Washington Post columnist Megan McArdle moderated a dynamic conversation with Hoover senior fellows John Cochrane (a.k.a. the Grumpy Economist and GoodFellow), Valerie Ramey, and Ross Levine on a defining question of the American experiment: why has the United States been such an enduring outlier in prosperity and can it remain so? For more than a century, America has been the world’s most prosperous large nation, yet confidence in the American Dream is faltering.

Drawing on their expertise in economic growth, public policy, and financial systems, the discussion examined the sources of America’s exceptionalism, from freedom and federalism to a culture that rewards risk-taking and tolerates failure and ask whether those strengths are now being undermined. Are the institutions that once expanded opportunity still doing so, or have they become barriers to growth and mobility?

The panel considered what it will take to restore a sense of dynamism and possibility in the American economy, and whether current policies are strengthening that future or quietly putting it at risk.

- Freedom is not an accident of history. It is the result of ideas tested over time, shaped by debate and sustained by institutions and citizens willing to defend them. The United States was founded on an audacious premise that a free people could govern themselves, that liberty could endure, not through force, but through law, not through unanimity, but through argument.

- I have a dream that one day this nation will rise up and live up the true meaning of its creed, and

- Not through tradition alone, but continued renewal across generations. Americans have wrestled with enduring questions. What does citizenship require? What responsibilities accompany freedom? How should power be restrained? And how should a free society respond to moments of danger, disruption, and change? Today, those questions are once again, urgent. Democratic societies face pressure at home and abroad. New technologies are reshaping economies and institutions. Authoritarian systems challenge the principles of open societies, and Americans are called to reconsider how freedom can be preserved in a rapidly changing world. The ideas that made us dialogues on freedom is dedicated to examining these challenges through serious inquiry and open debate. Across the year, the Hoover Institution will bring leading voices to explore the foundations of American freedom from citizenship and education to innovation, governance, national security, and global competition. Each dialogue connects enduring principles to contemporary choices, asking not only where we have been, but where we're going. These conversations are not about prescribed dogma or doctrine. They're grounded and open, serious and constructive dialogue. They are about a deeper understanding and about responsibility and about the ideas that have made the United States and will shape its future. We hold these truths to be self-evident that all men are created equal, and that they are endowed by their creator with certain unalienable rights. That among these are life, liberty, and the pursuit of happiness.

