion, and migration substantially erode the tax base over time.

- Fragile foundations. Current wealth tax proposals reflect political pressure rather than new evidence of their efficacy as an efficient tax or necessity for raising public sector revenue.

Drawing on historical and cross-country evidence — including the recent wave of state-level proposals in California, Washington, and Illinois — the primer documents how wealth tax revenue estimates consistently overstate what these taxes can deliver, and how the resulting shortfalls create political incentives to expand the tax base beyond its original targets.