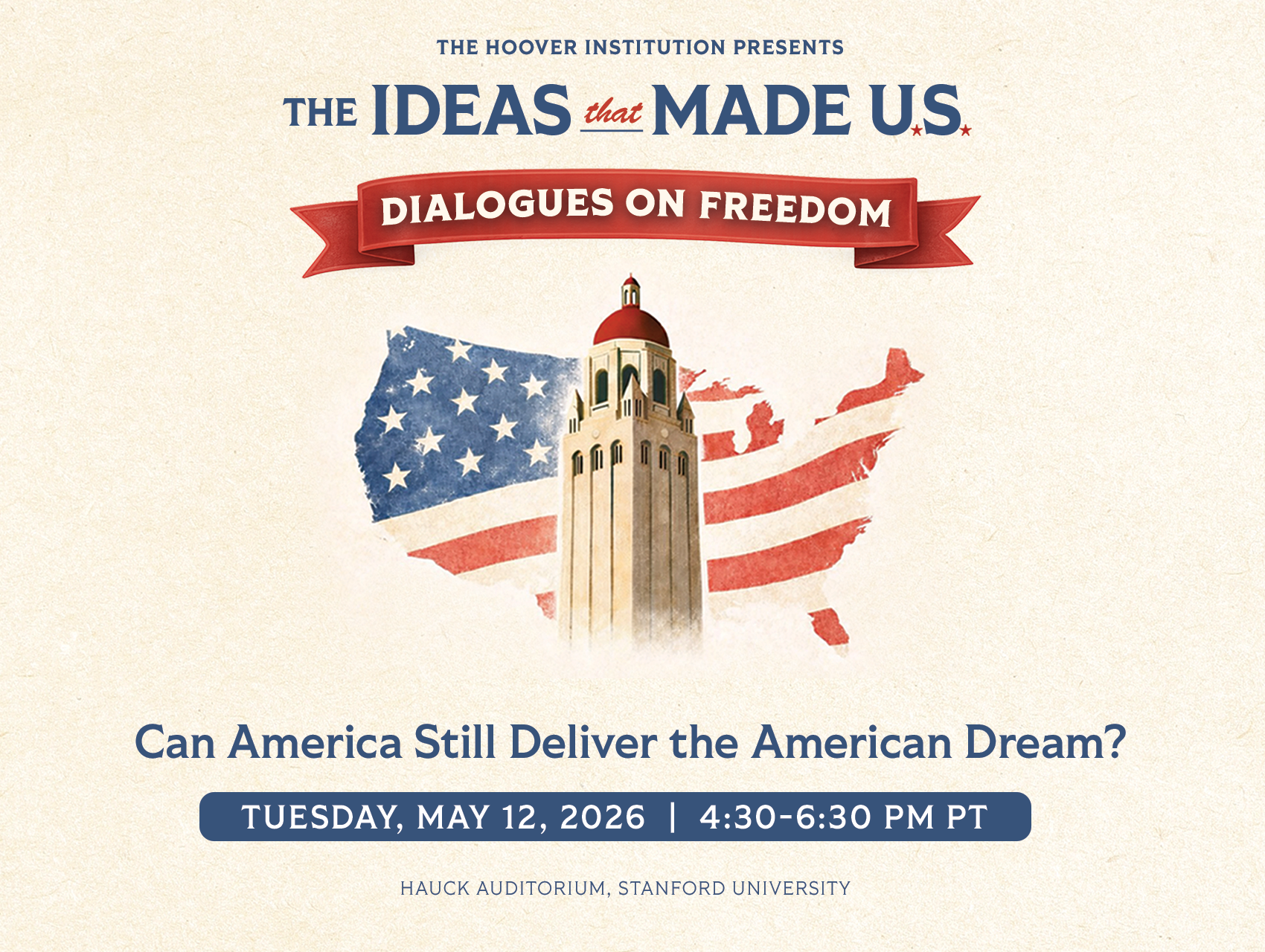

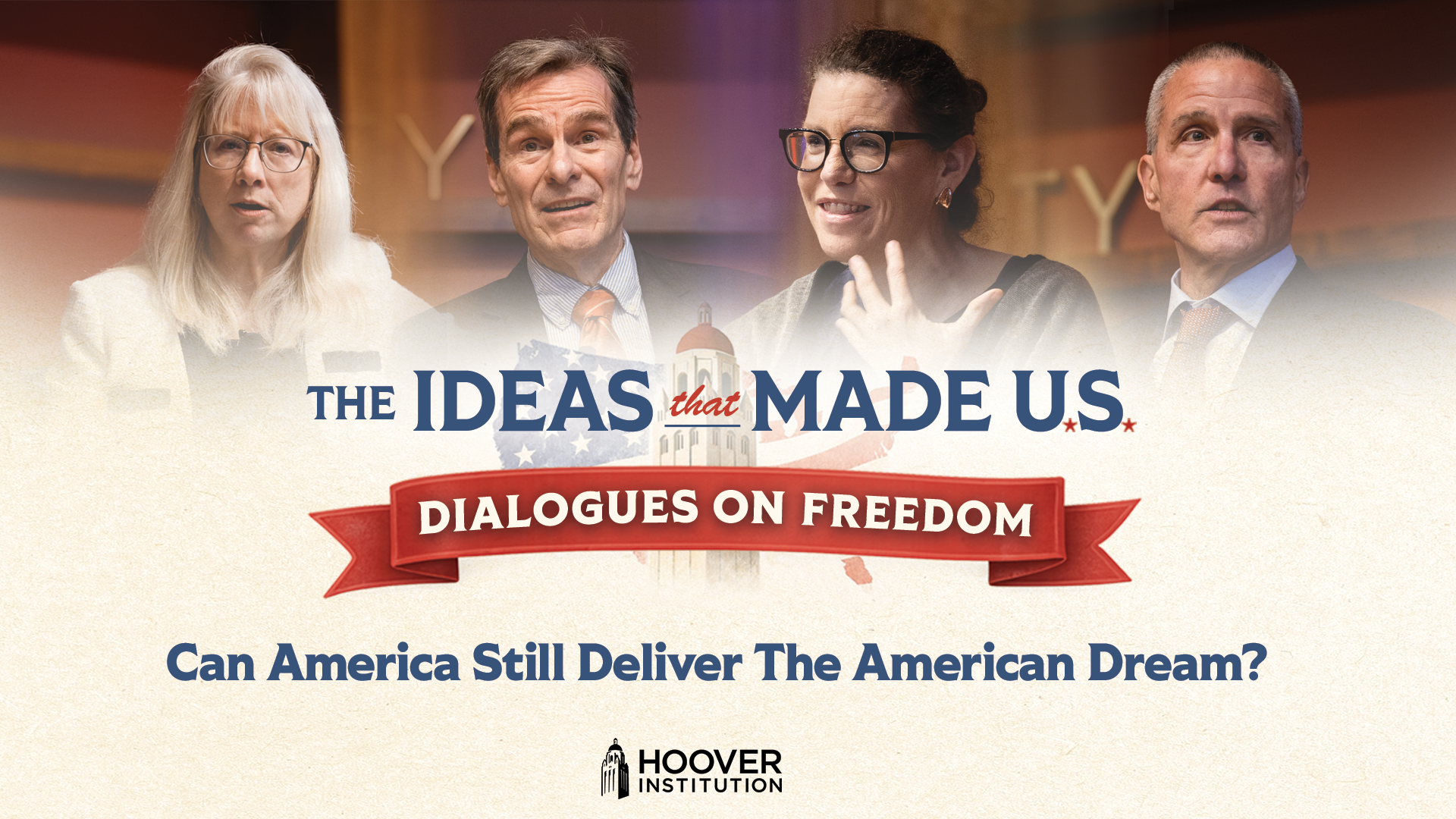

- Good afternoon everyone. I'm Steven Davis, the Thomas w, and Susan B. Ford Senior Fellow and Director of Research at the Hoover Institution. Let me welcome you to the fourth installment of Hoover's year long series marking America's 250th anniversary. We call this series the Ideas that Made us Dialogues on Freedom. For more than a century, the United States has stood as the world's most dynamic economy and most prosperous large country. Today, we will examine what made our success possible and whether the ideas, institutions and culture that powered our success cont continue to expand opportunity in the decades ahead. We live in a time when many feel a wavering confidence in the American dream that raises questions about what it will take to reinvigorate our prosperity opportunity and a renewed sense of economic possibilities. We have just the right folks to tackle those questions, so please welcome them to the stage. Hmm. Seated at the far right is our moderator today, Megan McCardle. She's a columnist for the Washington Post where she writes on economics, finance, public policy, and American life. She has authored The Upside of Down Why Failing Well is the Key to Success, and is known for bringing analytical rigor, intellectual curiosity, and a clear accessible voice to complex policy debates. Seated next to her is John Cochran. He's the Rose Marie and Jack Anderson, senior fellow at the Hoover Institution, and a leading scholar of macroeconomics, monetary policy, asset pricing, and financial markets. He is also a senior fellow at the Stanford Institute for Economic Policy Research, a professor of finance and economics by courtesy at Stanford Graduate School of Business, and author of the Grumpy Economist Pod Substack. Seated next to John is Ross Levine. He's the Booth Durby family, Edward Lazar, senior fellow at the Hoover Institution and Co-director of Hoover's Financial Regulation Working Group, a leading expert on financial regulation, banking, and the relationship between financial systems and economic growth. He is also a research associate at the National Bureau of Economic Research and a founding member of Hoover's program on the foundations of economic prosper. Seated closest to me is Valerie Ramey. She is the Thomas Sowell Senior fellow at the Hoover Institution and one of the nation's leading macro economists. Her research focuses on the effects of monetary and fiscal policy, and she currently serves as chair of the National Bureau of Economic Research, a business cycle dating committee, and as a member of the Congressional Budget Offices panel of economic advisors, over to the panel.

- Thank you. America is the biggest rich country and the richest big country, and we have occupied that space for more than a century now. So what are the roots of that exception? Is it size freedom institutions, land risk taking tolerance for failure, both in the sense of being willing to take risks and being willing to tolerate unequal outcomes, federalism our, our C Credle identity and our ability to assimilate immigrants? Or is it just luck or maybe all of the above?

- John, I'm gonna start with you.

- Oh,

- All of the above. And a certain amount of not shooting ourselves in the foot, which a lot of Europe seems to be busy doing these days, but I, I wanna slightly change the question if you

- Alright,

- Because I love editing. Being better than everybody else isn't as important in the long run as being great, as being prosperous. And when you look at the world of our founders, America was astonishingly poor compared to today's in numbers maybe a thousand dollars per capita GDP, now it's $80,000, you know, people's infant mortality, poverty. We have grown spectacular, and I think if the founding fathers were to come back, they would say that we had no idea this would happen. So I think the institutions that propelled us to growth, to the leadership of the grow growing world are the most important. And, and the worry is of course that that growth is slowing down. So a quick kind of do a little economics. Absolutely,

- Absolutely. We love economics here.

- Where does growth come from? There's two kinds of growth. There's frontier growth, which is new ideas, new technologies embodied in new businesses, and then there's catch up, which means greater efficiency in the end. It has to be those new ideas which, and that that's where America innovated more than any of us. That's why we grew and the Romans didn't grow, even though they had a big free trade area. We were able to let people be innovative and there I think in fact not policies but limited government, secure property rights, knowing that if you invested in a business it wouldn't get instantly taxed away. Orated. That was key. Now, other places had that the UK had in the industrial revolution and we passed them I think when they turned war to socialism than we did. So that's the wonderful news. The bad news is our entire professional lives growth has been slowing down. Ideas have been come, been harder and harder to get. And I think we all worry about whether that process is, is is slowing down, is the problem that we're out of ideas and AI is gonna come rescue us? Or is the problem that you just can't get the permits? And we've tied ourselves in red tape. I sort of think I'm on this side of we have ideas, but we can't get the permits. But I think that for the future is the important issue. Will we create our own stagnation? The way Europe has created its stagnation, but I think we also overemphasize the innovation part. India's GDP per capita is about 6,000. Ours is about 80,000. India doesn't need to innovate. It needs to only be as dysfunctional as the US to have an enormous amount of growth. And I think if you look around, there's plenty of dysfunction in the us something almost equivalent. I think a doubling or tripling of our, our current prosperity is possible if we would just catch up to our own possibilities. And also there's too much focus I think among economists, and you guys can disagree with me on innovation led by government programs. We didn't have any government programs for innovation in the 19th century. Innovation is not just inventing a new chip. Innovation is inventing a better way to get people on airplanes faster. That's how the airlines got much. They, they factor of two or three efficiency just in operational efficiencies. You know, Henry Ford figured out how to make cars better, that those kinds of process innovations are, Elon Musk didn't invent the rocket ship. He invented how to do it 10 times cheaper than everybody else. That kind of process innovation is, is in is incredibly important. So I think those are the challenges and to the, you know, why are we so much better than everyone? Now I'll finally shut up after I answer your question. Sort of limited government, a large market, property rights, rule of law, those are all incredibly important and once I mention them slightly in danger in, in in the us Okay, I, you guys

- Like to

- Hear your, you'll actually answer the

- Question.

- So

- Three things. One, competition, two justice, three stability. And rather than go for statistics, I'm gonna talk about my former neighbor, my summer home in Maine. So Sam graduated from high school and what he did was he finished wood floors and he worked for someone for about 10 years and we would talk about life over beers on his porch and during his work he had a better idea for how to install the floors.

- Okay.

- So Sam was able to go to some friends, including me, get a little money. He had a good reputation in the community. He got some funds from a bank and he was able to compete, okay. He did not have to serve a long apprenticeship or put down $50,000 in order to, you know, break into this occupation. He was able to compete, he was able to try to persuade people that he had a better product and then he could go out because of the judicial system. He could hire contract workers, he could get supplies and he could pursue his entrepreneurial ambitions. And he did this in the context of a reasonably stable economic environment, not everywhere and always, but usually so that when people came in for their summer homes in the spring and they were writing contracts for him to finish their floors and the fall, there was great confidence that there was not gonna be so much inflation over those six months so he could write his contracts. So he was able to operate. And what happened, what happened was Bar Harbor got better floors and take into a big scale. It's what has helped steer economic and propel economic prosperity in the us. So as we talk, I'm gonna keep coming back to those, those three themes.

- I love this idea of process instead of, you know, technology, I always say like container shipping magical, but the idea of putting things in a box was not a revolutionary idea that no one had ever thought before, but they figured out how to do it better. Valerie, what's your, yeah, what are your thoughts on that?

- So, so I think it's some of all of the above things that you listed, lemme just highlight a few. There was luck in that the US was breaking into independence just at the time of the Scottish Enlightenment. And you know, Adam Smith's welcome Nations came out in 1776 as well. And I think that those sorts of ideas had a very important impact on the US and just gave it a great start. But it, you know, what was written in the Constitution, it wasn't enough in that it, you know, and a counter example is that Liberia modeled its constitution after the us but it didn't work so well there. So, you know, something that Tocqueville said during his journeys around the US is that he thought there were three important things, and I agree with him. And in increasing order of importance, he had geography, you know, the amount of land, but also distance from all that European kind of, you know, tradition bound sort of thinking. The second one, let me remember, the second one was laws, of course of the constitution. But the third, and he thought this was the most important, was the morays. And he really emphasized how important literacy was. And I started looking up some of the research on this. They didn't do surveys back then, but by the best estimates, which is if somebody could sign their name. Since people learned to read before they learned to write that the white male literacy rate knew England in 1790s was 85 to 90% by that estimate. It was somewhat lower in some of the other parts of the country, but still just much higher than Europe. And the press was just vibrant. There were newspapers, people read newspapers, they were informed about the government. And so that led to this initial culture that really solidified these aspirations written in the Constitution, into the culture of the country in terms of how we conducted business and all of those sorts of things. Then what was really good was all the immigrants, all right, because immigrants self-select. So who's willing to take risks and go across the Atlantic Ocean to, you know, at that time to go to a completely new land, people who are willing to take risks. So that led us to a nation of risk takers. And often with risk, there is a lot of return on average, also immigrants, you know, they tended to go to the most dynamic places. So it turns out that e back then continuing into the present time, immigrants have more upward mobility than native born Americans. And, and some res research over the last decade or so by Ron Abramsky over in Econ and Leah Busan has, has linked people through censuses. And so it's still continuing to this day that the immigrants are the ones who bring more innovation and who have more social mobility than the Native Americans. So that led us to have a very dynamic economy.

- I had a couple thoughts.

- Yeah, absolutely.

- I'm just riffing on my colleagues here. Some of the essential features of what makes America great, I would say competition, not so much because there's a government agency that in that puts in competition, there's largely a failure. But you're right, you're right to disrupt existing businesses. New innovations are always very disruptive. And let's take groceries. There used to be grocery stores, then the a and p came in and basically put out of business all the mom and pop grocery stores, big social upheaval, but cheaper stuff for us. Then Walmart came in and put a and p outta business, big social upheaval, lots of people lost money. Then Amazon came in and, and you know, that's challenging, challenging. Walmart, the one you're all familiar with, Uber came in and undermined the taxi monopoly. And I think that's a good one to re to remind ourselves the function of in most of these cases is to retard growth. Governments when given the chance to do it, will try to protect incumbents, make life easy, don't let people come in into new businesses. And it is limited government that really preserves that ability to have disruptive competition. Another way of putting it, we are our, our government of rights, not of permissions. Why do we have fracking? And Europe doesn't because you have the right to do it. If you, you own the subsoil rights and, and there's limited amounts of permits you have to get in Europe, you have to ask permission before you do anything and, and nothing happens. So it is really the limits on our government that have provided that, that ability for people to do innovative and disruptive things.

- Valerie, you and John have queued up my next question beautifully. As we, you just mentioned The Wealth of Nations was published in 1776, the same year that Thomas Jefferson wrote the Declaration of Independence. Coincidence? I think not. And so question Adam Smith and the founding father is Walk into a Walmart.

- This

- Is not the start of a joke. What would they, what would they be impressed by? What would they think? This is what I was working towards and what would horrify them about that Walmart, if anything, it would just be an alloyed glee.

- I think they would just be mostly impressed with it. I still remember a story from the Soviet days when a Soviet visitor was over in the US So this was, you know, the seventies and they were showing them all of the monuments in Washington DC and the Soviet person just wasn't impressed. They had the Kremlin and all kinds of things and you know, went and then they happened to take them in a grocery store and the person for the Soviet Union just started crying. They could not believe the abundance. And I think that that's what they would feel.

- Gorbachev I think said that that was when he knew it was over. When he first saw an American grocery store.

- An American

- Grocery, yeah. Probably wasn't even a super Walmart.

- Right? I I think the, the variety, the variety that capitalism gives you is, is astounding. And for example, we have tried to re rehab a house and, and my wife said, okay, let's look at the kid at the, at the light fixtures. Why does the free market supply 10,000 different kinds of light fixtures? You know, the Soviet Union, they had it right number one, two, and three, except none of them were, were any good. And of course the quality and freshness of the food available. I think the founding fathers would be astounded. 'cause they would go in, in January and you would see fresh blueberries and fresh strawberries. Where the heck are these coming from? And then they'd look at the prices and, and, you know, getting enough to eat was a real problem for Americans at the time. And if you compute the prices in terms of

- You first have to explain to them what the relative wage was. Now, otherwise they might be a little horrified.

- Well, they would be horrified at what a dollar is worth. Now inflation.

- Yeah, that's true. That's a

- But I want, I just want to 'cause you put the, the Adam Smith together with the founding of America, and I think that's a very important conjunction. Adam Smith's crucial observation was the invisible hand that markets take imperfect people who, who you don't count on the benevolence of the butcher, the, and the brewer. You count on their self-interest, a set of rules of the game that guides people pursuing their own selfish self-interest to, to do good for their, for their fellow human beings peacefully. That is also the central idea of the founding of America. We do not try to make better people, the Soviet man. We don't hector people just to, to behave better. We have a system of checks and balances beautifully worked out so that selfish venal, imperfect people cooperate together and peacefully. Ours is the only ism that's fundamentally founded on peaceful interaction, not violent exp appropriation. And that's, that's something of both of those visions to be celebrated.

- Ross, you you look like you have thoughts. Sorry, Ross. Yes, I think,

- I think that Smith, I I I, I don't disagree with what John and Valerie said about Smith, but Smith was much broader and had a much more nuanced view of his human nature and people getting together. So first of all, when Smith spoke, and he wrote again and again and again about this, that competition, the potential restrictions on competition came from the markets. It came from powerful people in the markets trying to use government to restrict entry and to be coercive. So to only categorize it as the evil government misses really Smith's Smith's insight into why you needed competition. That you needed competition in order to stop that co-mingling of powerful private interests and the government that would work against the public at large. The second thing that NF spoke about, and he called this the most fundamental element in his entire structure, was justice. You needed the rule of law so that people would view the system as legitimate. And without that legitimacy, people would not buy into this system. You would not have peace, you would have violence. And so the notion of justice cuts through his first book and the one that he favored, the Theory of Moral Sentiments and the Wealth of Nations. And so that is, those are also themes that echo through the Declaration of Independence and the Constitution. It is a very sophisticated view of what people want and how you create a society that, you know, to go from the declaration allows them to pursue happiness. It doesn't guarantee happiness, as you know, John has mentioned in different words, but it's the same concept. It was a guarantee of a pursuit of happiness. It was a guarantee of liberty. Although that's a complicated concept also. But that was, that was the promise. Go for it. And as you emphasize in your book, if it doesn't work out, pick yourself up and go for it again. C can I

- Ask Ross a question? Yeah.

- On that topic, because

- Ro

- Freeform Jazz Odyssey

- Ross is writing a lot about Adam Smith and you've read more of it more recently than I have. And and so you brought up a fascinating issue that to some extent business people try to conspire to monopolize things, but that usually gets undercut quickly. True monopolies are granted from the government, and so they run to the government for help. Yep. And I, so there is a tendency, I, I wrote, I noticed this in my own sort of free market group. We tend to bemoan how stupid policies are, oh, it's just as dumb, but it's dumb and dumb and dumb and it sits there for years. So why is it happening? And there seems to be a problem. We have a very responsive democracy. You want a democracy to respond to the needs of its citizens. They can know the right to petition the government. So, you know, economics, professors are under, under siege because there's all these foreigners coming in and, and you know, competing away our salaries. So what do we do? We run to the government and say, you gotta stop this ter it's ruining our business. We're gonna have to fire our secretaries. You need to give us some protection. And of course, a responsive government says, sure, of course we'll help you out. And that is how the government responds to people's desires for protection. But that just undermines growth. That's what happened with the taxi. It's not evil, it's not conspiratorial. It is actually, it's, it's, it's an undesired side effect of the feature of being responsive. And I don't know how to fix this.

- So are you asking me or Adam Smith?

- Well, - I I'll tell Adam Smith is smarter than you. I don't know if there's no question, so either, so let me start, let me start by telling you though, what, when you hit on is why I am so angry with Adam Smith. Okay? So he gave us the Theory of Moral Sentiments, which is a story or it, it is an, an evaluation of what makes us happy, what motivates us, what ultimately gives us fulfillment in life for economists, it's about the utility function. Then he gives us the wealth of nations, which is in many sense a positive book about how do people interact in a society, how do we organize that in a peaceful way? And it's also has these very clear policy prescriptions about justice, about competition and, and about stability, talks about fiscal policy, all of the rest, his third book. And he promised us this third book, starting with the Theory of Moral sentiments, was going to be about jurisprudence, which many people view as how are we gonna govern ourselves so that we choose good policies. And what happens is he's towards the end of his life and after he finishes the wealthy nations, he takes on the job of customs official. So here is this guy whose major work was to tear down the view of mercantilism and trade, and he come, becomes in charge of enforcing those tariffs at the custom houses. More importantly than that, he didn't write the third book, which is the answer to John's question.

- Tariffs make everything worse.

- Yes, this is, but I think I, I think to give a one potential answer is we are people, we are humans, and there are a variety of complexities. And we go to the government and we ask for the government to solve certain problems. We as people respond very quickly, as you can tell from social media to anger to stories. We want a clear villain, we want a clear victim, and we want an even clearer answer that it's gonna provide immediate relief That's not reality. Throughout human history, we created a variety of frictions that slow our thinking down. Okay? And this comes from behavioral economics. This is not my idea, of course. For example, you can have staggered elections, you can have required, you know, cost benefit analyses. You can have some of the recommendations that various regulations should go away and only have to be, you know, put back into place. All of this is to foster deliberation. What has happened in, since the mid 1970s or so, is technology speeds everything up and we're slow, but we'll get there to put in place a variety of frictions to get us to slow down. And I think that that's wolf progress.

- Well, that's, you guys are just basically asking my questions for me. So I don't know what I'm doing up here, but, so I think that the question, yeah, I think Milton Friedman said that the mystery is not why people are rich. It's like because why people are poor, because the, the, the normal human condition is poor. The question is why they're rich. And the question is, how did we avoid some of these? How did we manage to not have all of these, you know, cartels and so forth colluding against growth. There have been, we have had those episodes in our, our history, but remarkably few compared to Europe or other countries. And have we lost our mojo? Have we now got have, have the institutions become too sclerotic, the interest groups too well entrenched, are people too well settled and prosperous and just, we just wanna sit home and, and watch our huge screen televisions all day and have we sort of lost our edge? Or do we have another American century ahead of us?

- Right?

- We've been blabbing away blabbing too much. So you go first. I

- Think we have another American century ahead of us. I think that just as technology comes, so, so work that I've done before talks about how we have technological laws and then suddenly there's a shakeup, a technological revolution, and then that can take several decades to play out. I think we also see that in political thinking. And let me just give you an example. If you look at the start of the 19 seven, first half of the 1970s, there were so many regulations on trucking that truckers were only allowed to carry cargo one way and had to come back empty. All right, I be, and there, and that was just one example of what was happening with trucking. Also, there was the idea that, you know, every little city had to be served by an airline and you couldn't possibly have competition in airlines because things would not work. And then of course, if gasoline prices go up because of opec, you have to put on price controls and all of those things. Well, something amazing happened in the second half of the seventies. Usually one doesn't think so positively about the seventies, but the Ford administration and the Carter administration, Ford started it. And then it happened during the Carter administration, I believe it was in 1978, we had airline deregulation. Now anybody remembers that period. Remember it was pretty chaotic after, after, during that period with the big shakeup airlines coming in, going out. But look at what we have now, just much lower fares, really efficient airlines because this idea of deregulation bubbled up even though there were so many vested interests. And so this is something where we should case studies to say, how did we manage to do that? Also, I think his first day in office, Reagan signed something to get rid of all price controls on gasoline and oil. There hasn't been a line at a gas station since we figured out that letting the price go up gives the right signal that people should carpool while prices are up and do anything they can. And so we do learn, but it's often in these kinds of things. The other thing is with the tax system. So we start with the tax system and they start adding on this and that, and then the rates go up. And from an economic point of view, you want the broadest possible base and low rates because that, that raises tax revenue the most efficiently. But instead you start getting all these other things and then suddenly have something amazing like the 1986 tax reform where they just clear out all of that brush and then start up again with a much better system. So I still have, you know, optimism that we can do that, but sometimes things have to get worse before they get better. And it's been that like that a lot in the us. I was just started reading a book about all of the move to nationalized industry, all the defense industries after, during World War I and after, because they thought that private sector should not make any profits off of defense. And you can see that they changed their mind after World War ii. So those are examples.

- Oh, I, I am very optimistic about the, the US over the next century. So I think a lot of the challenges that we're facing now really come from our success that starting in the mid 1970s, there's lots and lots of technological innovation. There was automation, you know, with computers, information technology. Now there's ai. This has caused this a serious disruption in labor markets. It's caused some people, some families, some groups that have extraordinary opportunities and it's caused many people to be fearful. This is not a story where there's some evil person out there or there, there there's not a villain. This is a story where our success has caused disruptions, it's caused a lot of fear and it's caused some disillusionment. This has induced us to make some bad policy choices because politicians give us a villain. Oh, it's the foreigners. Oh, it's the immigrants. Oh, it's the elite. Oh, it's the billionaires. And, and we'll get over it eventually and come back to what are the ways in which we can foster competition, have a just society, keep economic stability. Fiscal policy is gonna obviously need serious adjustments along, along that front and, and do that while accounting for the real uncertainties and fears that people have. Why am I so confident? I, I'm confident because since we have data, reasonable data at the end of the Civil War, the US over long period of time has grown at about 2% per year in real per person terms.

- Hey,

- It's, we, we, not every single year, but if you look over a few decades, it's about 2% per year. Over that time period, we had no federal income tax over that time period. We had a marginal tax rate of 90% over that time period. We had women enter the labor force like never before. Over that time period we had high tariffs and low tariffs, okay? We had many individual policy changes, but eventually the US has come back to expanding opportunities and, and, and prosperity. And that's comes back to those three elements.

- So I wanna be a little

- Go

- Somebody, somebody has to be the Debbie Downer here and that's gonna be my job.

- You're the grumpy economist.

- How the grumpy economist. I think there's a real danger. Now the US has always cycled between periods of stagnation and then periods of reform. But the last 1980 was a while ago. Seems like yesterday to us, but, but it was a while ago. And the 1990s, there were some really serious reforms then as well. The number of unaddressed dumpster fires is, is increasing and the ability of our political system to handle sort of basic things seems to be, seems to be decreasing. I I just, I made a little list of dumpster fires here that desperately need reform education. K 12 education, especially in the cities, especially offered to poor people is, is a disaster in the hands of teachers unions. We can't seem to fix that. Permitting is a try rehabbing a house in Palo Alto. Good luck. And that, that part of that is also the disaster of our public investments to where California high speed train, I guess that was more than two words, you know, $200 billion just down a rat hole, not a single mile of track late rebuilding houses in LA after the fires. You know, they just can't get, get the permits. I'm, I'm hopeful on all of these. There are voices saying reform housing in California. Progressive democrats have, have actually said, oh maybe yes in my backyard, but they're having a trouble getting there. Our tax system has, is on a long way since 1986. We are pretty much having the minimal revenue at the maximum distortion rather than the other way around how to reform. It's perfectly obvious, getting around to doing it is not immigration. Another, another dumpster fire. We all know how to fix it. But getting around, you know, the bipartisan thing can never get done are social programs from zero to $60,000 in the US you earn an extra buck, they take away a dollar worth of benefits. Guess what happens there to say nothing of the amount that just goes into the pockets of n NGOs. California spends like $85,000 per homeless person. And what do you get? More homeless people. Financial, and, and a lot of this is reflecting the, the, we you used to be faith in elite institutions. And it's not that we lost faith, it's that they proved themselves completely incompetent. You know, the financial crisis I think was a wake up call to, to many people public health who trusts the FDA and the CDC after, you know, COVID when they told us two year olds had to wear masks to play outside. You gotta be kidding. These videos of people putting masks on screaming two year olds just is perfectly, perfectly obvious. And our inability once we start something to ever clean it up, farm subsidies, we're still subsidizing farmers. It's not 1933 anymore. Corn, ethanol, Trump administration just went back for more corn. Ethanol is completely useless policy for climate for anything else but subsidizing farmers so that we live always on this tension of it's going to hell and, and then we get it fixed. And the optimistic thing is there's a lot of volatility to American politics. You may not like, you know, the shift to Trump, but boy oh boy, did it reflect a, just a basics of the median Americans saying, I've had it with you guys. The we vote against presidents, we don't vote for new ones and, and we'll vote against this one soon enough as well. But the ability to shift and get back to common sense, I think is, is hopeful. But there's a long list of of things that need to get fixed and, but you know, said deliberative and so forth, it, it comes back to a functional Congress is necessary for our government to go forward. And I don't see so, so I keep hoping for reform before the deluge happens. But you know, some societies don't do it. The UK slid and keeps sliding and has not been able to get its, its act together. Maybe America's exceptional in that we're exceptionally chaotic when we're bad, but then exceptionally able to move when we finally get around to it. But, but

- Farm subsidies are a good example of of, I've been waiting for, I still remember reading PS Problem of horrors in 1990. A masterpiece too. A masterpiece. And I actually remember one of his lines about like the US honey program that we all remember when the US economy was brought to its knees by wild swings in the price of a and that's why we needed to stabilize it Jones

- Act.

- Could we

- Possibly get rid of the Jones Act?

- So I, I wanna come back to this fiscal question. I it's really important. But before that I want, I wanna ask about opportunity and mobility, whether or not we are going to have another American century. I think a lot of people don't feel like we are, they don't feel like the American dream defined as opportunity and the ability to have a good life. If you work hard and play by the roles, they don't feel like that's available anymore. And I think, you know, the abundance critique has come up of there's all these barriers to doing that, that are created by exactly these kinds of sclerotic, outdated regulations and special interests that prop them up. If you had to pick one between housing finance or education or something else, I haven't mentioned, what, what's the biggest barrier to realizing the American dream for normal people today? Valerie

- Education. So the, the K through 12 education just does not produce value. I, if you come from a household with educated parents, you can get by, but if you don't, there the, the, the gap between how you achieve and the kid from the educated household just grows with every grade. I, I've looked at this over time and it really matters. So I've looked at this across ethnic groups. So the Asian kids in the California public schools K through 12, the test score gap between them and the white kids is almost as big as between the white kids and other minorities. And so something that's going on in the house is making up for the lack of things going on in school. But if you don't have that education, then you lose the race between education and technology. So this is an idea in economics. Claudia Golden and Larry Katz wrote a book on it about 15 years ago that as technology moves ahead, you ha education has to move ahead to catch up so that you have workers who can implement the technology and understand it, but also, you know, innovate. So there was a big movement in the US in the 1920s. We were ahead of the rest of the world in terms of the years of education because we had the high school movement. And a big force leading to that was businesses who wanted educated workers because they knew that with that new technology we were having electrification, chemicals and all those things, they wanted workers who could come out of high school and understand a blueprint. And I, you just don't get that anymore. Unfortunately at over the 20th century, there was an increase in the demand for specialization. So it used to be that our colleges and universities educated people in the liberal arts but didn't specialize. But over time they saw there was a demand. So you started having engineering schools and business schools and all those things in colleges at the same time. After, you know, this is in the, basically starting in the seventies, high schools suddenly decided, well they should just prepare everybody for college. So they got rid of vocational training. And so there were a lot of people who just for whom college just wasn't a good option, who suddenly got out of high school without any usable skills to speak of. So, so they were let down by this move away from vocational training. Meanwhile Germany has kept up the vocational training and just done a much better job educating their workforce. So that's something that, you know, there are some movements now back to allowing a vocational track and the more general track to go to college. And I think that's just first order because without the education and not, you know, the skills, but also I should say civic education, I don't think that people understand why this country is so much more prosperous and successful because they've just deluded what most of us were probably taught when we were in school. So I would add that,

- Yeah, I think I wanna bridge two things. So I agree completely with Valerie and I'm just gonna pick up where she left off. And that if you have much better education, then you have many more people who see those opportunities and can take advantage of them. And so they're therefore not looking for protection from the government, all a whole assortment of regulations. They are looking for the ability to pursue happiness, to pursue their, their whatever goals that they have. And so with education will come a change in the population in terms of what they demand, which will lead to different leaders because they will want to give, respond to that.

- So let me, I'll try to be a little bit contrary. It's, it's boring if we just agree with each other all the time. I, first of all, I wanna salute that you're asking the right question 'cause there's a lot of inequality is terrible and somehow if we get rid of the billionaires, everyone will be fine. Well, the kid pumping gas in Fresno, whether billionaires fly private or, or, or not makes no difference. Stays like the problem is opportunity on on the, on the bottom end of American society. But that maybe the cheerful one now the charter school and voucher movement is happening and there are opportunities there even in the poorest communities in the US and, and they are inexorably spreading. Now this is, you know, reform happened slowly. Milton Friedman had this idea in about 1956 and slowly but surely, here we go. But this is clear to everyone, it's a problem. And that is the way opportunity's there. And I'll say more generally, America remains an open, the opportunities are there, the, the narrative that it's impossible anymore to get ahead, that it's worse than it was in the 1960s. I, I think is false. You, you, the the these path to middle class life finish high school, even a rotten high school, get a job, get married, have children, stay married in that order, produces still a middle class life in America. Even with all the difficulties. Too many people fall off of that. And I think, you know, some of the seductions of our social programs trap them. You know, if you, if you, if you have a benefit that gets taken away, if you get a better job, well of course you don't get a better job. I'm a little nervous about saying, you know, a federal program of vocational education or a top down answer is the right one or job retraining because it was only like three years ago that the answer is we'll take all the steelworkers and teach them to code. Oh whoop, sorry, AI came along. That was a bad idea. So the, so you know, lots of different opportunities and and supply side reforms rather than some, some new big program I think is the answer. But I also wanna, again, object slightly to the question. If you could do one thing

- The pro, I didn't say if you could do one thing, but what's the biggest one? What biggest just the, what's the biggest,

- But well then I'm gonna respond to the, if you could do one thing, probably not.

- Because - The nature of America's problems right now, it's, i I call it we need to a Marie Kondo cleaning up of the insane complexity of our public life. We don't need, as opposed to we're all macro economists, the seduction of stimulus, we'll just hand out checks and everything will be fine. That's so simple. But as you remember, Marie Kondo is how to clean up your house. And it goes, first we do the sock drawer, then we do the underwear drawer, then we go through the kitchen cabinets and finally, oh God, here comes the garage. It's step by step and you gotta clean each one and every, every part of our, of the things that are screwed up or screwed up in their own complicated ways. So the one thing is a large scale reform program, but that means you gotta fix everything.

- So I wanna talk about fiscal policy because our, our, our government has been spending like a drunken sailor on shore leave with a terminal disease and our and a credit card. And a credit card and, and his father's credit card. I think I've pushed this metaphor as far as it can go. So you know, debt is now a hundred percent of GDP and that leaves us, our budget deficit is six 7%, which is just ridiculous in in peace time. Does that leave us less room than we had? I look back in 1976, they made a lot of mistakes, right? The inflation, bad fed share, bad, lots of things bad, but they didn't have this problem and this problem seems like it makes everything worse. Is there a way out of that short of having a fiscal crisis

- Wants to go first? I'll go first. So there's, we're going to get out of this. It can happen in a couple of ways.

- Yes. Do we, do we go out in a body bag bag or do we go out and right now on our own feet with our head held high

- Right now we have bipartisan support for the worst way out is that we're gonna have high deficits growing debt and it's some point something is going to trigger a reaction in the bond market and we're gonna get soaring interest rates and we are going to be in a lot of trouble. And it, it was really remarkable last year when the head of the house and the head of the Senate, both of whom and the course of their careers had called the deficit immoral past the fiscal policy that increased the deficit. And as I wrote it actually in the Washington Post where have all the conservatives gone,

- Fine choice of outlet and fine point.

- And so that's the, this is the issue, you know, are we going to be able to address this? And I'll again go back to Smith. There's another way to address this. And that's gradually incredibly and Smith the great proponent of, you know, the invisible hand in markets and even he, when he talked about the deficit, looked to somebody who he admired a little bit older David Yung who talked about the long history that he had studied about the problems of fiscal debts. So there's nothing new here, but what he talked about is approaching this gradually. This is anything that starts with we just have to, is not going to work. It's going to have to be an adjustment of spending over time, including entitlement programs. And it is very unlikely to come from raising taxes because taxes are already high. And that is a clear way to stymie growth and innovation in the opportunity that we've spoken about. But it's gonna be, it's going to require bipartisan support where right now there's bipartisan support for the opposite. So you're the expert on fiscal policy. So yeah,

- So usually when I speak I am very pessimistic because I speak about the issue of debt and deficits. Alright? So it's unbelievable. I I've been talking about this for many years and it looked bad at 70% and then it went up to 80% and then 90% and a hundred. And I just cannot believe that we are at, almost at the same level as at the end of World War ii, that countries that do this, world powers, that do this, like the Netherlands white centuries ago and Great Britain that ran into these problems, they lost their hegemony in the world because of their fiscal situation. So, so there is a lot to lose from this. I agree. Well when you, when we say let's just, well one thing, let's, let's just get serious and start talking about this and start talking about it publicly. The, the problem is that, that the public doesn't seem to register this. They know that there's a problem, but they don't understand you. You know, when you talk trillions of dollars, they don't understand what that is. So sometimes I'll give numbers, like currently the level of the debt is $89,000 per person, including women and children. So that's a lot. Alright? And, and that's how much a baby's born. That's how much you could say, you know, they owe when they're born. And it's, I i I wrote something for the Wall Street Journal in 2019 about how a prudent government runs surpluses during good times. 'cause 2019 was a good time. 'cause you don't know what's around the corner. Well, you know, that was a little bit presion. I had no idea it would be a pandemic, you know, which we hadn't had in a hundred years. But, but now with the defense buildup, we are so much weaker because what we did with the deficits, so 23%, so debt to GDP ratio is currently a hundred percent, 23% of that is all of those key and stimulus payments during the Great recession and during COVID. And my research shows that there was very little macro stimulus from those payments. So 23% of that otherwise, you know, we would be down at, at a nice 77% without all of those payments.

- I think just to add on is just to broaden it, is that when you look at the unfunded liabilities like Medicare and social security, I think you're talking about 78 trillion or something that makes the debt about three times bigger. And so it's even, it's much worse than after World War ii. Yes. Because of those unfunded liabilities and because of the, the demographics,

- Right? Yeah. So, so yeah, two things. The latest CBO estimate is that by 2056 we will be at 175% debt to GDP ratio. Something also to keep in mind is how did we go from 107% debt to GDP ratio at the end of World War ii down to 23% in the 1970s. So people like Paul Kru and said, oh, we grew our way out. Turns out that's not, there was a little bit of that, but that wasn't most of it. So first of all, I calculated something for Brookings in the first three years after the end of the war, prices went up almost 30%. When prices go up, that reduces the debt to GDP ratio because, because the debt is in nominal terms and it doesn't go up. But then GDP and prices go up. So almost 30% was eliminated in three years. So think of all the people who bought those war bonds for patriotism. They had huge losses on those. And what and why didn't interest rates go up? 'cause usually when inflation goes up, you have inflationary expectations and interest rates should go up. Well, it's something called financial repression. The treasury put pressure on the Federal Reserve to keep interest rates close to 0% to help finance the debt. This continued on even though the, the Federal Reserve got, its in more independence in 1951, the government kept surprising people with inflation so that real interest rates were often negative. So you, so if you lent money to somebody, what you got back was actually less in terms of goods. That was great. If you taken out a mortgage in the 1950s, you know, you, they were basically paying you to do it. But it really led to misallocation of all the funds in our financial system. And so financial repression is one of the worst things you can do to an economy. In fact, the the person who coined that was Ron McKinnon here at Stanford. And he said, you know, South Korea was very poor after the Korean War and it was only when they lift the financial repression that they took off. And you had the South Korean miracle. The problem is, when you have high debt like this, the government has a big incentive to try to use what we call the inflation tax. And that's to inflate it away.

- John, would you like to bring the optimism or are we get the, are we getting, are we getting the grumpy economists now? So

- I I will close with some optimism. I'll try to say something that you guys haven't said in your, in your great remarks. The problem isn't the debt. The problem is a lack of a plan for repaying the debt. Countries have paid off the UK paid off 140% debt to GDP ratio after the Napoleonic Wars by while inventing the industrial evolution helped, but then by steady small primary surpluses outside of crises and slowly pay them off. We can do that too. We could borrow 150% of GDP if people had some sense that we have a way to pay it back. In fact, our debt was not racked up by, it was primarily racked up as, as Valerie said by two big deficits. One in the financial crisis, one in COVID. I agree most of that money was thrown down rat holes. It was not spent productively. So one of the lessons going forward is in the next crisis could we spend with a little more attention to whether it makes a difference. But the, the plan to pay it back is really the issue. Imagine that we, we just wipe out the debt default, inflate away all the debt today. Well then tomorrow the government goes to bond markets. Oh, by the way, I need to borrow three to 5% of GDP for this year's deficit. And bond markets say, well that's funny. The problem is the lack of a plan to pay it, pay it back. And, and that's really where, where we're in trouble. And that we know where that comes from, comes from. We have a European welfare state and we don't have European middle class taxes to pay for it. And we also are, are throwing money down rat holes. There's about a trillion dollars a year, if not a trillion isn't a lot, a trillion isn't enough money. You know, I'll go back to the California high speed train is emblematic o of our rat holes. So now this could end up very badly and pe I I think you don't realize how badly could end up people sort of say, oh, someday the bond market vigilantes will come. And the three of us have been holding this sign saying the world is ending. The bond market vigilantes are coming for about 25 years now they're still not here. But I think that's not really the worry. Let, let me first scare you and then, and then make you feel better. What happens in the next crisis? Another pandemic maybe had the viruses on its way. China blockades Taiwan, massive financial crisis. World trade falls apart. GDP falls. What does Uncle Sam do? I need to borrow 5 trillion, $10 trillion to bail out all the financial institutions again for stimulus checks, right, left and center. And oh by the way, we kind of neglected the military and we need one right now. What do bond markets say? Wait, you want five to $10 billion of new savings that we are gonna hold as an investment? 'cause you're good for it. Could I see the repayment plan on that one? And by the way, a little apology note that in in COVID era we gave you 5 trillion and you inflated away 20% of it. We took a 20% haircut right away. They may say no. And that, that's that loss of fiscal space to meet the next crisis is I think the worry. Not just that the bond market vigilantes come along. Every crisis needs a spark. We are, we are more fragile than we used to be. Or it could go badly in standard Latin American way. So what happens is governments find it harder and harder to finance deficits well, they start putting in more restrictions back to financial repression force banks to hold government bonds, tell the fit to hold interest rates down, start taxing government debts, very high tax rates on wealth. Take all the billionaires tax and the economy slowly starts faltering. That wouldn't be pleasant either. So, and a big, big bill bout of inflation came along there somewhere now. Huh? How do we get out of this now? Some good news. It would take a committee of the four of us about 10 minutes to solve the problem. We need to close a fiscal gap of maybe 3% of GDP for the next 20, 30 years. We need to bring America back to the fiscal policy we have always had, which is small, steady primary surpluses in good times, and then borrowing to, to meet the events of the bad times. We have no external pressures. We are still, as much as I worry about us slow growth, we're doing better than everyone else. Europe stopped growing. So we just, you know, we have a, the best economy in the world. We don't have external pressures. There's no barbarians invading Rome. You know why in the, if we have a debt crisis of our inability to to, to match spending and transfer payments, that is a self-inflicted wound of first order. And I think the founding fathers and, and, and mothers will come back from their graves to, to to, to lash us with noodles for how could you screw this up? So it, it's on an economic basis, e easy to do and it would be a shame if, if it didn't happen. But it needs not just administration doesn't need budget tricks, doesn't need even the 10 year budget window. It doesn't need austerity, it needs reform, it needs a tax system that raises some revenue without economic distortion. We all know how to do that. Redo 1986, put me in charge. We'll have a pure consumption tax raise a lot of money without a lot of distortions reform. The social programs. We don't need to throw grandma from the train, but you know, we don't have to index to wages. We could index the prices. That would be pretty good. We could cure the massive whole of our, our health insurance. You know, we're promising to pay everything to everybody that, you know, there's 10 easy ways to fix that. But that's, but it, it doesn't help to do, you know, some quick, quick fix. That's both the good news and the bad news. And it has to last through multiple administrations. So it has to be bipartisan because just for the reason that this has gotta last 20, 30 years, and most importantly the bond holders to which to whom we will turn in the next crisis have to have the confidence that yes, America will go back to slowly repaying its debts. They still have that confidence. Why have bond markets not already exploded? Why have we not seen the hyperinflation already? 'cause bond markets look so yeah, Congress, but this is a great country. Sooner or later of course they will get back, we're, this country isn't gonna have a Argentina style prima lay debt crisis. They'll figure out the obvious things that any bipartisan could do before that happens, won't they? Well, well they will, won't they? So that faith is still there, but that faith is more fragile than it used to be.

- So 50 years from now, if America has had a good 50 years, how will historians tell the story of what we did to have those good 50 years? And if it's a bad 50 years, if we don't get it together, how will they tell that story?

- Do you wanna go first? Well, no, I to think up in that story.

- Ross, you you opened your mouth first. Yeah, I did. Okay, so did, so we get to get five

- Minutes to think So I think so. I don't think it's a matter of one policy, just like, I don't think it's a matter of one policy that caused economic growth over a hundred and fifty, two hundred fifty years or is causing our problems now. I think it's going to be that the population stopped enjoying being angry so much. It rejected that as an explanation for all of its problems, both the right and the left. And it got back to, if I can go back to my original story about Sam, he really doesn't want to hear about all of this. He wants problems solved. Anybody that works in a small business knows that you have to compromise that there's workers and suppliers and that's gonna be part of the deal. And so that is going to be the story. It's going to be a political economy story where we got set up and we chose leaders. And leaders gave us a choice of somebody who's going to, for example, on fiscal policy, say, Hey, we're gonna have to make this adjustment over the next decade or over the next year if you're if, if, if John is in charge. And it's gonna involve some costs and some pains, but here's what's gonna happen afterwards. It's gonna involve someone looking at the financial sector, which is really a mess. Now with regulation, I am very fearful that we are headed toward a financial crisis bigger than in 2008. Imagine having a financial crisis that much larger with the, with potential unemployment, with our fiscal situation and with our political economy now telling people that this happened because there was a mismatch of incentives with moral hazards and too big to fail and, and poor regulations isn't gonna cut it. They are going to demand government intervention and finance. And that's going to be so, it's gonna, it's gonna require a leader and it's gonna require us not a leader, it's gonna require us demanding leaders that will solve problems rather than give us these platitudes that make us angry at some make believe villain. So that will be the, that will be the book that will sit in about this period.

- Yeah, you know, I, I do think it's the way if things turn out good or bad, it's gonna be the inner play between the voters and potential leaders. And you know, I still think, you know, I study a lot of history, you know, sort of the great man or woman of history really can ma people can matter. And so particularly politicians who can say, yes, this is gonna be tough in the short run, but we're going to enact reforms that are gonna make us better off later. And, and there are a number of them on both, you know, in both parties. But you know, it's really amazing for example, that Reagan would support Paul Volcker lowering inflation despite the unemployment rate going up to something like 10%. And he said, just hang in there, you know, even though, and I remember those midterm, you know, keep it up and the economy actually recovered from that very deep recession. And it, you know, in war time, you know, FDRI don't agree with all his economic policies, but he was a leader that could get people to do things. And I think that that is just really important. But you need to have a polity that elects leaders. And something that I worry about now, it seems like all of the reasonable people are retiring from politics because it's just so awful in Washington. And so something has to turn around that, because we could go down if we don't do that.

- Yeah, I just, I'm gonna echo what you guys have said, but I think it bears echoing if things turn out well in the next 50 years. The, the precondition for that is a generation of leaders in Congress as well as president, as well as state and local governments, which are even more dysfunctional and need to become more functional of what the American people want, which is people who will just mind the store. And we, we, our our public discourse has been overtaken by these sort of Arian religious quests. You know, first it was overpopulation is gonna starve us all. And then it was the resources all all run out and then nuclear power will poison the earth and then GMO foods are gonna turn us into Franken foods. And then it was the global warming, which became climate crisis, became climate catastrophe. And we need to de industrialize and go back to the farm for that. And now AI is gonna take all the jobs. No, no, no, wait, wait, wait. Just mind the store, fix the, the, the things that are broken in, in American public life and allow that natural progress to occur. You know, take a deep breath, calm down. Reform as, as Valerie said, we've done it before the late 1970s actually had remarkable economic reforms. You, you may, air travel was one of the great ones. You know, you may be, you may be fond of the pictures of 1970s air travel. It's still available. It's called business class. And that's the price that you paid for it back then. And other countries ever, you know, Sweden gave up socialism. They're actually more free market than we are. They still have high taxes. But things like that are possible now, I think part of the problem is in the rules of the game. So it's, it's not, we don't need visionary politicians, but we do need like the, it's just amazing what the founders did in terms of thinking through the rules of the game that would produce better outcomes. And, and let's just, we're supposed to be reflecting on the 250th, especially the constitution. They were a crisis moment. The articles of confederation weren't working at all and they needed to cobble something together that was gonna actually work. And they came up with this beautiful machinery thinking about how all the sorts of events nobody had had thought would happen and just did a beautiful job. Well that machinery I think is at the root of the problem. Just one example, why are we so polarized? Well, two reasons. One is we've turned into a winner. Take all presidency, we rule by executive order. So now there's in some sense too much democracy. You get to win and then shove it down the other guy's throats as opposed to, and then too much power leads to too. It's, you can't, you, you have to afford to lose an election. And primaries, we have maybe too much democracy. Primaries used to be decided by old white men in smoke field rooms and they picked people who would win the general. Now primaries are democratic, which means they're picked by the extremes. This is just two examples of how the rules of our game are not working. Now how do you fix the rules? It's hard. And, and, but the art of reform, I think the 1986 tax reform is a good example. It's not necessarily painful. 1986, we reduced the top marginal tax rate from 70% to 28% and closed so many loopholes that they made more money on it when they were done. How did they do that? Well, it wasn't as perfect and it doesn't make it sound, but here's the art of leadership. The art of leadership is Ross, you're gonna le lose the tax deduction for re for beautiful purple ties, Valerie, sorry that that white jacket tax deduction that's going Megan, you know, nope, the, the, the gold earrings tax special credit is gonna go, but you're all gonna make it up on, on the volume. We'll lose a little on each item. You make it up on the volume. And in doing so, I want you all to be allies with me, Megan, you're gonna vote with me to get rid of their tax deduction as opposed to come get mine. So, you know, that's the, you do need leadership and I think leadership can, can do that. But that's what it takes. And, and I hope 50 years from now they say, oh, America went on. It's just calm down with the crises. Let's mine the store. Let's fix the machinery of government. And then the news will not be the government. The news will be the ai, the news will be the great innovations, the great new companies, the unleashing of prosperity. And no one will really pay attention as you know, we look at the 1920s and nobody thinks about Calvin Coolidge, but he actually was there as, as part of what allowed that great increase in, in prosperity to happen. But that can also get, get killed. Remember nuclear power, nuclear power. We could have cheap carbon free electricity right now except we put it on hold for 50 years. Genetically modified foods. Most of Europe has put that on hold for 50 years with actually fairly bad bad effects around. So it is entirely possible to kill this goose kill, kill the goose who lives, who lays the golden eggs. But if we don't, then what they'll remember is, is the wonderful prosperity and all this politics will be forgotten.

- Alright, this is a final question. This lightning round I am pulling

- For us that's really important.

- Well, I I, you get a, you get a, you get a one word answer. I am pulling 10% of your net worth. And I'm gonna ask you to bet whether by the next, not the semi quincentennial, but whatever the, the t centennial, I guess it will be by, by or tricentennial is America, has America pulled out of its current be grs or did it go in the wrong direction? You or which way do you wanna bet? You can bet in either direction, but you gotta put, you gotta put 10% of your net net worth down, Valerie, which way do you bet? Up or down, up,

- Up, up. And I've put in more than 10% now 'cause I hold the stock market.

- And that is a great answer to close with. Okay, we're gonna take some questions. I'm gonna take a few at a time and then we'll, we'll ask the panel to answer them. We have Mike circulating hands up you sir. And a few more people can keep their hands up. And I'll just point at,

- Thank you. This has been fascinating. Employment, employment productivity has been improving. You know, farm agriculture went from 40% to 2% of the people in the United States in a century. Automation and software have already begun before AI to increase productivity. So the question is, what happens when we get to a point where everything the United States needs is produced by only half the effort we do now? I mean, so you half the people could be employed and half people not employed at all or everybody is employed halftime, but then what happens to their income relative to their, you know, mortgages and things like that. Has any, is anybody thinking about that?

- Thank you. Can we have a question here and then we'll, we'll throw them both to the panel at the same time.

- Mine's not related to that. It focuses on the substrates of the American dream dismount, a lot of attention on the dis growing disparity between the incomes of the richest and the incomes of the poorest. But it's my understanding that there's a great, there has been between census taking a great deal of mobility out of the lowest quintile, down from the highest quintile. So that this sense that there's an American dream out there that you can pursue and that you could be one of those, at least the middle class and maybe one of those upper quintiles was robust. I'm wondering if you have data about whether that movement is stalling and if so, what you think that portends to our ability politically to deal with the problems we have with our 10, with people's tendency to demand protection instead of risk and disruption.

- Throw those questions. They, they seem, those actually seem somewhat more related than, than maybe you think to me that they, they're both about, you know, opportunity in the future for people and, and how they look. Valerie, you

- Are, I'll take that first one. You know, what happens if we become so productive? You only need half the effort. So John Maynard Keynes, who wrote many things, you know, besides his ca had a beautiful essay, which I'm sure you can find online called The Economic Possibilities for our Grandchildren. And he wrote it in the midst of the Great Depression. But he predicted that over the next a hundred years productivity would increase eightfold. And he said suddenly that the economic problem of man will disappear. We won't have a shortage, you know, there will be abundance for all. But he said work is a good thing for people, some work. So he suggested that people might split it so that everybody works maybe 10 hours a week or five to 10 hours a week. Now as it turns out, we haven't seen a decrease in work. I have a paper called A Century of Work in Leisure that looks at what happened to, to work in leisure over the, the 20th century in the US among prime age people. Even though we became so much more productive, the hour average hours worked per, per, per per working age population actually didn't change. There was a shift from, from men to women because there was increased labor force participation. And part of it was, it's not that we wanted just more of the same old things, it's a suddenly we have all of these new things like, you know, relative to canes, we have flights to Europe, we have amazing health innovations that we all wanna be able to afford. Now in Europe, their hours have gone down. Some, not, not nearly as much as Kane's predicted, but some new evidence that came out from some researchers at Berkeley that seems to be because their governments put so much, so many labor market restrictions on them. So I think we can deal with these sorts of things. We might decide to just sort of, people don't have to work as many hours. If, if, if we decide that's the way we wanna approach it or the new goods that are produced are just so good, we still wanna work just as much because we like all of those new goods.

- So I'll, I'll, I'll chime in on that one. Hey, you, you put the question, do we work half as much each or half time each? How about we produce two times as much and work the same? And this is the AI question which somebody's gonna ask. What happens if AI takes all the jobs? We have seen this hundreds and hundreds of times before Gutenberg invents the printing press. Oh no, the monks will be out of a job. They'll all be, you know, what are they gonna do? The steam engine, the steam ship, the the tractor. 70% of Americans work on farms. The tractor is invented. Now 2% of Americans work on farms. 68% are not out, out in the streets unemployed with, with nothing to do. What happens every time it becomes cheaper to make stuff is we have new ideas, new things for people to do and, and we produce twice as much. That's exactly what's gonna happen this time and, and it's gonna be great. The mobility, I'm glad you brought it up. There's, there's nothing where the numbers are more jiggered than this whole income inequality mobility business. So first of all, anything you read be suspicious. I'll give you my bottom line. Take the, the allegation that income inequality is, is much, much worse than it ever was, is false. Especially when you look correcting over the life cycle. We're all, you know, you're, you're you're rich when you're middle aged. You're in high income when you're middle aged and you're low income when you're young and old. Is that inequality? No, that's just the life cycle. When you think about actual levels of consumption and so forth, it's much less than alleged. And mobility, it's kind of funny people say mobility isn't exactly random. That wherever you start is where you go up. Well is that really the benchmark is astounding in America, how many people from the bottom 20% actually end up at the top? And since not all the children can be above average, how many people fall down in the opposite direction? So there, there's a glass half full glass, half empty, but there is still quite substantial social mobility in the us.

- I'd give a slightly different answer from an economist answer to your question. So in the, in the book that I'm writing, I've read more philosophy than an economist would typically read. And I think what one sees is that people throughout history, across cultures really want to shine. They really want esteem, they really want dignity, they want to stand out. And so there will be technological innovations and I agree completely with with Valerie and John about, about where this is going in terms of jobs. But people, regardless of income, are going to try to figure out ways in order to be distinct. And I think that is both a source of human frustration and a source of great satisfaction. And if we have more stuff, we're gonna have the same desire to, to achieve. I think on inequality, I'll add two observations from research and I can be corrected. One is that it's important to distinguish the headline, which is differences in income when looking at a paycheck from differences from income, measuring it after taxes and after transfers. And if you ignore the top one 10th of 1% of the people and you focus on everybody else, the increase in inequality over say since the seventies after taxes and after government transfers has been fairly moderate. Definitely not what we are tend to see in, in in newspaper reporting. And the other is about this issue of intergenerational mobility. You know, whether you do better or worse where you move relative one's parents. And I think there's a nice study by Ward in the, in the a ER recently, which sort of says that that just hasn't changed too much over the century. So this notion that the American dream as characterized by that hasn't, hasn't diminished. We are all two generations from the

- Trailer

- Park in both

- Directions.

- If I can take moderator's privilege and just say about the, the fear that AI is gonna take all the jobs, you know, think about how many people you know who run five Ks, even though they're no one, none of them is faster than a cheetah or how many people enjoy singing even though none of them is ever gonna become professional and people have a tremendous hunger to achieve and they will keep seeking that regardless of, and they will find there are always, there's always new dimensions that you can, you could be the the best singer in, you know, this two square feet. So can we take a couple questions from this side? And again, I'm gonna take two and then just throw them in the panel. 'cause we're at, we're running very short on time. Do we have anyone on this side who wants? Do we have to call on people like hands up? Anyone, anyone over here then? Okay, well I don't and all the questioners are over here. You, you back there on the green shirt and the, and then the woman with her handed that fellow there and then that woman either in either order.

- Hi, thank you for the discussion. I wanna read out a favorite code of mine from an all time favorite movie. The Gods must be Crazy Civilized man refused to adapt himself to his environment. Instead he adapted his environment to suit him. So he built cities, roads, vehicles, missionary, and he put up power lines to run his labor saving devices. But somehow he didn't know when to stop. The more he improved his surroundings to make his life easier, the more complicated he made it. So now his children are sentenced to 10 to 25 years of school just to learn how to survive in this complex and hazardous habitat. They were born in two and civilized man who refused to adapt himself to his natural surroundings now finds he has to adapt and re-adapt himself every day and every hour of the day to his self-created environment. So I'd like to know your, the panel's thoughts about this

- And you, sir, in front of her have,

- Thank you. Bring us back to the title of the panel. Can America still deliver the American Dream? I'm curious, and I'm not guessing anybody's birthday on stage, but if, if you all had a choice to be born when you were versus be born when a lot of the students were that attend this university, now bringing it back to that bet you made, right with the, with the 10% up in the stakes a little bit, how would you bet your own life being born 20 years ago versus when you were

- Can I, - I'm, I'm really flattered that you think some of us were born 20 years ago.

- I can jump in on, I wanna, there's this fantasy of how simple life was back on the farm and we should just go back to something simpler than we had before. Life on the farm was rueful and short backbreaking labor all day long. And then you die young, your children die of horrible diseases. You know, all the Greta Thunberg who think this is a great idea, need to go spend some time on the farm. Our ancestors lived horrible lives. This is a great, this complicated life is a great civilization. How much more fun to spend time at school, learning how to, all sorts of wonderful things than to start at six years old, hoeing the ground. And that's your, that's what you're gonna do for the rest of your life until you starve where the soldiers come and take it all away. Even animals bears love McDonald's food given the choice they don't like. No,

- They keep getting stuck. Drive. Though I would